Three Perspectives That Change How You See the World

Posted on 2025-05-06 (https://office-bev.com/en/2025/05/06/1e-three-perspectives/)

1. Fiction – Yuval Noah Harari

2. Domains of Objects – Markus Gabriel

3. Relations – Carlo Rovelli

4. The Loop of Fiction, Domains, and Relations

5. The Disruptive Force of Domain Jumps

6. Concrete Examples of Domain Jumps

7. Conclusion: A New Way to See the World

The Fundamental Structure of the Balance Sheet

Posted on 2025-05-07 (https://office-bev.com/en/2025/05/07/2e-the-fundamental-sturucture-of-the-bs/)

1. What Is the Basic Structure of the Balance Sheet?

2. BS as a Tool for Applying the Three Perspectives

3. Applying the BS Binary Framework

4. Conclusion

The Dual Structure of the Balance Sheet: Fiction and Stock

Posted on 2025-05-08 (https://office-bev.com/en/2025/05/08/3e-the-dual-structure-of-the-bs/)

1. The Dual Structure of the Balance Sheet: Stock and Flow

2. The Structure of Flow: Claims and Obligations as Relational Constructs

3. Trust as the Foundation of Claims and Obligations—In Other Words, Fiction

4. The Balance Sheet as a Dual Structure: Fiction and Stock

5. Applying the Framework: Fiction and Stock Across the Balance Sheet

6. Conclusion

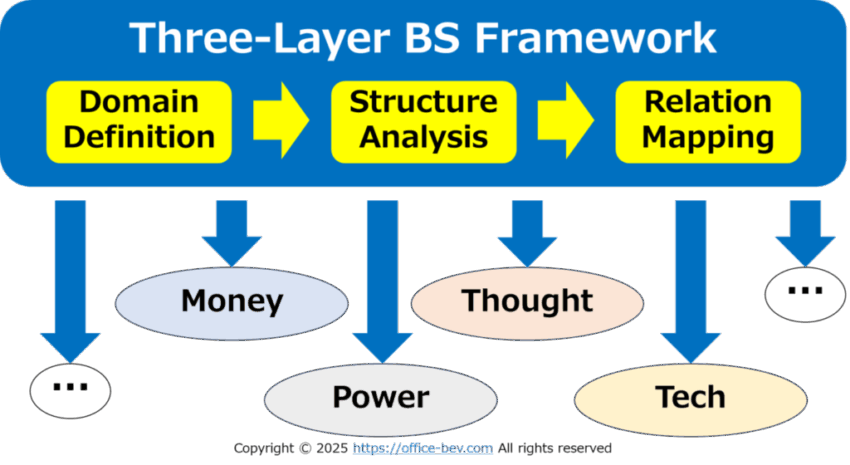

The Three-Layer Balance Sheet Framework — Interpreting Through Domain, Structure, and Relation

Posted on 2025-05-09 (https://office-bev.com/en/2025/05/09/4e-the-three-layer-bs-framework/)

1. Introduction: The Expanding Scope of BS Thinking

2. The Structure of the Three Layers

Layer 1: Whose BS? And of What? — Defining Perspective and Domain

Layer 2: What Is It Made Of? — Stock and Flow (i.e., Fiction)

Layer 3: With Whom? And How? — The Structure of Relation

3. Applying the Framework Across Domains

4. Conclusion: Connecting Past Posts and the Next Steps

Structural Analysis (1): The Genesis of Assets — Where Stock and Flow Begin

Posted on 2025-05-09 (https://office-bev.com/en/2025/05/09/5e-the-genesis-of-assets/)

1. Introduction: Where Do Assets Come From?

2. The Birth of Assets: Single-Entity Co-Generation

3. The Creation of Stock Assets

(1) Pure Stock Assets (Accumulated Assets)

(2) Stock-like Flow Assets (Structurally Created Assets)

(2-1) Securitized Claims

(2-2) Fictionally Created Claims

4. The Creation of Flow Assets

(1) Flow from Pure Stock Assets (Inter-Entity Co-Generation)

(2) Exchange of Stock-like Flow Assets (No Inter-Entity Co-Generation)

(3) Flow from Stock-like Flow Assets (Layered Flow Structures)

5. Conclusion: Genesis as the Structural Foundation of Assets

Structural Analysis (2): The Structure of Assets — The Forms of Stock and Flow

Posted on 2025-05-09 (https://office-bev.com/en/2025/05/09/6e-the-structure-of-assets/)

1. Introduction — What Kind of Structure Do Assets Have?

2. Self-Contained Stock Changes — Instantaneous Movements within a Single Entity

2.1 Single-Entity Co-Generation: Self-Contained Generation of Assets

(1) Generation of Pure Stock Assets

(2) Generation of Securitized Claims

(3) Generation of Fictional Claims

2.2 Single-Entity Co-Extinction: Self-Contained Extinguishment of Assets

3. Unilateral Stock Transfers — One-Way Movements between Entities

3.1 Involuntary Transfer: Without the Sender’s Intent

3.2 Voluntary Transfer: With the Sender’s Intent

4. Bilateral Stock Transfers — Exchange between Entities

5. Self-Contained Flow Cycles — Time-Based Transformations within a Single Entity

5.1 Consumption Flow: Input Aimed at Utility Recovery

5.2 Operational Flow: Input Aimed at Creating Value or Outcomes

6.Inter-Entity Flow Cycles — Time-Based Transactions between Entities

6.1 Lending Flow — Asset Deployment with Repayment Obligations

6.2 Investment Flow — Asset Deployment without Repayment Obligations

7. Asset Typologies and Structures

7.1 Typology of the Debit Side — Asset Status

(1) Absolute Assets

(2) Relational Assets (Repayment-Based Claims)

(3) Investment Assets (Return-Based Claims)

7.2 Typology of the Credit Side — Sources of Assets

(1) Relational Liabilities

(2) Relational Capital

(3) Absolute Capital

7.3 Structural Overview of Asset Typologies

8. Conclusion — The Path to Surplus

<Appendix> Visual Summary — Asset Movement & Typology Framework

Asset Movement Typologies (4 Quadrants, 8 Types)

[1] Self-Contained Stock Changes:

(1) Single-Entity Co-Generation & Co-Extinction

[2] Inter-Entity Stock Transfers:

(2) Involuntary Transfer (Unilateral / Without Intent)

(3) Voluntary Transfer (Unilateral / With Intent)

(4) Mutual Exchange (Bilateral)

[3] Self-Contained Flow Cycles

(5) Consumption Flow

(6) Operational Flow

[4] Inter-Entity Flow Cycles

(7) Lending Flow

(8) Investment Flow

Asset Typologies (6 Types)

[Debit Side: Asset Status]

・Absolute Assets ・Relational Assets ・Investment Assets

[Credit Side: Asset Sources]

・Relational Liabilities ・Relational Capital ・Absolute Capital

Structural Analysis(3): The Emergence of Surplus — Part 1: The Generation of Surplus

Posted on 2025-06-02 (https://office-bev.com/en/2025/06/02/7e-generation-of-surplus/)

1. Introduction – What Does It Mean for an Asset to Increase?

2. Where Does Surplus Arise?

2.1 Self-Contained Stock Change — Can Surplus Arise Within a Single Entity?

2.1.1 Pure Stock Assets (Accumulated Assets)

2.1.2 Stock-like Flow Assets (Structurally Created Assets)

(1) Securitized Claims

(2) Fictionally Created Claims

2.2 Inter-Entity Stock Transfers — Can Surplus Arise Through Asset Movement?

(1) Unilateral Transfer — One-Way Movement Without Return

(2) Bilateral Stock Transfer — Two-Way Movement Through Exchange

2.3 Self-Contained Flow Cycles — Can Internal Deployment Generate Surplus?

2.4 Inter-Entity Flow Cycles — Can Surplus Arise Through Relational Flows?

(1) Lending Flow — Principal and Interest

(2) Investment Flow — Capital and Returns

3. Only One Path Leads to Surplus

3.1 Asset Movement Types That Generate Surplus

3.2 Core Components and Cycles of Surplus

4. Conclusion — Surplus Emerges Only in Self-Contained Flow Cycles

Structural Analysis (3) The Emergence of Surplus — Part 2: The Sources of Surplus (Revision)

Posted on 2025-06-27 (https://office-bev.com/en/2025/06/27/8er-sources-of-surplus/)

1. Introduction: Surplus Seeks Money

2. Analysis of Self-Contained Flow Cycles: Exploring the Sources of Surplus

2.1 Development Structures within Self-Contained Flow Cycles

(Primary and Secondary Development Types)

2.2 Classification of Development Types within Self-Contained Flow Cycles

(1) Self-Contained Stock Change (Without Labor Input)

(2) Recovery of Labor through Consumption Flows

(3) Recovery of PSA through Labor-Driven Operational Flows

(4) Recovery of Money through Labor-Driven Operational Flows

Summary: Classification of Development Types by Surplus Elements

2.3 Analysis of Primary Development Types

(2.3.1) In-Depth Review of Primary Development Types

(2.3.2) Conclusion: The Fundamental Structure of Surplus Generation in Primary

Development

2.4 Analysis of Secondary Development Types

2.5 Summary: The Sources of Surplus

3. Conclusion — The Three Sources of Surplus

Structure Analysis (4) The Transformation of Assets — The Interlinked and Layered Structure of Stock and Flow (Revision)

Posted on 2025-07-30(https://office-bev.com/en/2025/07/30/9er-the-transformation-of-assets/)

1. Introduction – Assets That Interlink and Transform Through Domain Jumps

2. The Grand Circulation Structure of Assets — Generation → Transfer → Extinction

2.1 Generation of Assets as the Emergence of Surplus

2.2 Representing The Grand Circulation Structure through Eight Asset Movement Typologies

(1) Generation: The Emergence of Surplus

(2) Transfer: Asset Movements without Net Increase or Decrease

(3) Extinction: The End of Assets

2.3 The Essence of the Grand Circulation Structure of Assets

3. The Evolutionary Model of Asset Transfer — From Transfer to Transformation

(0) Phase Zero: The Onset of Self-Contained Asset Movements

(1) Phase One: Initiation of Inter-Entity Stock Transfers

(2) Phase Two: Initiation of Inter-Entity Flow Cycles

(3) Phase Three: Development of Multi-Layered Inter-Entity Flow Cycles

Summary: From Transfer to Transformation

4. Typologies of Asset Transformation — The Emergence of Layered Structures Through

Deepening of Inter-Entity Asset Movements

4.1 Self-Contained Asset Transformation

4.2 Inter-Entity Asset Transformation

4.2.1 Inter-Entity Stock Transformation: Investment Flows

4.2.2 Inter-Entity Flow Transformation: Domain Jumps

(1) Externalization

(2) Nesting

(3) Interlinkage

(4) Cross-Generation

5. Conclusion — Assets as Structures That Interlink, Layer, and Transform