Structure of This Article

This article proceeds as follows:

1. Introduction – Assets That Interlink and Transform Through Domain Jumps

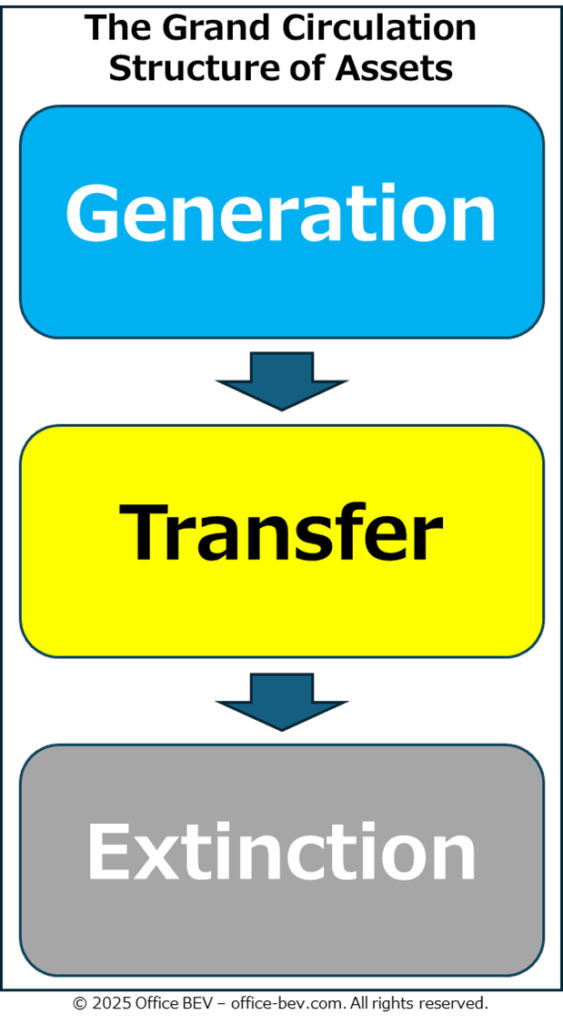

2. The Grand Circulation Structure of Assets — Generation → Transfer → Extinction

2.1 Generation of Assets as the Emergence of Surplus

2.2 Representing The Grand Circulation Structure through Eight Asset Movement Typologies

(1) Generation: The Emergence of Surplus

(2) Transfer: Asset Movements without Net Increase or Decrease

(3) Extinction: The End of Assets

2.3 The Essence of the Grand Circulation Structure of Assets

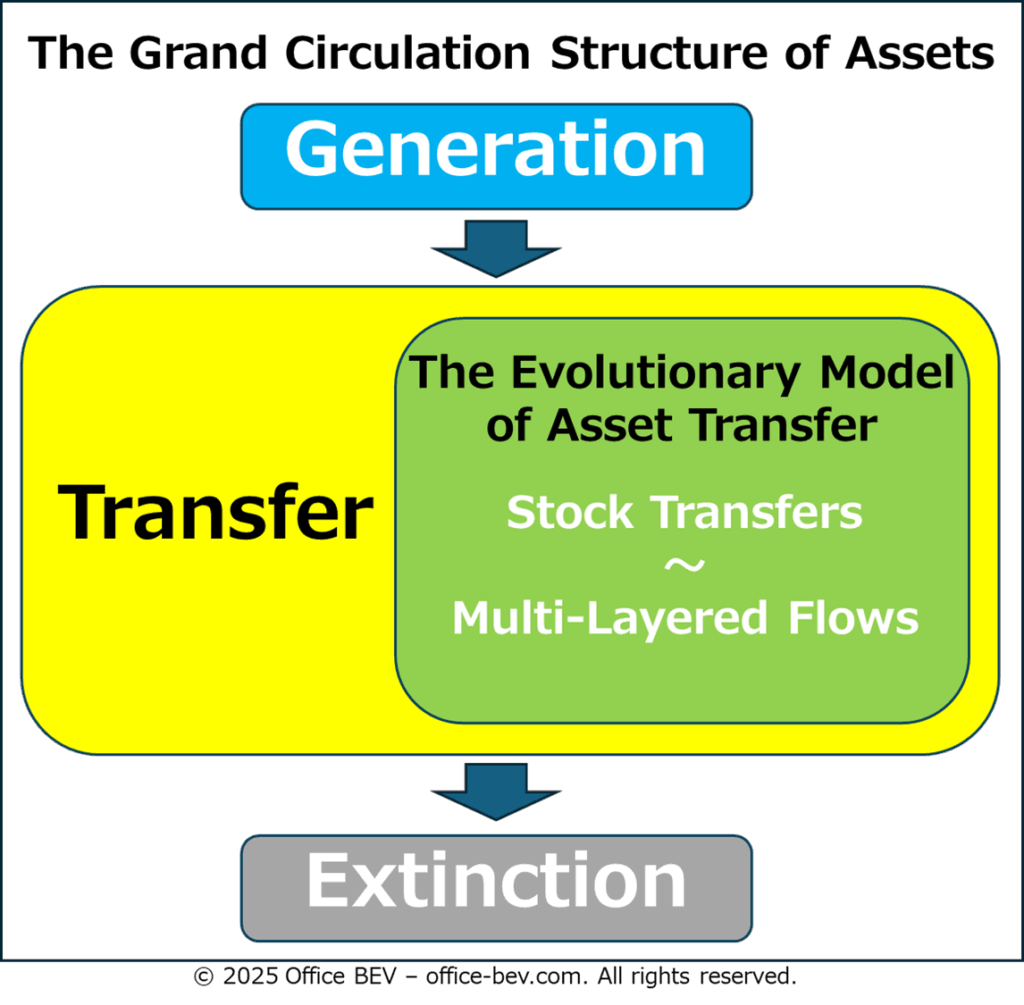

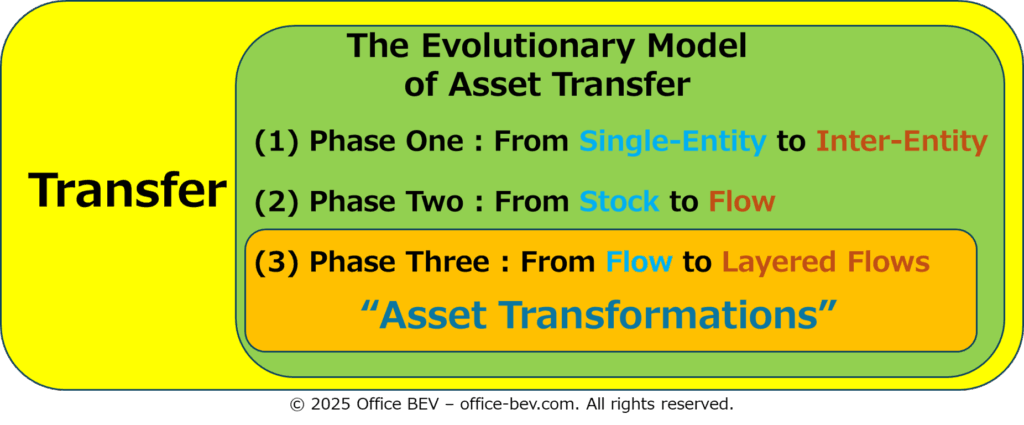

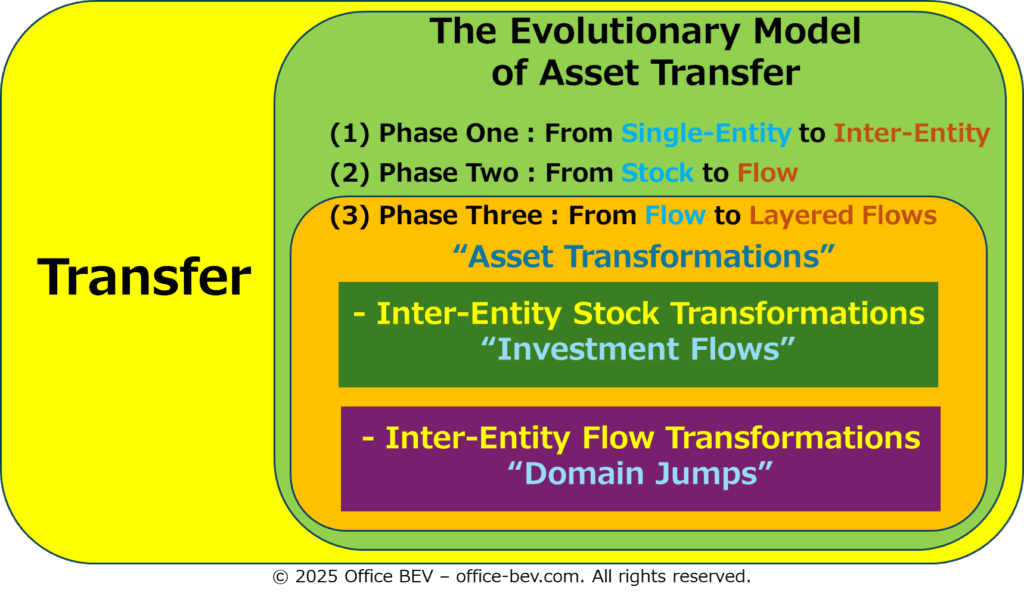

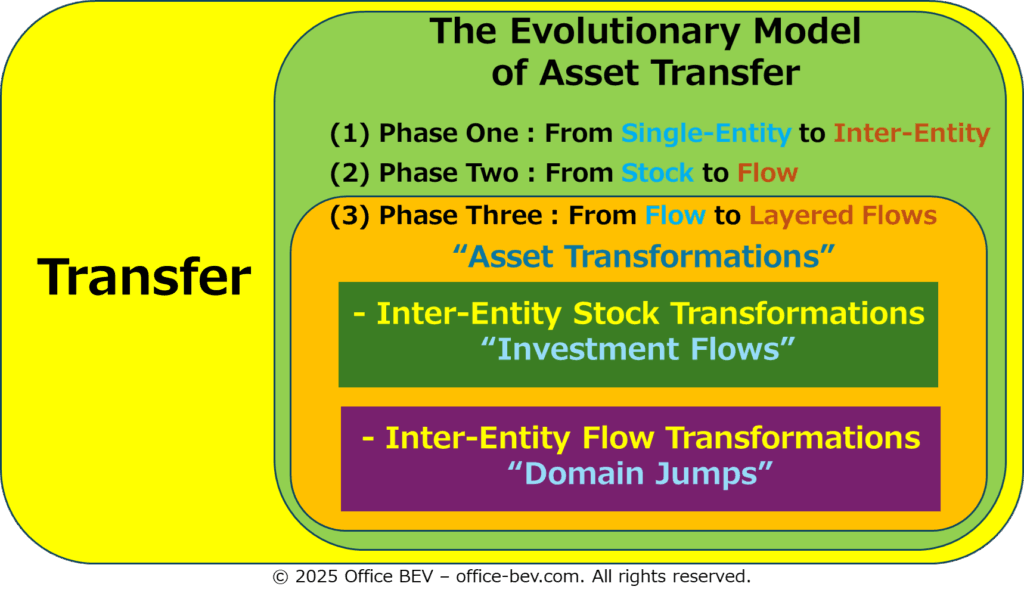

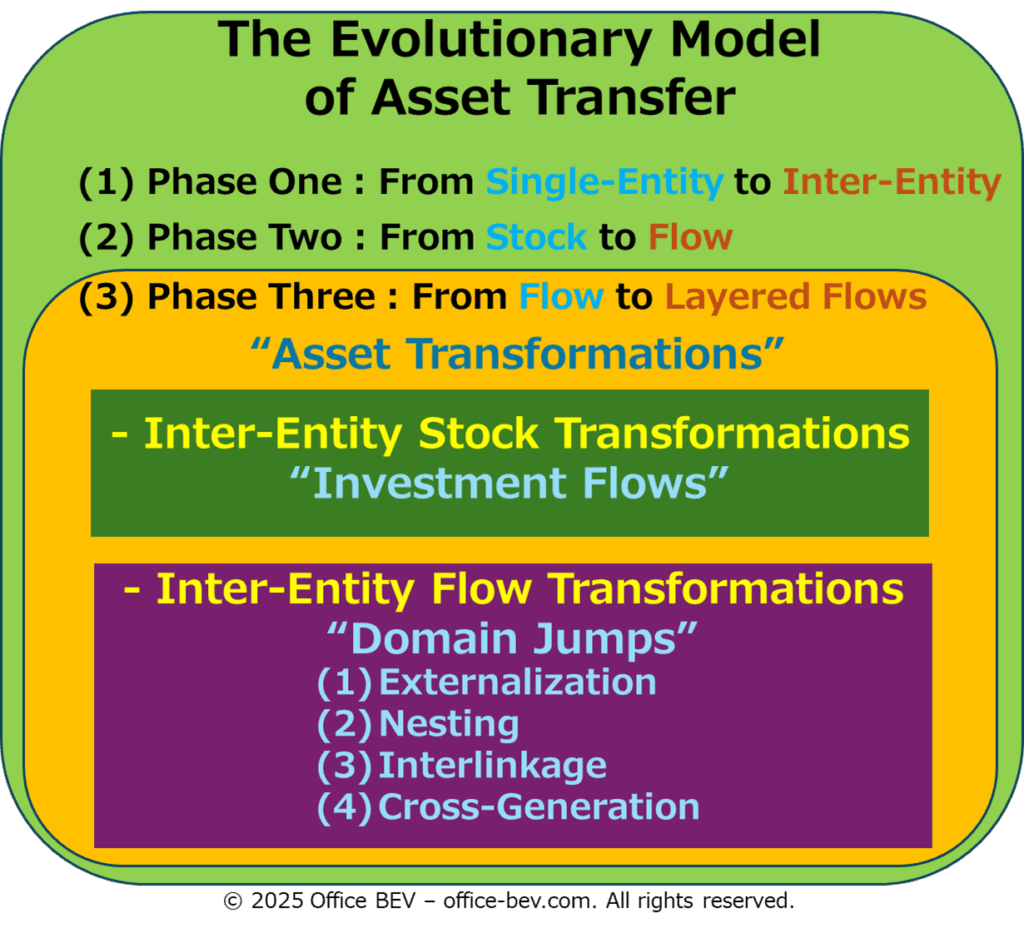

3. The Evolutionary Model of Asset Transfer — From Transfer to Transformation

(0) Phase Zero: The Onset of Self-Contained Asset Movements

(1) Phase One: Initiation of Inter-Entity Stock Transfers

(2) Phase Two: Initiation of Inter-Entity Flow Cycles

(3) Phase Three: Development of Multi-Layered Flows

Summary: From Transfer to Transformation

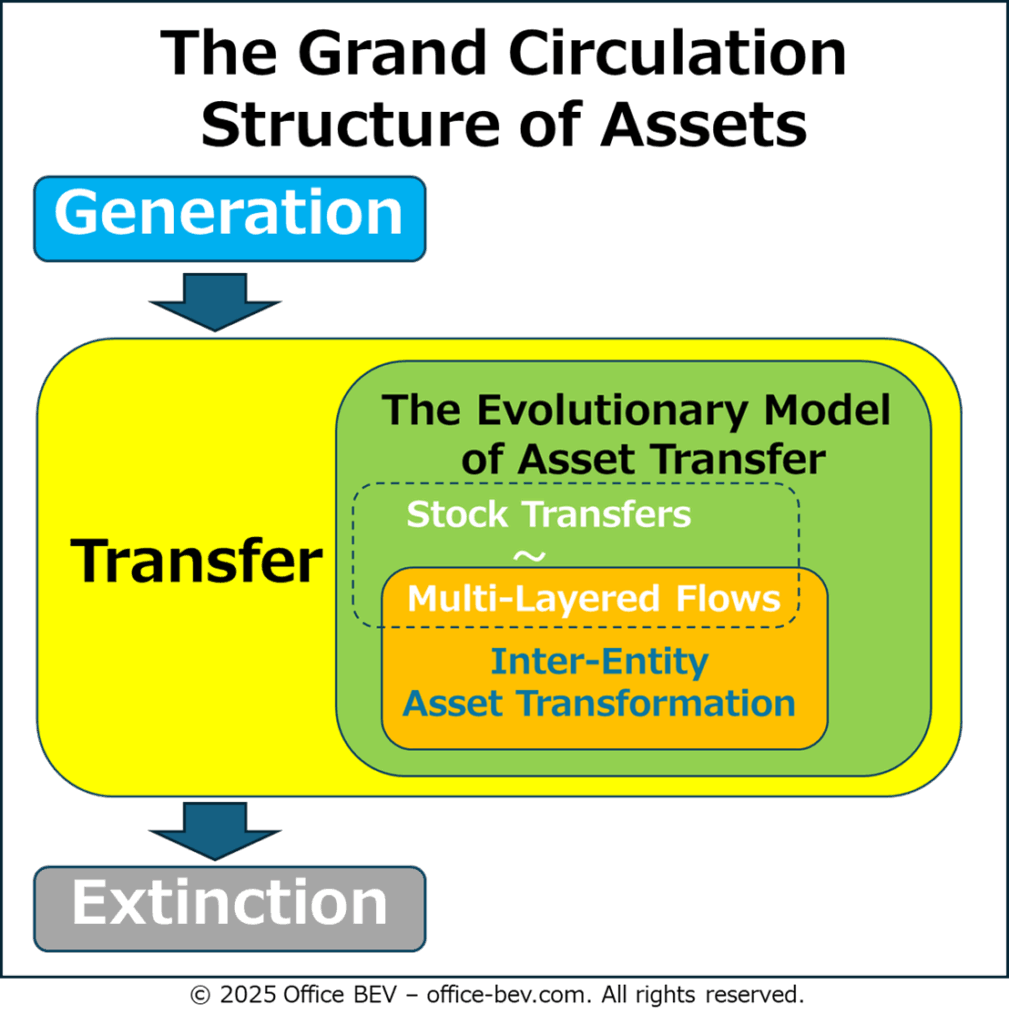

4. Typologies of Asset Transformation — The Emergence of Layered Structures Through

Deepening of Inter-Entity Asset Movements

4.1 Self-Contained Asset Transformation

4.2 Inter-Entity Asset Transformation

4.2.1 Inter-Entity Stock Transformation: Investment Flows

4.2.2 Inter-Entity Flow Transformation: Domain Jumps

(1) Externalization

(2) Nesting

(3) Interlinkage

(4) Cross-Generation

5. Conclusion — Assets as Structures That Interlink, Layer, and Transform

1. Introduction – Assets That Interlink and Transform Through Domain Jumps

In our previous posts, we examined how assets—both stocks and flows—move through various relational structures, as outlined in the Three-Layer BS Framework. We analyzed how assets emerge (Structure Analysis (1): The Genesis of Assets), how they move and interact across entities (Structure Analysis (2): The Structure of Assets), and how surplus arises within specific movement types (Structure Analysis (3): Part 1 — The Generation of Surplus; Part 2 — The Sources of Surplus).

Yet these asset movements are not merely linear. When assets are placed in inter-entity relationships, they often evolve into patterns that are far more intricate than simple transfers.

What structural dynamics drive this evolution?

At what point does “transfer” give way to “transformation”?

And how do layered and interlinked flows emerge from such movements?

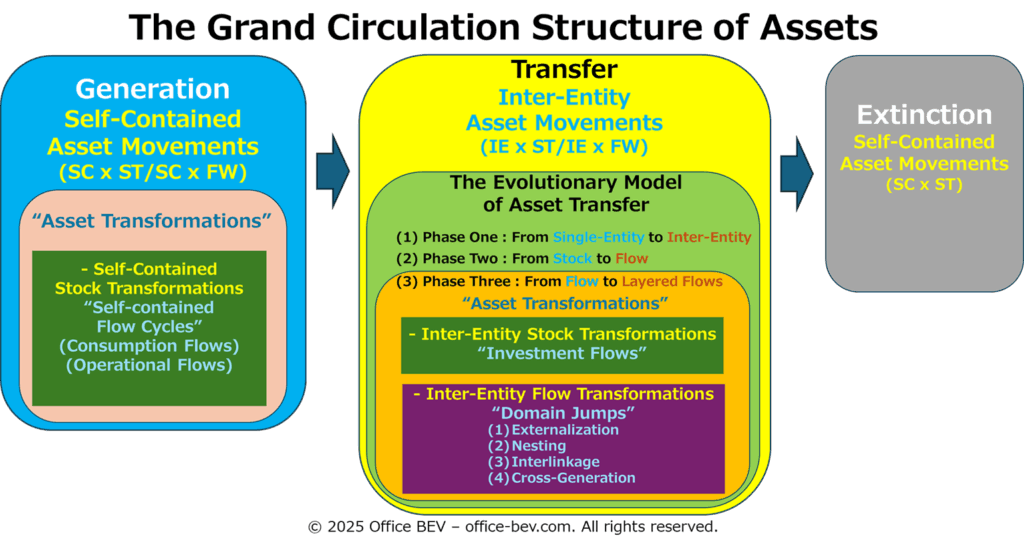

This article addresses these questions by first reframing asset dynamics within the Grand Circulation Structure of Assets—a cycle of Generation, Transfer, and Extinction (Chapter 2).

(Illustration inserted)

We then delve deeper into the “Transfer” phase by introducing the Evolutionary Model of Asset Transfer, which traces the structural deepening from Stock Transfers to Multi-Layered Flow Cycles (Chapter 3).

(Illustration inserted)

Finally, building on the final stage of the Evolutionary Model introduced in Chapter 3—where Asset Transfers begin to evolve into Layered and Interlinked Structures—we classify the Typologies of Asset Transformation, focusing on Inter-Entity Stock Transformation (Investment Flows) and Inter-Entity Flow Transformation (Domain Jumps) (Chapter 4).

(Illustration inserted)

To begin this exploration, we first revisit the Grand Circulation Structure of Assets—Generation, Transfer, and Extinction—in Chapter 2.

2. The Grand Circulation Structure of Assets — Generation → Transfer → Extinction

We have already examined how asset movements can be categorized into the four quadrants and eight typologies. When we step back and view these asset dynamics within a broader cyclical structure, we can identify three distinct phases in the movement of assets.

First, we have the Generation Phase, when a previously nonexistent asset is first recorded on the balance sheet.

Second, we observe the Transfer Phase, in which the generated asset is passed on to others. The eight typologies of asset movements unfold in various ways within this stage.

Finally, there comes the Extinction Phase, when even those assets that were once generated and actively circulating eventually cease to exist on the balance sheet.

These eight typologies unfold within an interconnected and recurring circulation structure, encompassing Generation, Transfer, and Extinction. While some may span multiple phases, each plays a distinct role in shaping the circulation of assets.

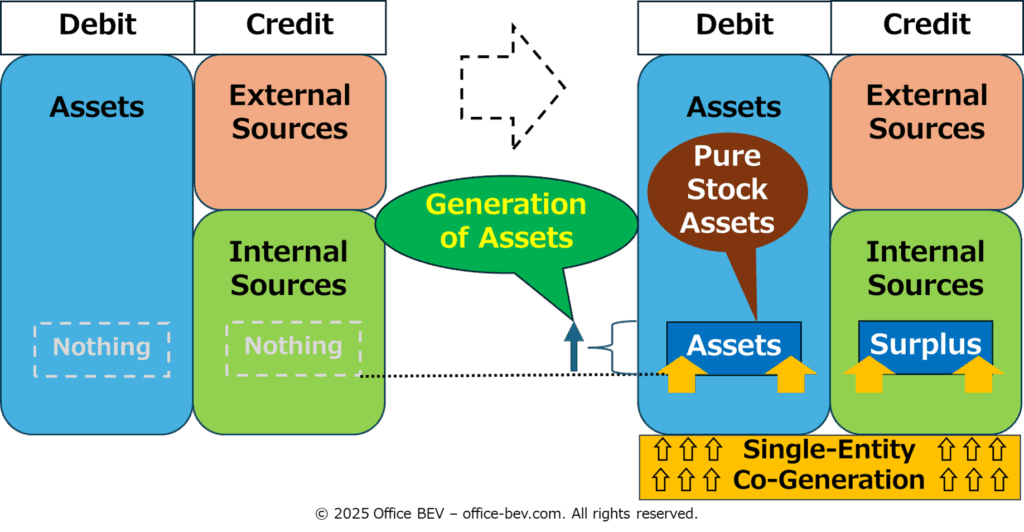

2.1 Generation of Assets as the Emergence of Surplus

The first phase of this Grand Circulation Structure—Generation—refers to the appearance of a previously nonexistent asset as a positive value on the balance sheet.

In essence, all forms of asset generation can be structurally understood as the Emergence of Surplus—a recovery that exceeds the value initially deployed.

As discussed in the previous post, Structure Analysis (3): The Emergence of Surplus (Part 1: The Generation of Surplus and Part 2: The Sources of Surplus), the concept of Surplus Emergence was already introduced and examined in detail.

However, not all surplus is structurally identical. We distinguish between two types of surplus:

- Genuine Surplus: A surplus that remains even when the analytical domain is extended to include all relevant entities and asset movements.

- Fictitious Surplus: A surplus that appears within a partial domain but disappears when the domain is expanded to include all relevant entities and the full scope of related asset movements.

This distinction is critical for evaluating whether asset generation constitutes a structurally sustained creation or merely a temporary and localized appearance of value.

As also confirmed in the previous post (Part 1: The Generation of Surplus), what appears to be surplus within the scope of inter-entity asset movements often turns out to be non-surplus when the analytical domain is expanded to include all relevant entities and the full scope of related asset movements. This is precisely what we define as Fictitious Surplus.

The distinction between Genuine and Fictitious Surplus will be explored in greater depth—particularly from the perspective of consolidated balance sheets—in the next article, Structure Analysis (5): The Nature of Surplus.

The remainder of this section will map the eight asset movement typologies onto the structural phases of The Grand Circulation —Generation, Transfer, and Extinction—highlighting how each typology contributes to the overall dynamic.

2.2 Representing The Grand Circulation Structure through Eight Asset Movement Typologies

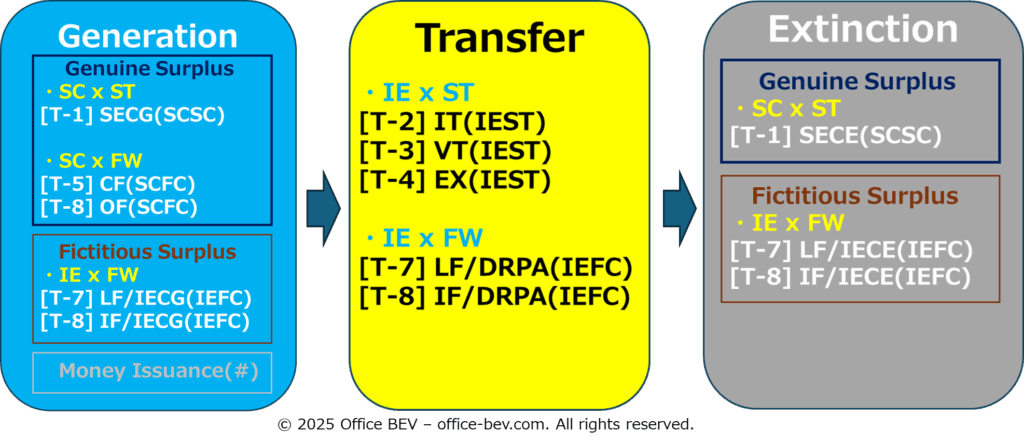

We now reorganize the Eight Typologies of Asset Movements previously introduced, aligning them with the three phases of the Grand Circulation Structure: Generation → Transfer → Extinction.

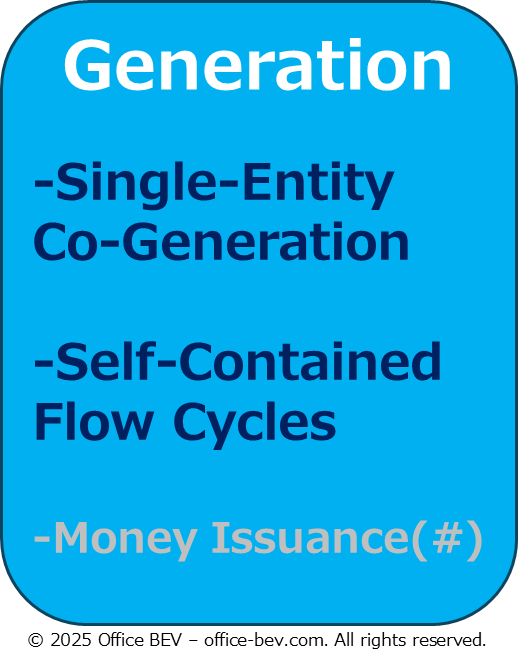

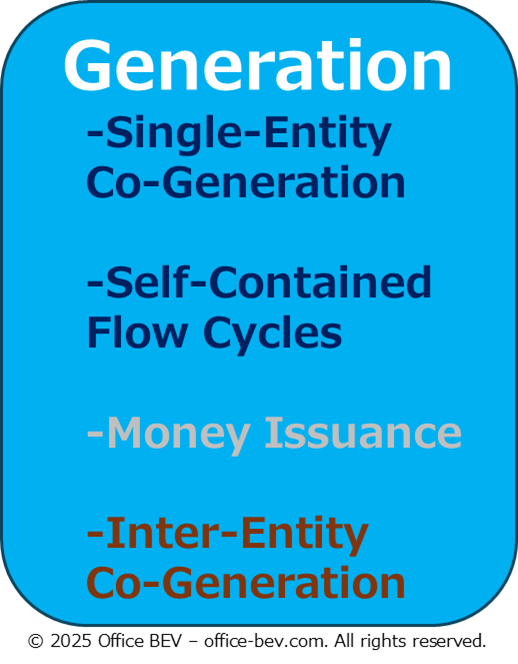

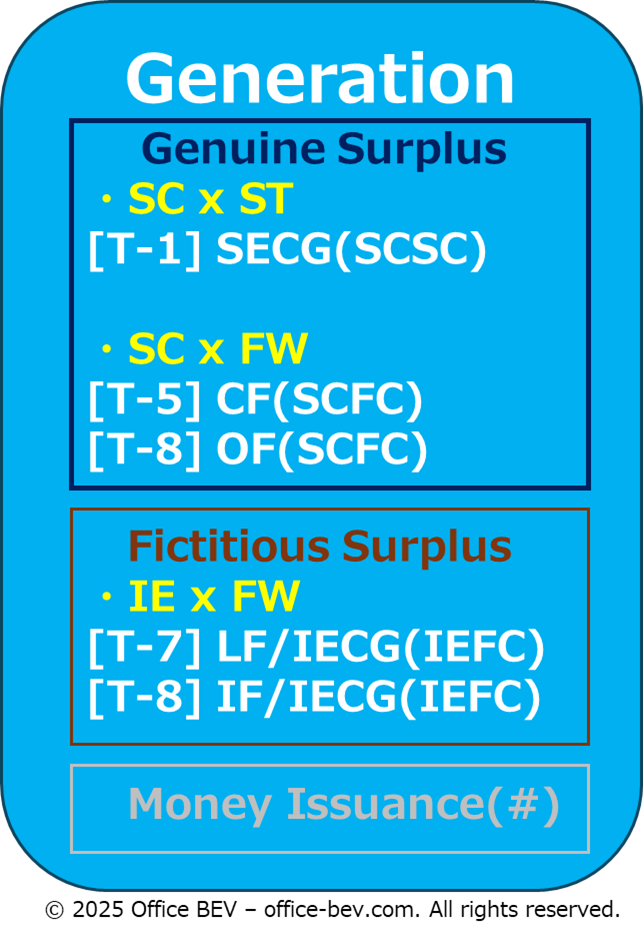

(1) Generation: The Emergence of Surplus

As previously discussed, Asset Generation structurally corresponds to The Emergence of Surplus. As outlined in Structure Analysis (3): Part 1 — The Generation of Surplus and Part 2 — The Sources of Surplus, this occurs in the following typologies:

- [Typology 1] Surplus generation in the form of PSA (Pure Stock Assets)

— through Self-Contained Stock Change (Single-Entity Co-Generation) - [Typologies 5 and 6] Surplus generation in the form of PSA

— through Self-Contained Flow Cycles (Consumption and Operational Flows) - Money Issuance

(Illustration inserted)

Note: (#) Whether

"Money Issuance"constitutes Genuine or Fictitious Surplus—if it constitutes surplus at all—will be examined in a future article, as discussed in Structure Analysis (3): Part 2 — The Sources of Surplus.)

We also noted in Structure Analysis (3): Part 1 — The Generation of Surplus that the following typologies involve the Generation of Claim–Obligation Flows:

[Typologies 7 and 8] Claim–obligation flows

— generated through Inter-Entity Co-Generation (Lending and Investment Flows)

Because these flows are typically nullified through Inter-Entity Co-Extinction, they cannot be regarded as structurally sustained surplus.

Consequently, this distinction aligns with the classification presented in Section 2.1:

- Genuine Surplus arises in Typology 1 and Typologies 5 and 6 — all within Self-Contained Asset Movements.

- Fictitious Surplus arises in Typologies 7 and 8 — within Inter-Entity Asset Movements.

However, because Fictitious Surplus ultimately disappears when the analytical scope is expanded to include all relevant entities and asset movements, it does not constitute surplus in the structural sense.

In this framework, Fictitious Surplus is not surplus at all. Accordingly, Typologies 7 and 8 do not generate surplus.

Genuine Surplus, by definition, never arises from Inter-Entity Asset Movements. Any perceived surplus in such movements is, without exception, Fictitious Surplus.

To conclude, asset generation can be further classified based on the nature of the asset and the type of surplus it entails:

• Generation of Stock Assets [Genuine Surplus]:

— through Single-Entity Co-Generation (Self-Contained Stock Change)

— through Self-Contained Flow Cycles (Consumption and Operational Flows)

• Generation of Inter-Entity Flows (Claims and Obligations) [Fictitious Surplus]:

— through Inter-Entity Co-Generation (within Inter-Entity Flow Cycles)

(Illustration inserted)

Note: (#) Money Issuance as Surplus Generation to be examined in a future article.

Note: ST(Stock), FW(Flow), SC(Self-Contained), IE(Inter-Entity), SCSC(Self-Contained Stock Changes), SECG(Single-Entity C-Generation), SECE(Single-Entity Co Extinction), SCFC(Self-Contained Flow Cycles), CF(Consumption Flows), OF(Operational Flows), IEFC(Inter-Entity Flow Cycles), IECG(Inter-Entity Co Generation), LF(Lending Flows), IF(Investment Flows),

In this framework, only Self-Contained Asset Movements give rise to Genuine Surplus, while Inter-Entity Generation of flows merely creates Fictitious Surplus, which does not structurally persist.

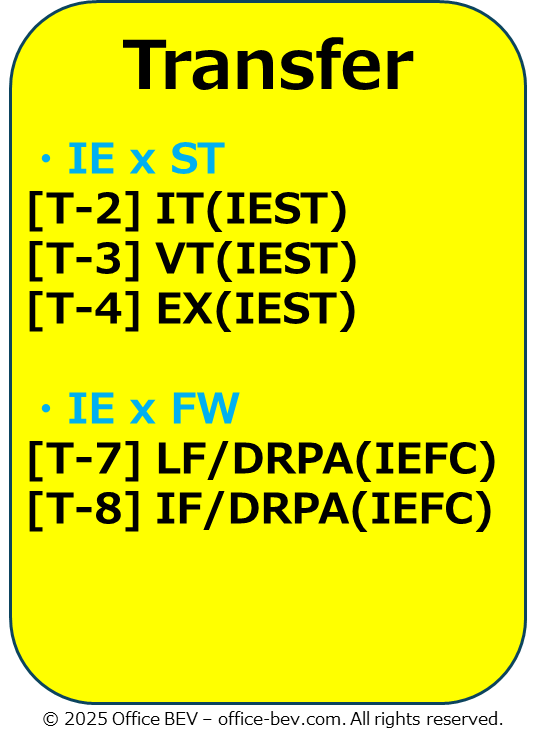

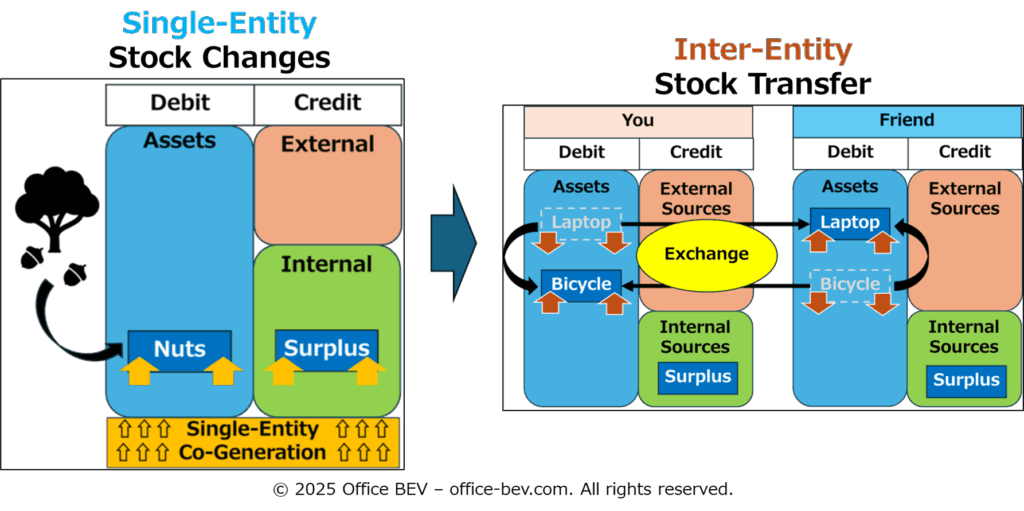

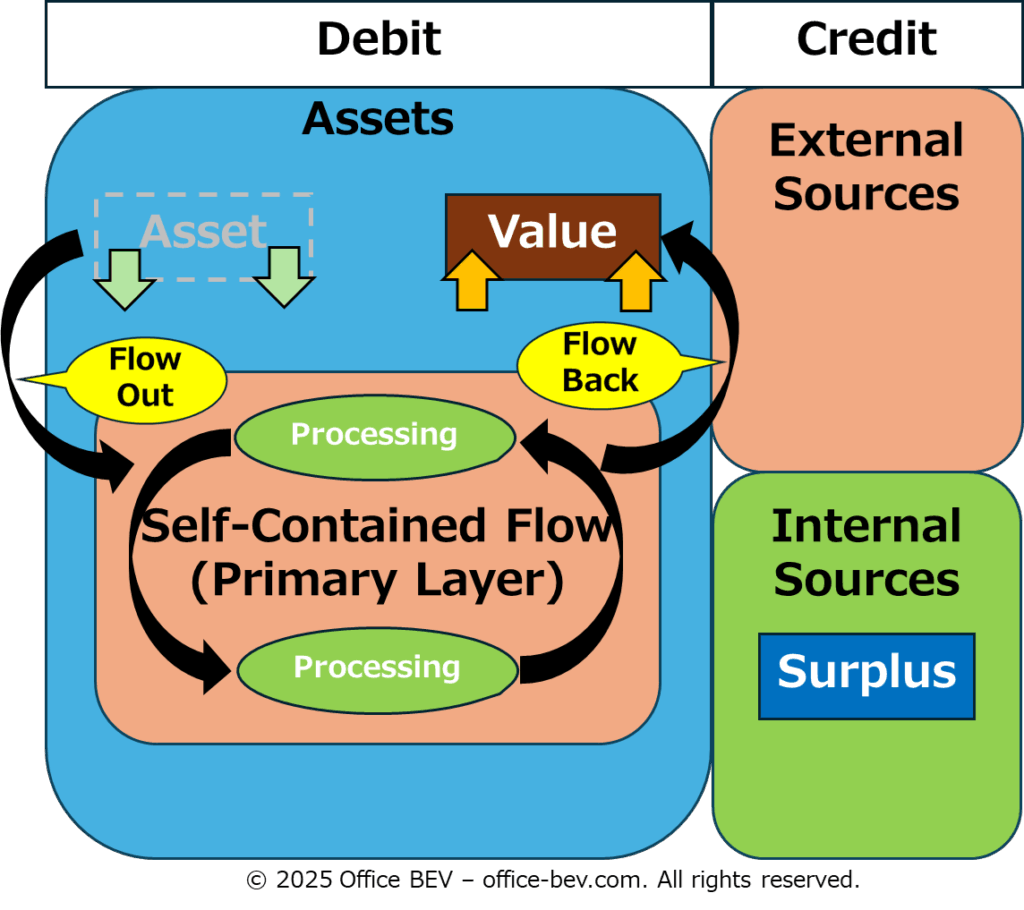

(2) Transfer: Asset Movements without Net Increase or Decrease

Once generated, assets circulate among entities across various structural relationships. However, in this framework, “Transfer” refers specifically to asset movements that entail no net increase or decrease in total assets—neither generation nor extinction.

Among the Asset Movement Typologies outlined in Structure Analysis (2): The Structure of Assets, those that correspond to this definition include:

- Inter-Entity Stock Transfers (Involuntary Transfer, Voluntary Transfer, and Mutual Exchange)

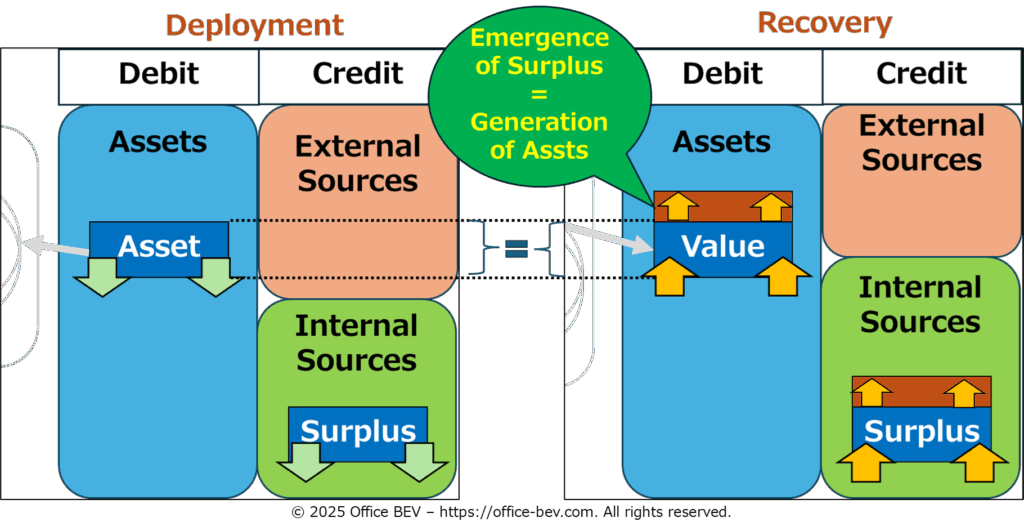

— corresponding to Typologies (2), (3), and (4) - Deployment and Recovery of Principal Assets within Inter-Entity Flow Cycles (Lending and Investment Flows)

— corresponding to Typologies (7) and (8)

(Illustration inserted)

Note: ST(Stock), FW(Flow), SC(Self-Contained), IE(Inter-Entity), IEST(Inter-Entity Stock Transfers), IT(Involuntary Transfers), VT(Voluntary Transfers), EX(Exchanges), IEFC(Inter-Entity Flow Cycles), DRPA(Deployment & Recovery of Principal Asset), LF(Lending Flows), IF(Investment Flows),

In each case, assets simply move from one entity to another. When viewed from the extended domain of all involved parties, the total amount of assets remains unchanged. In stock transfers, an asset moves from one balance sheet to another. In flow cycles, principal assets are deployed from one party’s balance sheet to another and then recovered—returning to the original holder. Throughout these processes, no new value is created; the asset’s ownership simply shifts.

Note: Although claim–obligation flows are generated during these Inter-Entity Flow Cycles and may appear to increase assets within a partial domain, they represent fictitious surplus. When the scope is expanded to include the full cycle of asset movements, these flows are structurally extinguished through Inter-Entity Co-Extinction. Accordingly, no net asset increase occurs.

Note: Asset transformations within Self-Contained Flow Cycles may appear to involve transfer, but the assets remain entirely within a single balance sheet. Since they do not leave the entity or change ownership, they fall outside the scope of inter-entity transfers as defined in this section.

Let us now reconsider transfer from the perspective of the type of asset being transferred—stock or flow.

Stock assets:

Both Inter-Entity Stock Transfers and the Deployment and Recovery of Principal Assets clearly involve Pure Stock Assets (PSAs) as the object of transfer.

Flow assets:

Claim–obligation flows can also serve as transferrable assets within these two types of movements. For example:

– Entitlements to future dividends can be traded—that is, flow-based claims treated as transferrable assets.

– In certain forms of contributions, existing flow-based claims (such as equity shares) may be used as the principal asset deployed or recovered.

Thus, both stock and flow assets can serve as the object of transfer within inter-entity movements. This confirms that the domain of asset transfer spans across both types of assets.

Note: The deployment of flow-based claims as input into other flow cycles—a structure that creates layered inter-entity relationships—will be examined in a later chapter of this article (Chapter 4).

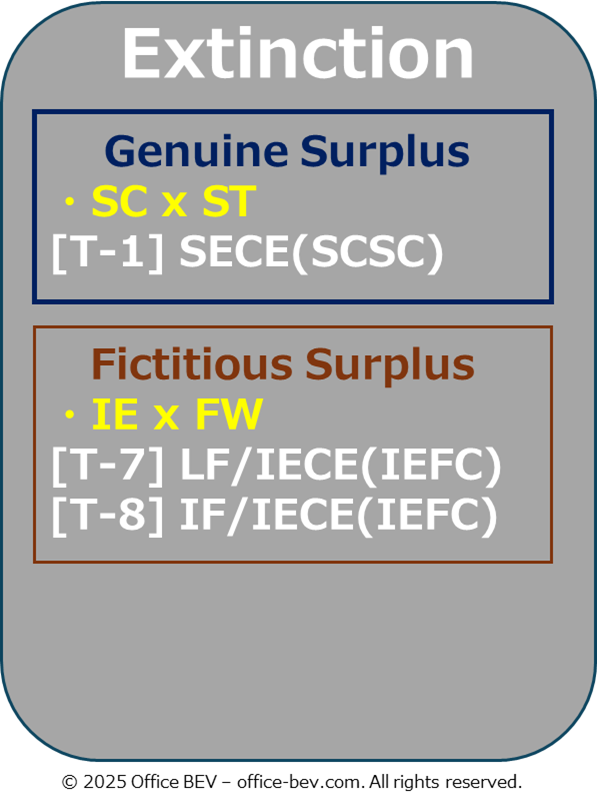

(3) Extinction: The End of Assets

Once generated and transferred in various forms, how do assets eventually come to an end?

In this framework, extinction is defined as the structural inverse of generation. Accordingly, we can classify asset extinction by tracing each type of generation process discussed previously.

Extinction of PSA generated through Single-Entity Stock Change

PSAs generated through Single-Entity Co-Generation—i.e., assets that emerge through internal generation within a Single Entity—are extinguished through the inverse structure, i.e., Single-Entity Co-Extinction.

— Corresponds to Typology (1)

Extinction of PSA generated through Self-Contained Flow Cycles

PSAs generated through Self-Contained Flow Cycles (such as Consumption or Operational Flows) are structurally identical to those generated through Single-Entity Stock Change in terms of their emergence as PSAs. Accordingly, these too are ultimately extinguished through Single-Entity Co-Extinction.

Extinction of Claims and Obligations generated through Inter-Entity Flow Cycles

Claims and obligations that were generated as Fictitious Surplus within Inter-Entity Flow Cycles—such as Lending or Investment Flows—are extinguished through Inter-Entity Co-Extinction, completing the cycle.

— Corresponds to Typologies (7) and (8)

We can now summarize asset extinction along two axes: Stock vs. Flow and Genuine vs. Fictitious Surplus.

- Extinction of Stock Assets [Disappearance of Genuine Surplus]

→ through Single-Entity Co-Extinction (Typology 1) - Extinction of Inter-Entity Flows (Claims and Obligations) [Reversion of Fictitious Surplus]

→ through Inter-Entity Co-Extinction (Typologies 7 and 8)

(Illustration inserted)

Note: ST(Stock), FW(Flow), SC(Self-Contained), IE(Inter-Entity), SCSC(Self-Contained Stock Changes), SECE(Single-Entity Co Extinction), IEFC(Inter-Entity Flow Cycles), IECE(Inter-Entity Co Extinction), LF(Lending Flows), IF(Investment Flows)

2.3 The Essence of the Grand Circulation Structure of Assets

As demonstrated above, the eight typologies of asset movements align with the three structural phases of asset dynamics—Generation, Transfer, and Extinction—each serving a distinct role in the Grand Circulation Structure of Assets:

- Generation: Typologies (1), (5), (6), (7), (8)

- Transfer: Typologies (2), (3), (4), (7), (8)

- Extinction: Typologies (1), (7), (8)

(Illustration inserted)

Note: ST(Stock), FW(Flow), SC(Self-Contained), IE(Inter-Entity), SCSC(Self-Contained Stock Changes), SECG(Single-Entity C-Generation), SECE(Single-Entity Co Extinction), IEST(Inter-Entity Stock Transfers), IT(Involuntary Transfers), VT(Voluntary Transfers), EX(Exchanges), SCFC(Self-Contained Flow Cycles), CF(Consumption Flows), OF(Operational Flows), IEFC(Inter-Entity Flow Cycles), DRPA(Deployment & Recovery of Principal Asset), IECG(Inter-Entity Co Generation), IECE(Inter-Entity Co Extinction), LF(Lending Flows), IF(Investment Flows)

We can reinterpret these movements through the lens of Genuine vs. Fictitious Surplus, and map them onto the Four Quadrants defined by the Three-Layer BS Framework (Self-Contained vs. Inter-Entity × Stock vs. Flow):

Genuine Surplus

- Generation: Single-Entity Co-Generation (Self-Contained Stock Change), Self-Contained Flow Cycles

- Transfer: Inter-Entity Stock Transfers, Deployment and Recovery of Principal Assets within Inter-Entity Flow Cycles

- Extinction: Single-Entity Co-Extinction (Self-Contained Stock Change)

Fictitious Surplus

- Generation: Inter-Entity Co-Generation within Inter-Entity Flow Cycles

- Transfer: Same as Genuine Surplus, namely, Inter-Entity Stock Transfers, Deployment and Recovery of Principal Assets within Inter-Entity Flow Cycles

- Extinction: Inter-Entity Co-Extinction within Inter-Entity Flow Cycles

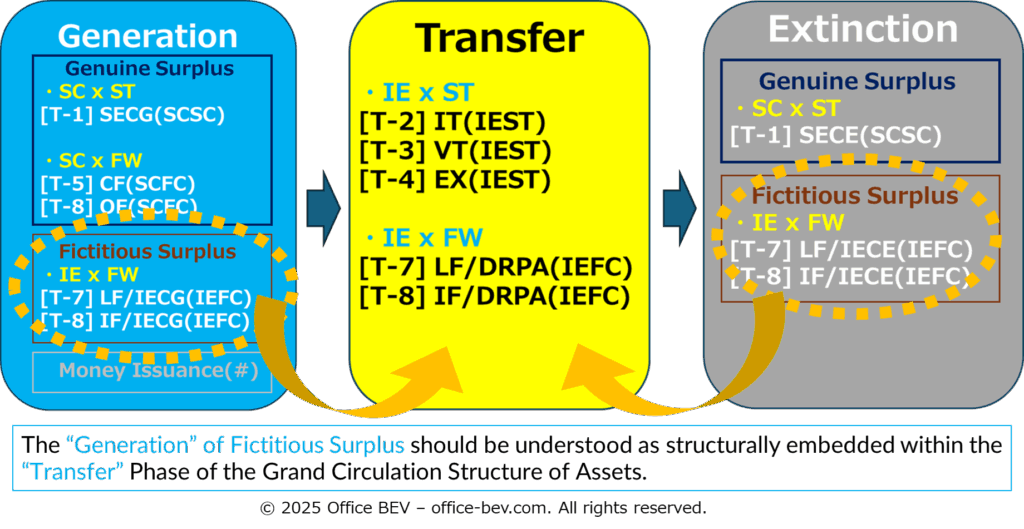

Note on Fictitious Surplus:

Fictitious Surplus arises from Inter-Entity Co-Generation within Inter-Entity Flow Cycles, but in the Grand Circulation Structure based on the Generation of Genuine Surplus, Inter-Entity Flow Cycles appear only in the Transfer phase, not in Generation. Moreover, such Co-Generation always originates from the deployment of Principal Assets—a Movement that itself belongs to the Transfer phase. Therefore, what appears to be the “Generation” of Fictitious Surplus should be understood as structurally embedded within the “Transfer” Phase of the Grand Circulation Structure of Assets.

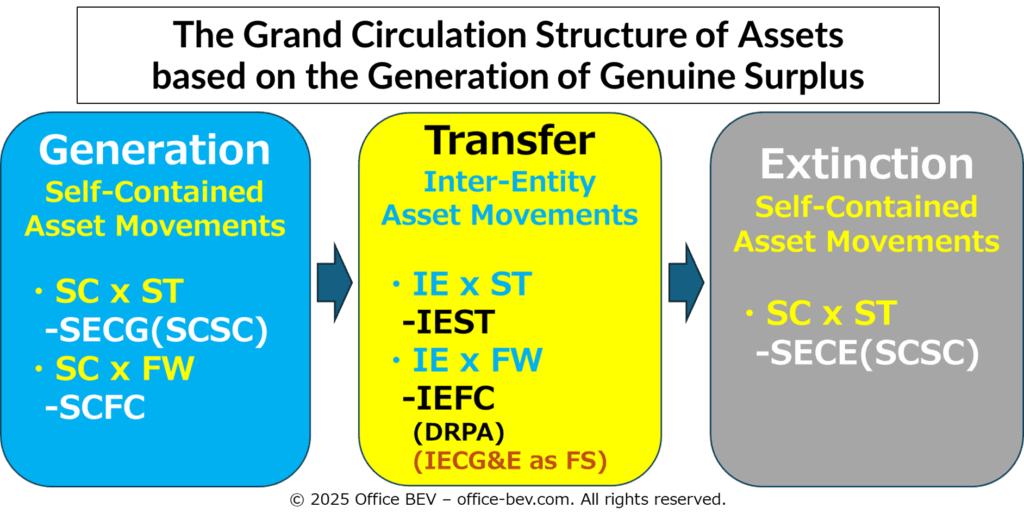

Conclusion — The Essence of the Grand Circulation Structure of Assets

Based on the above understanding, the Grand Circulation Structure of Assets—grounded in the Generation of Genuine Surplus—can be summarized as follows:

• Generation: Self-Contained Asset Movements

– Single-Entity Co-Generation (Self-Contained Stock Change)

– Self-Contained Flow Cycles

• Transfer: Inter-Entity Asset Movements

– Inter-Entity Stock Transfers

– Inter-Entity Flow Cycles(Deployment & Recovery of Principal Asset, Inter-Entity Co-Generation & Extinction of Flow Elements as Fictitious Surplus)

• Extinction: Self-Contained Asset Movements

– Single-Entity Co-Extinction (Self-Contained Stock Change)

Note: IECG&E as FS (Inter-Entity Co Generation and Extinction as Fictitious Surplus)

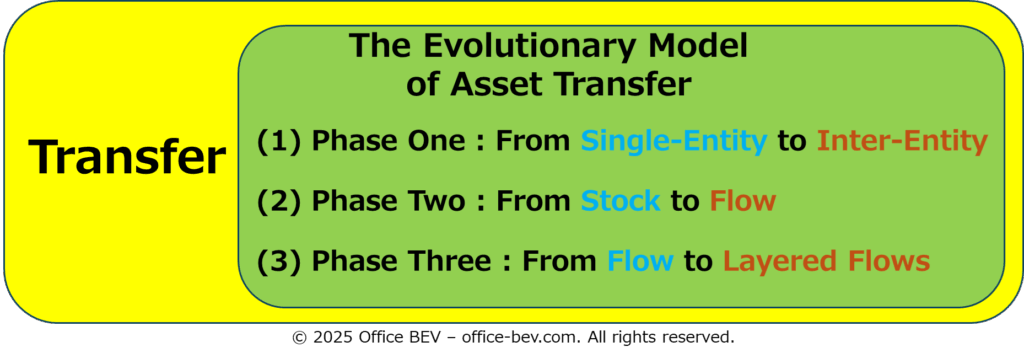

3. The Evolutionary Model of Asset Transfer — From Transfer to Transformation

In the previous chapter, we examined the Grand Circulation Structure of assets—a dynamic cycle comprising Generation, Transfer, and Extinction. In this chapter, we shift our focus to the second phase: Transfer.

Rather than viewing asset transfers as a flat array of independent movements, we seek to uncover a deeper structure—one that reveals how asset transfer progresses through structural stages and gives rise to more complex forms of Asset Transformation.

Within the realm of asset movement, we observe various transfer typologies: Inter-Entity Stock Transfers (such as Involuntary Transfer, Voluntary Transfer, and Mutual Exchange), and Inter-Entity Flow Cycles (such as Lending and Investment Flows). At first glance, these may appear as a collection of discrete patterns. But when reinterpreted as a sequence of structural developments, a coherent model of progressive deepening begins to emerge.

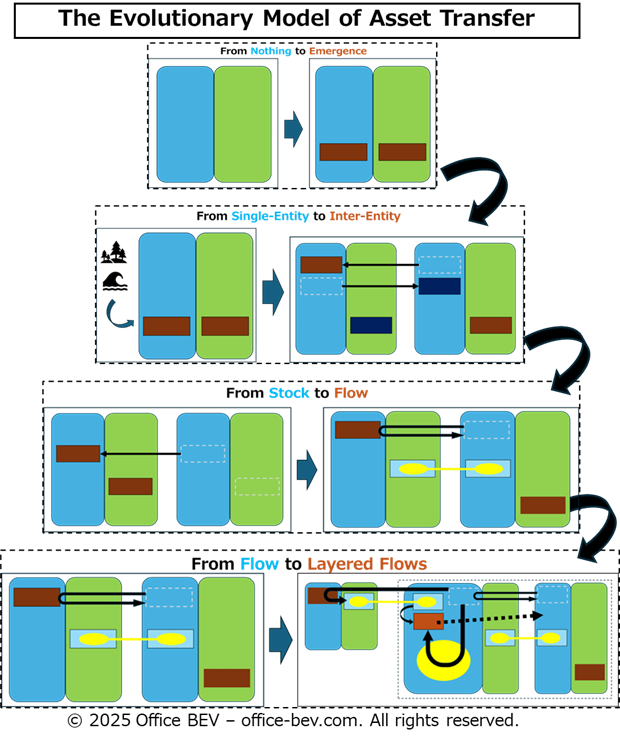

This chapter aims to illuminate that developmental logic. We introduce a Three-Stage Evolutionary Model of asset transfer, identifying the key turning points—structural thresholds—that make more sophisticated forms of asset movement possible.

(Illustration inserted)

Through this lens, we explore how each stage expands the potential for new types of interaction, laying the groundwork for more intricate inter-entity structures and eventually leading toward asset transformation.

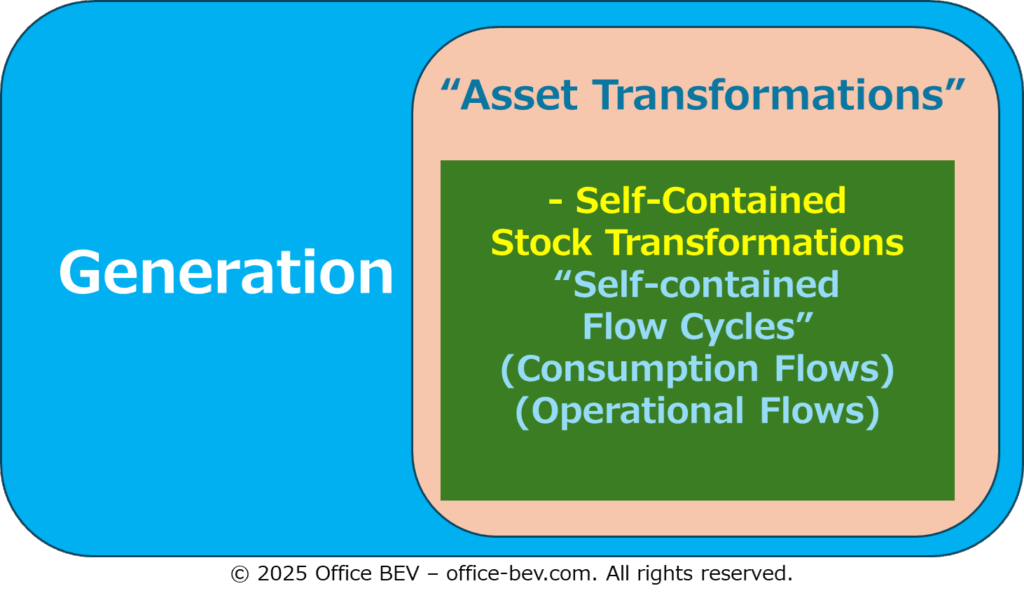

(0) Phase Zero : The Onset of Self-Contained Asset Movements

[From Nothing to Emergence]

All assets that circulate must have originated at some point, somewhere.

As discussed in Chapter 2 — The Grand Circulation Structure of Assets — the condition that precedes any asset transfer is the prior generation of the asset. Let us briefly recall the typologies of asset generation relevant here.

- Single-Entity Co-Generation (Self-Contained Stock Change) [Typology (1)]

- Self-Contained Flow Cycles (Consumption and Operational Flows) [Typologies (5) and (6)]

(Illustration : Generation of Assets through Single-Entity Co-Generation)

(Illustration: Generation of Assets through Self-Contained Flow Cycles)

These forms of Generation occur within a Single Entity and do not presuppose any relationship with other entities. They are fully Self-Contained Asset Movements.

Note: As confirmed in Chapter 2, these types of generation correspond to the creation of

Genuine Surplus within Self-Contained Asset Movements.

However, in contrast, Fictitious Surplus—specifically, the generation of claims and

obligations in inter-entity flow cycles—emerges not from within Self-Contained Asset Movements, but from the Deployment of Principal Assets into Inter-Entity Flow Cycles, i.e.,

through the Transfer of existing stock.

Therefore, the generation of Fictitious Surplus takes place within the structural evolution

of Asset Transfers, not prior to it.

The corresponding typologies are:

・Lending Flows (Inter-Entity Flow Cycle): [Typology (7)]

・Investment Flows (Inter-Entity Flow Cycle): [Typology (8)]

(1) Phase One: Initiation of Inter-Entity Stock Transfers

[From Single-Entity to Inter-Entity]

Once generated, assets are first introduced into relationships with other entities. At this stage, the asset undergoes a simple, unidirectional Transfer to another entity, initiating a relative change in stock positions.

Inter-Entity Stock Transfers (Involuntary Transfer, Voluntary Transfer, or Mutual Exchange)[Typologies (2), (3), and (4)]

(Illustration inserted)

This marks the first moment when an asset moves from one balance sheet to another, establishing an Inter-Entity relationship in the form of Stock Transfer.

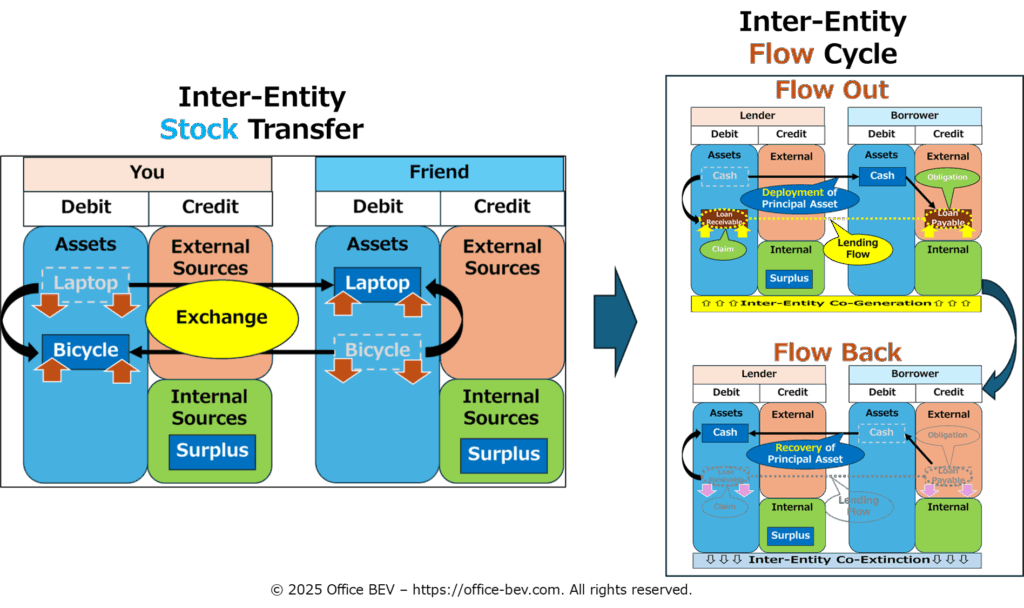

(2) Phase Two: Initiation of Inter-Entity Flow Cycles

[From Stock to Flow]

Next, asset movements evolve from instantaneous, one-way transfers to processes that unfold over time. A transferred asset is not simply handed over, but is instead set to return after a certain period—initiating a time-based flow structure. This marks the beginning of Inter-Entity Flow Cycles, with Lending Flows emerging at this stage.

Lending Flows (Inter-Entity Flow Cycle) [Typology (7)]

(Illustration inserted)

Asset transfers now function not as isolated events, but as temporally extended processes that embed expectations of Recovery.

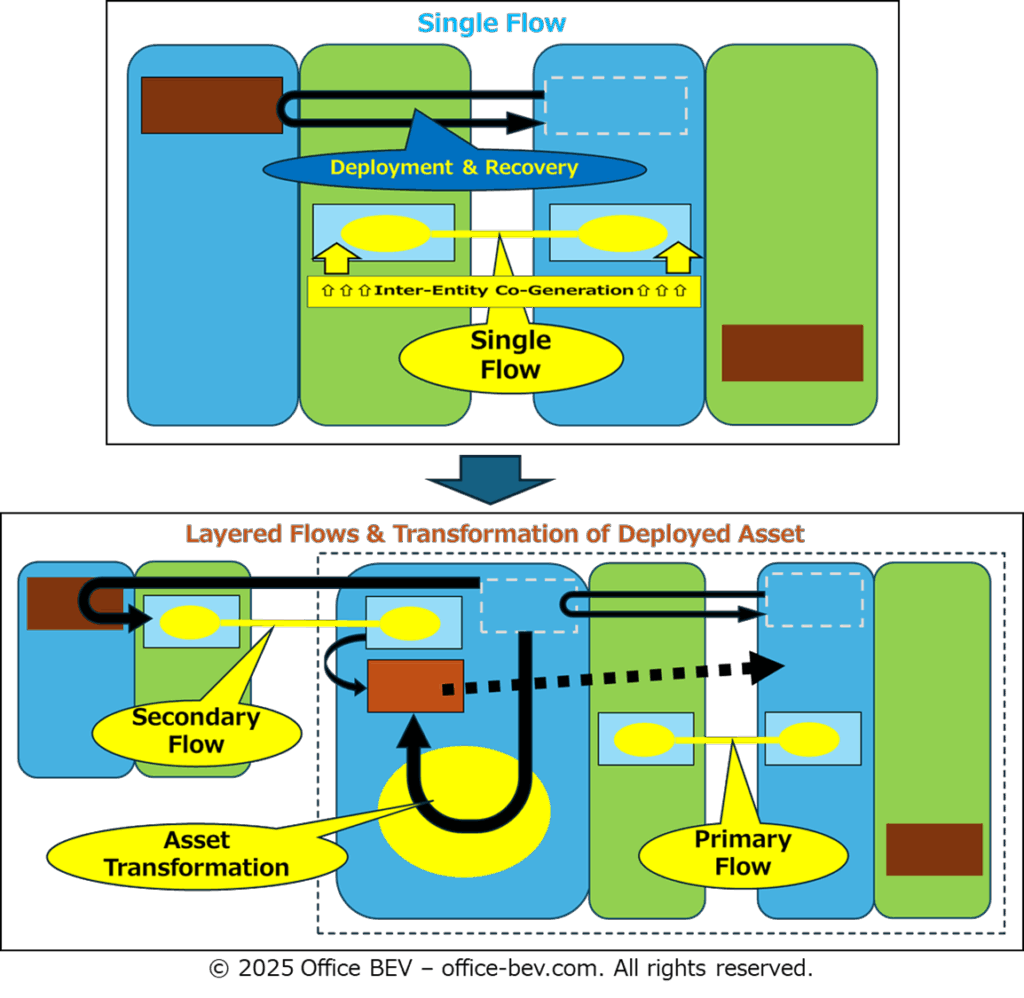

(3) Phase Three: Development of Multi-Layered Flows

[From Flow to Layered Flows]

Asset movement enters a more complex stage where the transferred principal itself undergoes Transformation or Redeployment by the recipient. These are no longer simple back-and-forth flows, but evolve into Layered Flow Structures that generate further asset creation and chain reactions of movement.

Investment Flows (Inter-Entity Flow Cycle) [Typology (8)]

Domain-Jumps [Externalization, Nesting, Interlinkage, Cross-Generation]

(Illustration inserted)

At this stage, the deployed assets generate new Flows by involving third entities, resulting in Layered Flow formations and resulting in Multi-Layered and Interlinked Inter-Entity Relationships. Asset Transfer thus unfolds into a network of Transformations that continuously regenerate new Layered Flows.

Summary: From Transfer to Transformation

Following the initial Generation of assets, asset transfers deepen through three evolutionary stages:

- From Single-Entity to Inter-Entity

- From Stock to Flow

- From Flow to Layered Flows

(Illustration inserted)

Layered flows, which emerge at the final stage of this three-phase evolution, mark the threshold where Transfer begins to turn into Transformation. In fact, this third stage is no longer merely a form of Transfer—it represents the onset of Structural Asset Transformation.

In Chapter 4, we will explore this Transformation in greater depth—specifically, how Inter-Entity Flows undergo Transformation into Layered Flows through the Structural Layering of Stock and Flow Elements, which triggers Domain-Jump dynamics. We will examine how such Structural Layering causes a shift in the structure and direction of basic flow relationships, ultimately giving rise to Layered Flow Formations and Structural Transformation.

This transformation can be categorized into four Domain-Jump typologies: Externalization, Nesting, Interlinkage, and Cross-Generation.

4. Typologies of Asset Transformation — The Emergence of Layered Structures Through Deepening of Inter-Entity Asset Movements

In this chapter, we focus on the third phase of the Evolutionary Model outlined in Chapter 3—From Flow to Layered Flows—where Inter-Entity Asset Movements deepen and evolve into structural transformations.

While this chapter primarily examines Inter-Entity Asset Transformation, it is helpful to recall that in the previous article, Structure Analysis (3): The Emergence of Surplus, we discussed Self-Contained Flow Cycles as a mechanism of generating Genuine Surplus. These can be viewed as Self-Contained Asset Transformations, which conceptually stand in contrast to the Inter-Entity transformations discussed here.

Inter-Entity Asset Transformation arises when transferred assets are redeployed or structurally altered under the control of other entities. These transformations are inherently multi-layered and dynamic, often giving rise to more complex relational structures.

To establish this contrast, we begin by briefly revisiting the structure of Self-Contained Asset Transformation—as represented by Self-Contained Flow Cycles—and then proceed to analyze Inter-Entity Asset Transformation, which we categorize further into:

- Inter-Entity Stock Transformation (Investment Flows), and

- Inter-Entity Flow Transformation (Domain Jumps).

(Illustration inserted)

4.1 Self-Contained Asset Transformation

Self-Contained Asset Transformation refers to the structural change that occurs in the first phase—Generation—of the Grand Circulation Structure of Assets. Specifically, it follows the creation of assets from nothing through Single-Entity Co-Generation.

In this Generation phase, assets are initially created from zero via Single-Entity Co-Generation. At this stage, the asset has merely begun to exist and has not yet undergone any transformation. From here, the asset may either be transferred to an external entity—marking the start of the Transfer phase—or it may undergo transformation within the same entity before any transfer takes place.

This internal transformation—Self-Contained Asset Transformation—occurs through a process in which the asset generated within the entity is deployed into its own internal flows, circulates within them, and is ultimately recovered, following the structure of a Self-Contained Flow Cycle.

(Illustration inserted)

As we have already demonstrated in the Structure Analysis (3): The Emergence of Surplus— Part 1: The Generation of Surplus, this Self-Contained Flow Cycle has the structural potential to generate Surplus.

Since both types of Self-Contained Asset Movements—Single-Entity Co-Generation and Self-Contained Flow Cycles—exclusively involve stock assets (PSAs) as their subject, Self-Contained Asset Transformation can be understood as a transformation of Stock Assets; in other words, it constitutes Self-Contained Stock Transformation.

This Self-Contained Stock Transformation can be further categorized into the following two types:

- Consumption Flow: A PSA (e.g., food, content) is deployed to recover Labor Power.

→ Transformation of PSA into Labor Power. - Operational Flow: Labor Power, PSAs, and Money are deployed to generate new assets or recover modified assets.

→ Transformation of PSAs or money through Labor Power.

(Illustration inserted)

Although Self-Contained Asset Transformation occurs at the very origin of the Grand Circulation Structure of Assets, it is also a process that can be repeated over and over again, inserted between episodes of Inter-Entity Asset Movement. Amid the complex sequence of movement → transformation → redeployment, it consistently functions as a self-contained moment of transformation, serving repeatedly as a structural trigger for Surplus Generation.

4.2 Inter-Entity Asset Transformation

In contrast, Inter-Entity Asset Transformation refers to a structural process in which an asset is transferred into a relationship with another entity, and subsequently undergoes further development or transformation at its new location.

This corresponds to Phase Three of the Evolutionary Model of Asset Transfer—Development of Multi-Layered Inter-Entity Flow Cycles [From Flow to Layered Flows]—introduced in the previous chapter, especially Investment Flows and Domain Jumps, where either the redeployment of principal assets—a process ultimately driven by the Structural Layering of Stock and Flow elements—or the Structural Layering itself serves as the point of departure.

(Illustration inserted)

In the following sections, we will examine these two structures in turn: Investment Flows as a form of Inter-Entity Stock Transformation (Section 4.2.1), and Domain Jumps as a form of Inter-Entity Flow Transformation (Section 4.2.2).

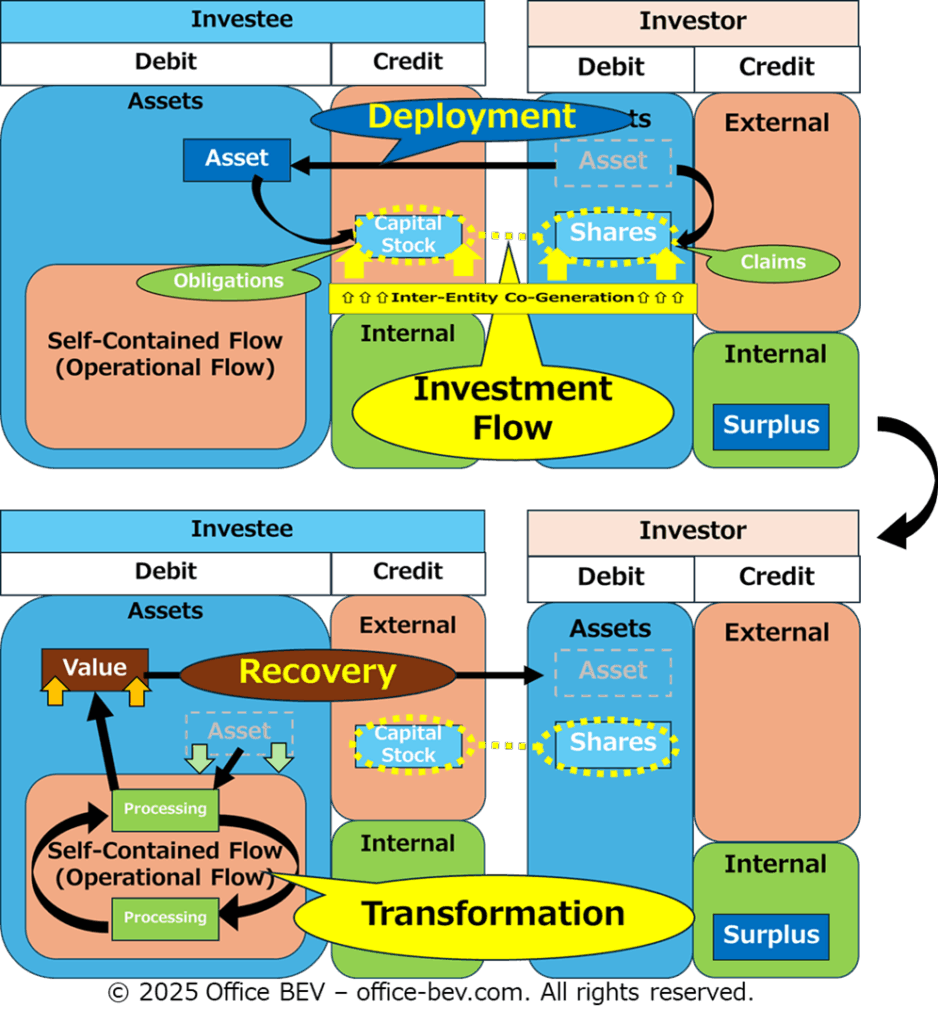

4.2.1 Inter-Entity Stock Transformation: Investment Flows

This category of transformation arises when a principal asset deployed through an inter-entity flow is subsequently transformed by the receiving entity. This structure takes the form of what we classify as Investment Flows.

Unlike Lending Flows, in which the principal asset moves back and forth without undergoing transformation, Investment Flows are designed to allow the principal asset to be transformed through internal operations or transformative processes conducted by the investee.

(1) MNY Input → Transformation → PSA Recovery

Example: Financial support for an artist (in-kind dividend type)

Investment in an artist → Creative activity by the artist (use of funds = transformation) → In-kind dividend (delivery of artwork)

The money is transformed through artistic production and returned as a transformed asset.

(2) PSA Input → Transformation → MNY or PSA Recovery

Example: In-kind contribution to a company

An investor contributes goods (PSA) as capital → The company uses these goods for operations (transformation) → The investor receives dividends (MNY) or other goods (PSA).

Here, the contributed PSA is structurally transformed through the company’s operations before being returned in a different form.

(Illustration inserted)

In both cases, the transformation of the principal asset—in physical, functional, or accounting terms—is essential. This marks a level of asset movement distinct from mere transfer, as it presupposes actual change in the nature of the deployed stock.

📌 Note: Investment Flows vs. Operational Flows — Structural Classification Across the Four Quadrants

Let us revisit the earlier example of investing in an artist.

If a patron supports the artist’s creative work and receives the resulting artwork as a dividend, this is classified as an Investment Flow—a type of Inter-Entity Flow Cycle, where the asset is deployed externally and the resulting surplus is generated by the investee.

However, if the same patron funds the artist’s work in order to display it in their own gallery and generate income, the transaction becomes part of their own Operational Flow—a type of Self-Contained Flow Cycle, where the asset is used internally for the benefit of the deploying entity.

Thus, even if the surface-level transactions appear similar, their classification across the Four Quadrants differs fundamentally:

Investment Flow = Inter-Entity × Flow vs Operational Flow = Self-Contained × Flow.

This distinction becomes clear only through an analysis of the underlying structure of asset transformation, not its superficial form.

Definitions:

Investment Flow:

An Inter-Entity Flow in which an asset is deployed to another entity for the purpose of transforming that entity’s assets.

→ The deploying entity receives a portion of the surplus that is generated by the receiving entity.

Operational Flow:

A Self-Contained Flow in which an asset is deployed within one’s own entity to transform one’s own assets.

→ The deploying entity creates value through their own activities.This distinction highlights how the classification of asset movements depends not on their superficial form, but on whether the asset transformation occurs within or across entity boundaries.

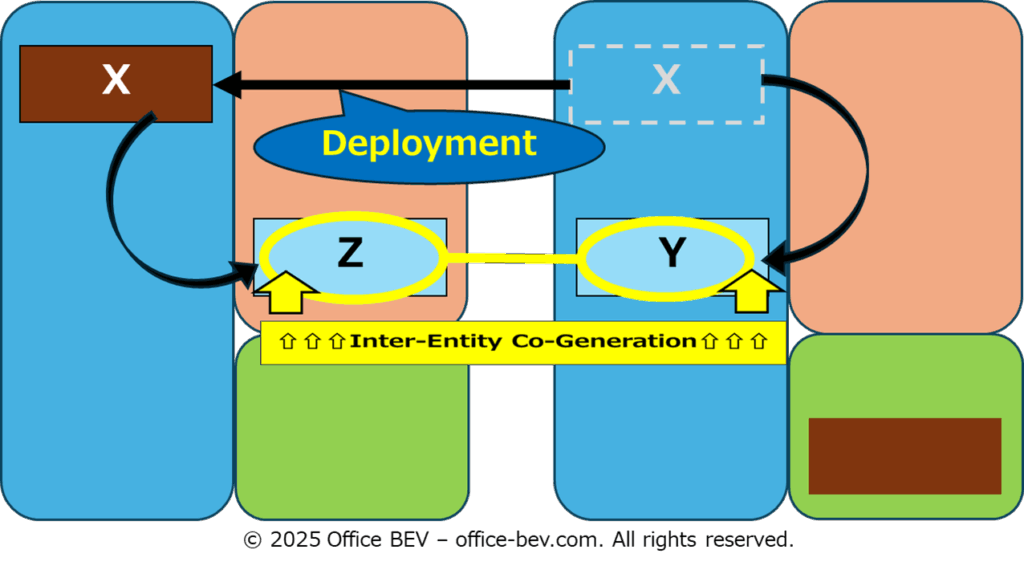

4.2.2 Inter-Entity Flow Transformation: Domain Jumps

In the previous section, we examined how a principal asset (a stock) undergoes transformation through an Investment Flow. In this section, we turn to another dimension of transformation—one in which the Inter-Entity Flow itself is structurally transformed, namely, through what we call a Domain Jump.

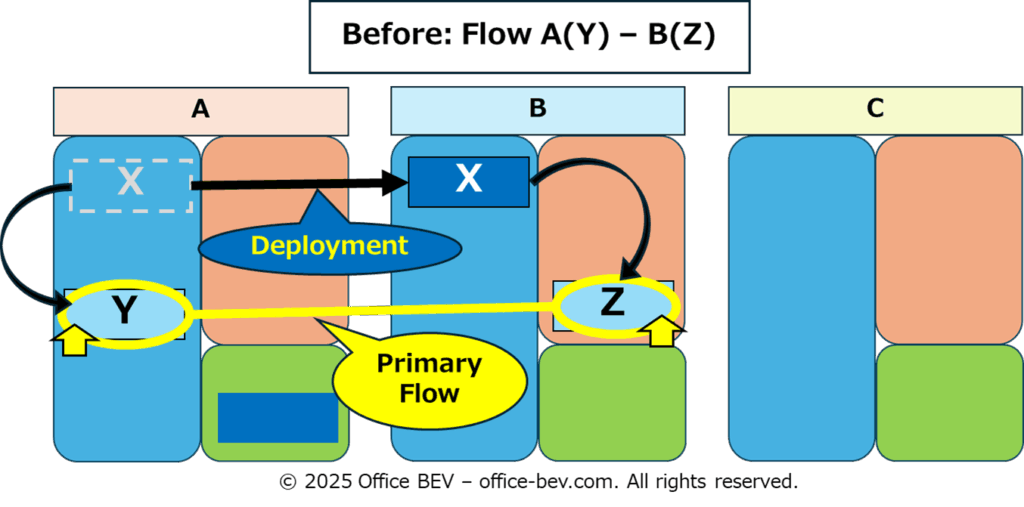

Before proceeding, let us briefly revisit the basic structure of an Inter-Entity Flow Cycle.

An Inter-Entity Flow is a relational structure in which an asset is temporarily deployed between two entities and subsequently recovered or repaid. Typical examples include Lending Flows and Investment Flows.

This flow relationship is composed of three core elements:

- X: Principal Asset

- Y: Claim

- Z: Obligation

When a flow is initiated, these elements form the following fundamental structure:

Deployment of X (Principal Asset) → Inter-Entity Co-Generation of Y (Claim) and Z (Obligation)

For example, when Entity A lends money (X) to Entity B, A acquires a repayment claim (Y) against B, while B assumes a repayment obligation (Z) to A. In this way, the deployment of a principal asset gives rise to a pair of claim and obligation—a Claim–Obligation Flow—a structure we refer to as Inter-Entity Co-Generation.

(Illustration inserted: Deployment of X in a flow ⇒ Inter-Entity Co-Generation of Y / Z)

In this section, we analyze what occurs when the elements of a primary flow (X, Y, Z) are structurally layered with the asset elements of a secondary relationship (X’, Y’, Z’, and Stock), and whether such layering triggers a Domain Jump.

The result of this structural simulation is summarized in the following matrix:

| Stock | X’ (Principal) | Y’ (Claim) | Z’ (Obligation) | |

|---|---|---|---|---|

| X (Principal) | NA | (3) Interlinkage | NA | NA |

| Y (Claim) | (1) Externalization | (2) Nesting | NA | (4) Cross-Generation |

| Z (Obligation) | (1) Externalization | NA | (4) Cross-Generation | NA |

Note: “NA (Not Applicable)” indicates that layering these particular elements does not produce any structural transformation.

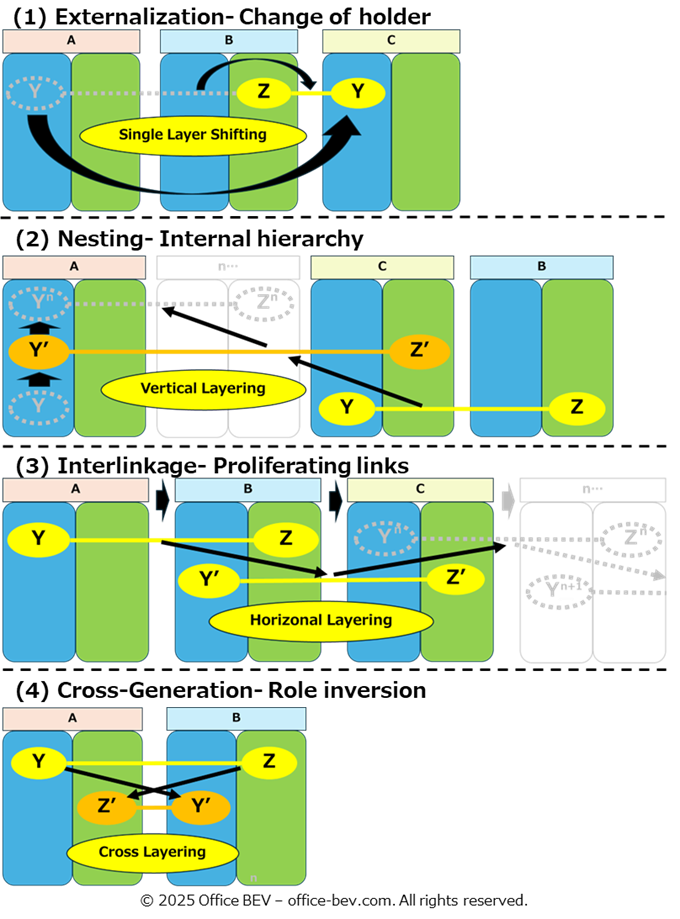

From this simulation, we identify four distinct typologies of Domain Jumps. These are summarized below, with each type described in terms of:

① the structural layering that triggers the Domain Jump, ② the resulting flow structure after the jump, and ③ the transformation of entity involvement.

Typologies of Domain Jumps (as observed in Inter-Entity Flow Transformation)

| Type | ① Structural Layering | ② Flow Structure | ③ Entity Involvement |

|---|---|---|---|

| (1) Externalization | Flow ≡ Stock Layering (Claim-Exchange) | Shifted Flow (Single-Layer) | Entity Shift (change of holder) |

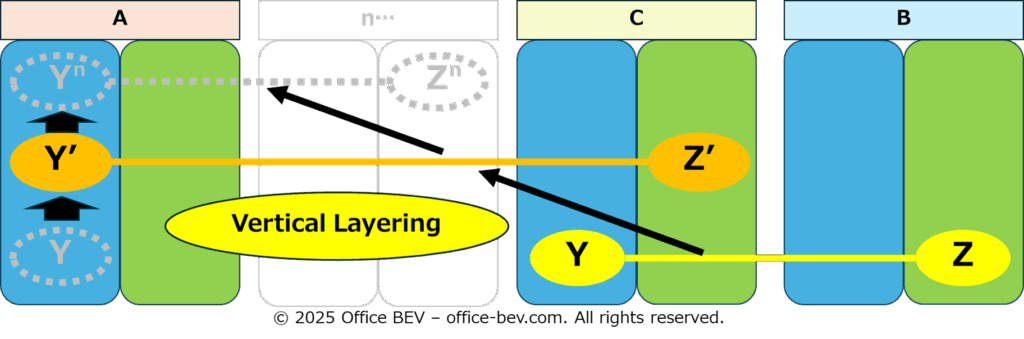

| (2) Nesting | Flow ≡ Stock Layering (Claim-Deployment) | Nested Flows (Vertical Layering) | Intra-Entity Layering (internal hierarchy) |

| (3) Interlinkage | Stock ≡ Stock’ Layering | Cascade Flows (Horizontal Layering) | Inter-Entity Chain Expansion (Proliferating Links) |

| (4) Cross-Generation | Flow ≡ Flow’ Layering | Reverse Flows (Cross Layering) | Reversal of Entity Relations (role inversion) |

From this table, we see how different combinations of stock and flow elements, through Domain Jumps, give rise to various layered flow structures and transformations in entity relationships.

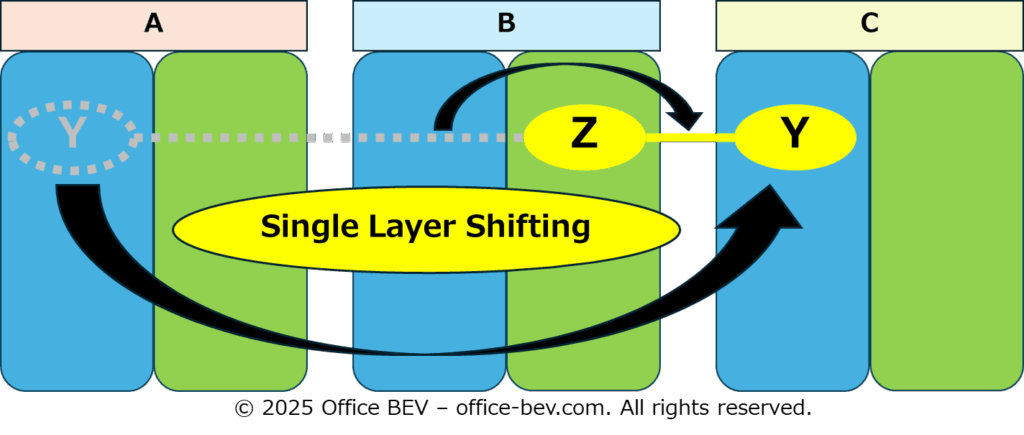

Inter-Entity Flow Transformation progresses through (1) Externalization → (2) Nesting → (3) Interlinkage → (4) Cross-Generation, with each stage introducing higher structural entanglement—whether through Vertical Layering, Horizontal Expansion, or Reversed Flow Dynamics—resulting in a gradual rise in overall structural complexity.

In the following sections, we will examine each of these typologies in detail, using diagrams and examples to illustrate their distinct mechanisms.

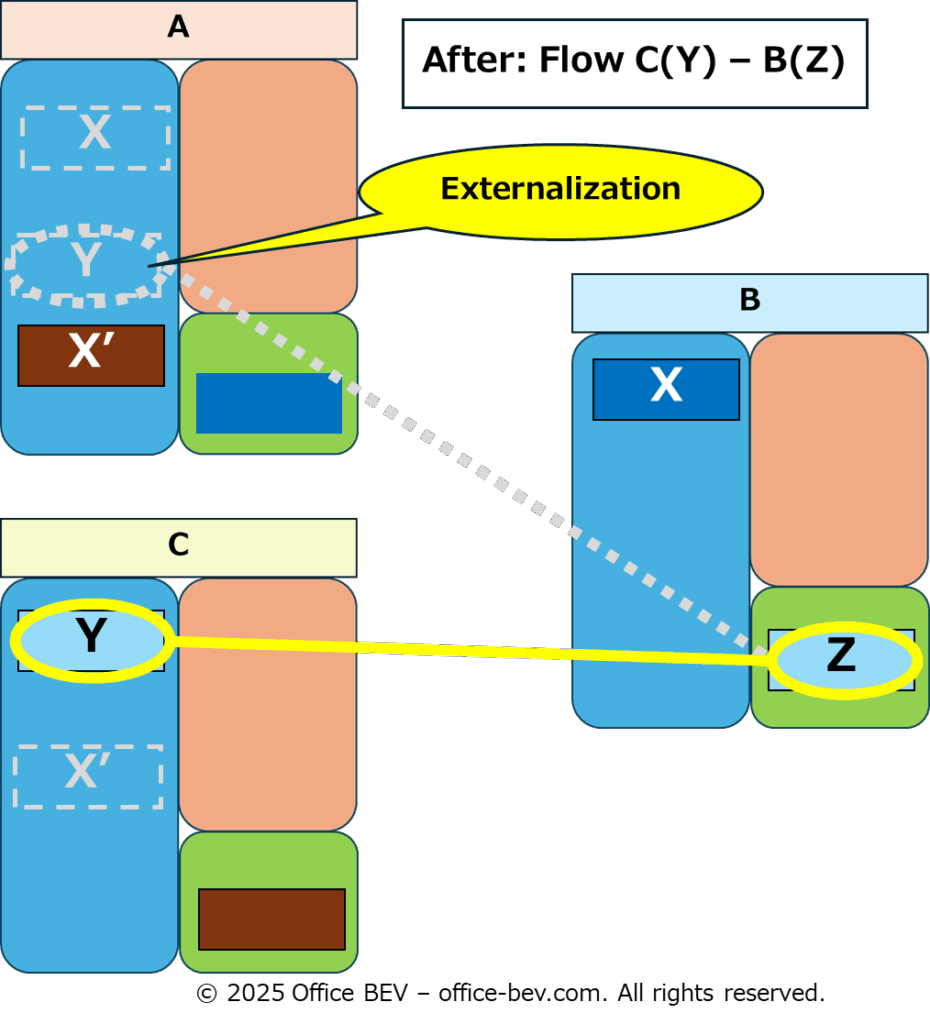

(1) Externalization

- Structural Layering: Flow ≡ Stock Layering (Claim-Exchange)

- Flow Structure: Shifted Flow (Single-Layer)

- Entity Involvement: Entity Shift (change of holder)

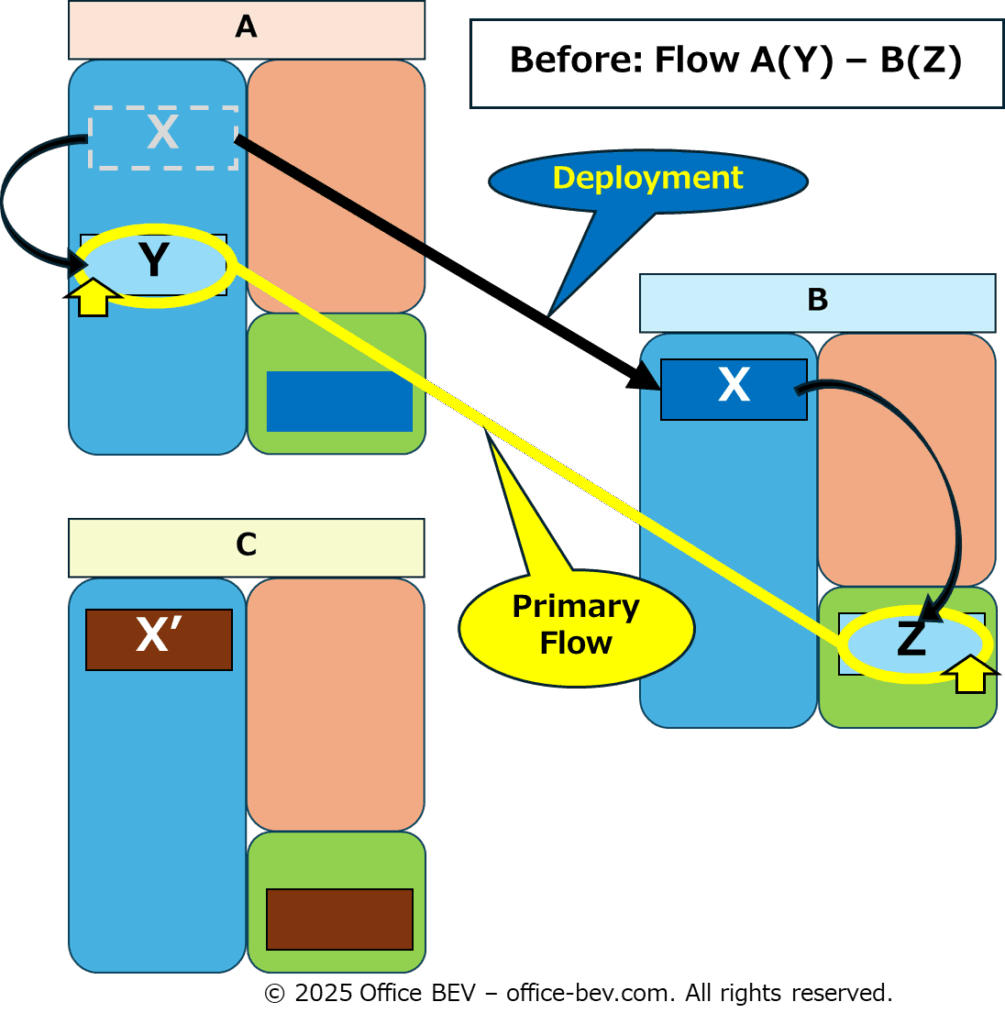

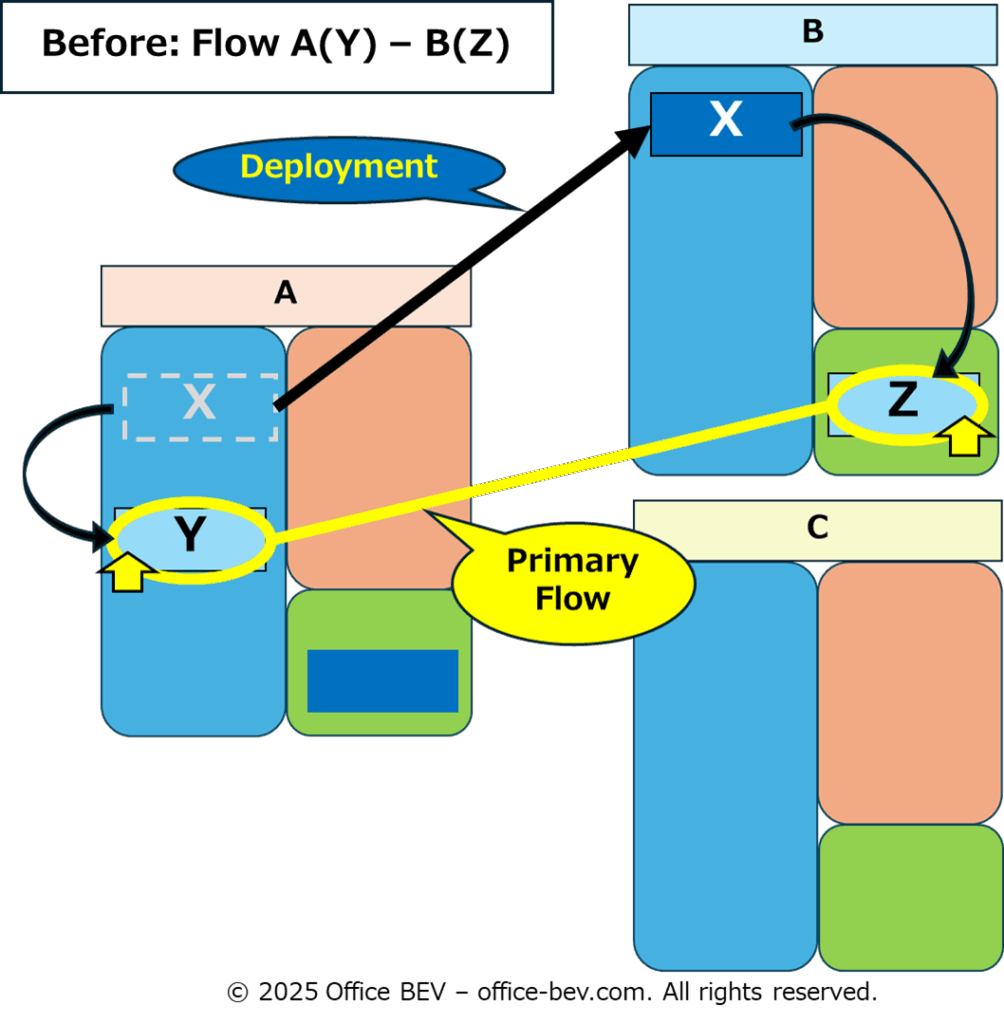

The first typology, Externalization, refers to a structure in which the claim or obligation that constitutes an Inter-Entity Flow is transferred to an external third party in the form of a Stock Asset.

Example: A sells the shares of Company B (Y) that A holds to C.

- Entities: A, B, C

- Primary Flow (A–B) Elements:

X = Principal for the share purchase,

Y = A’s claim (shares of Company B),

Z = B’s obligation (issuer of shares). - Secondary Flow (C–B) Elements:

X’ = Principal for the share purchase,

Y = C’s claim (shares of Company B),

Z = B’s obligation (issuer of shares).

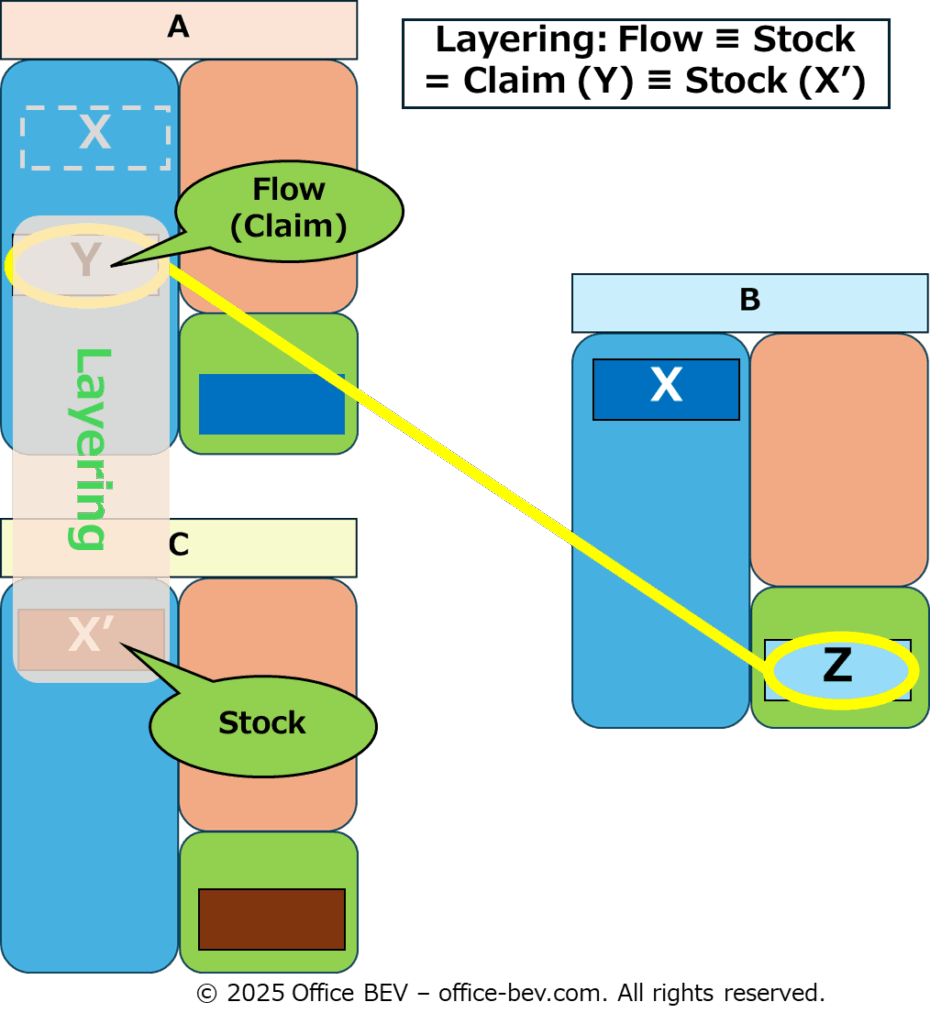

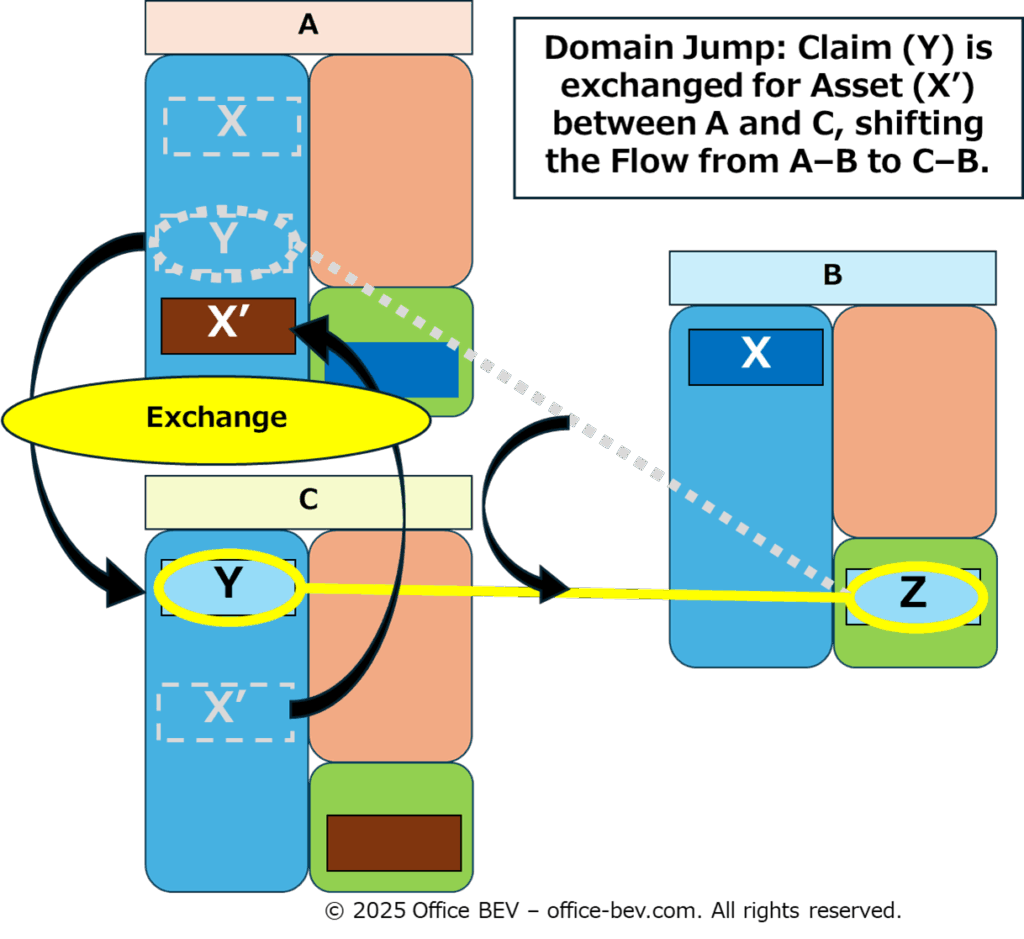

Before: Flow A(Y) – B(Z)

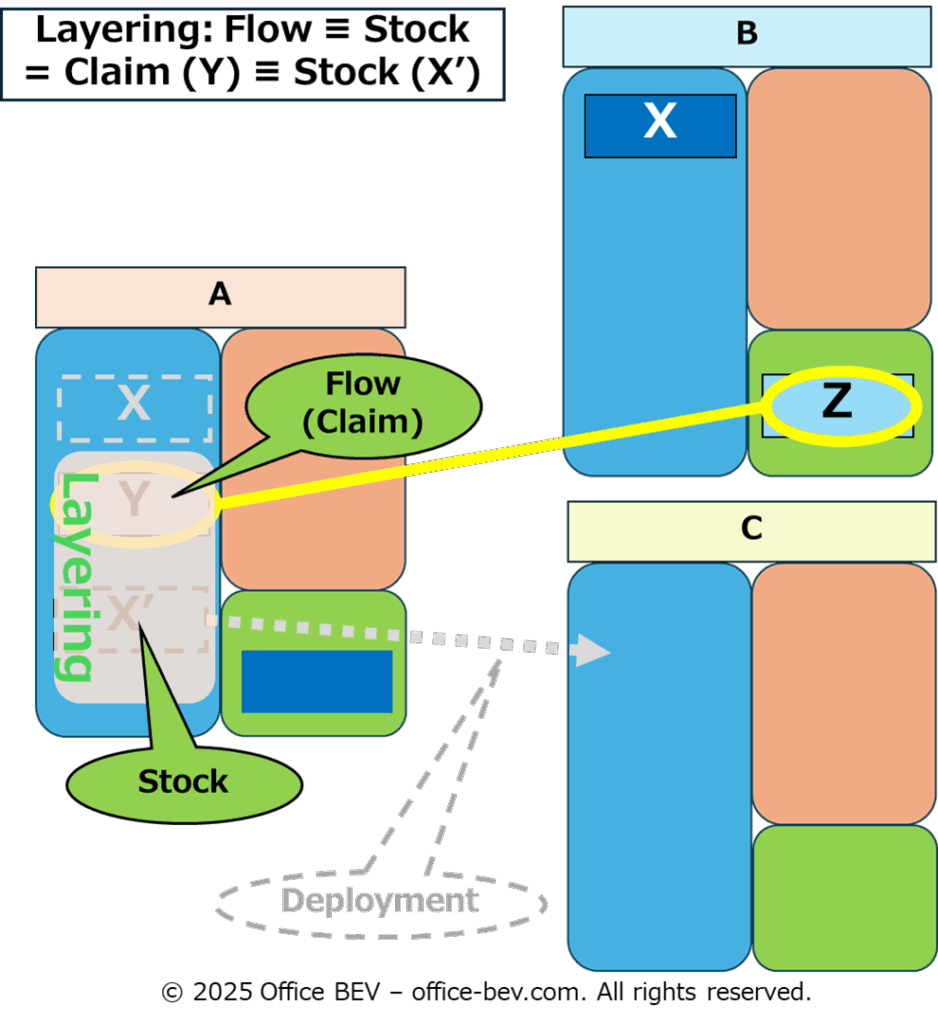

Layering: Flow ≡ Stock = Claim (Y) ≡ Stock (X’)

Domain Jump: Claim (Y) is exchanged for Asset (X’) between A and C, shifting the Flow from A–B to C–B.

After: Flow C(Y) – B(Z)

(Illustration to be inserted)

- In the Inter-Entity Flow Cycle between A and B, A deploys the principal asset X to B to purchase the shares, thereby triggering Inter-Entity Co-Generation of the flow A(Y) – B(Z), where Y (claim) is held by A and Z (obligation) is held by B (Before).

- By applying Structural Layering of Claim Y with Stock Asset X’ (Flow ≡ Stock Layering), A engages in an exchange (selling Y for X’) with an external third party C.

- This exchange constitutes a Domain Jump, through which the original Inter-Entity Flow (Y–Z) between A and B is shifted, without altering its single-layer structure, to a new Flow between C and B. As a result, the holder of claim Y changes from A to C, achieving Externalization from A’s perspective.

Note: The same logic applies to obligations as well. Externalization via a Domain Jump can occur through Structural Layering of an obligation (a flow element) with a stock asset, for example in cases of “assumption of debt,” among other possible structures.

(2) Nesting

Structural Layering: Flow ≡ Stock Layering (Claim-Deployment)

Flow Structure: Nested Flows (Vertical Layering)

Entity Involvement: Intra-Entity Layering (internal hierarchy)

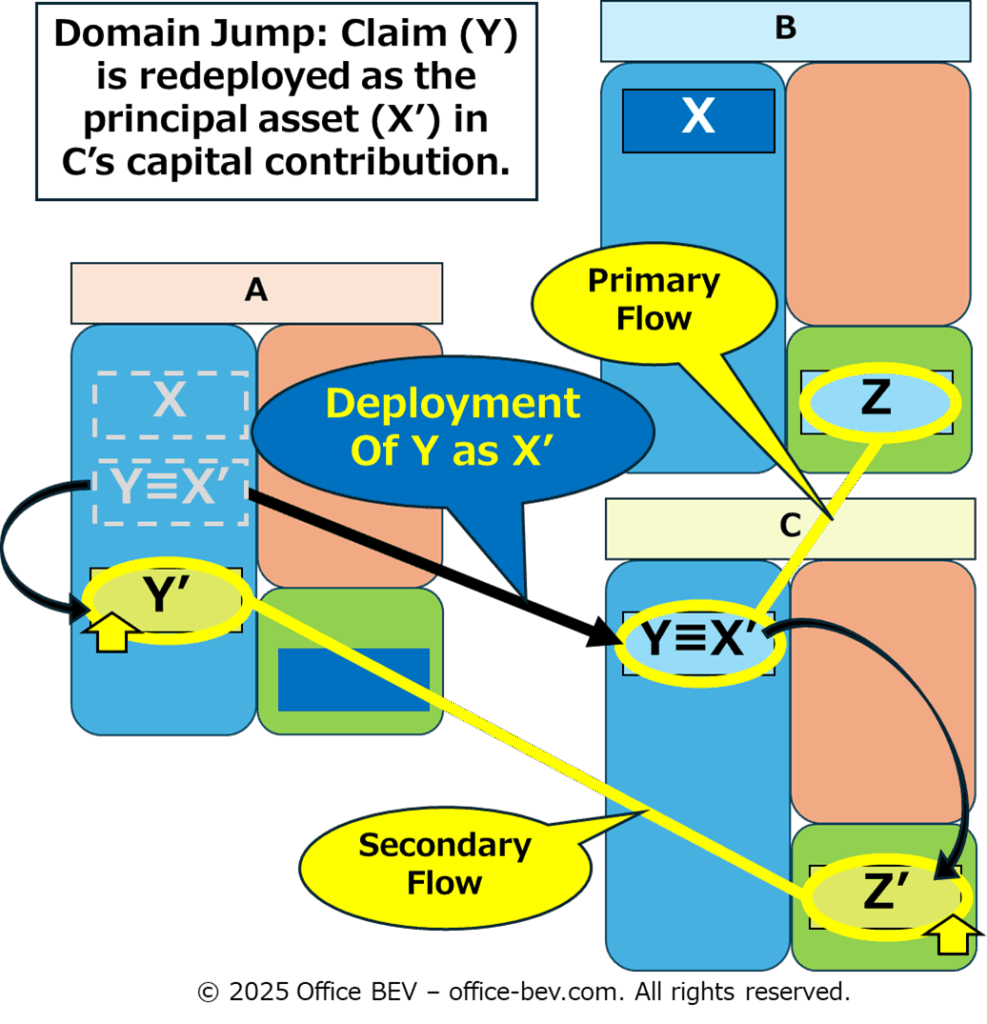

The second typology, Nesting, refers to a structure in which a Claim that constitutes an Inter-Entity Flow is redeployed as the Principal Asset of another Inter-Entity Flow, creating a Multi-Layered Structure of Flows—an “Nested” configuration.

Example: A contributes the shares of Company B (Y) that A holds as in-kind capital (X’) to establish a new company C.

・Entities: A, B, C

・Primary Flow (A–B) Elements:

X= Principal for the share purchase,

Y = A’s claim (shares of Company B),

Z = B’s obligation (issuer of shares).

・Secondary Flow (A–C) Elements:

X’ = Contributed principal = Y,

Y’ = A’s claim (equity in Company C),

Z’ = C’s obligation (recipient of capital contribution).

Before: Flow A(Y) – B(Z)

Layering: Flow ≡ Stock = Claim (Y) ≡ Stock (X’)

Domain Jump: Claim (Y) is redeployed as the principal asset (X’) in C’s capital contribution.

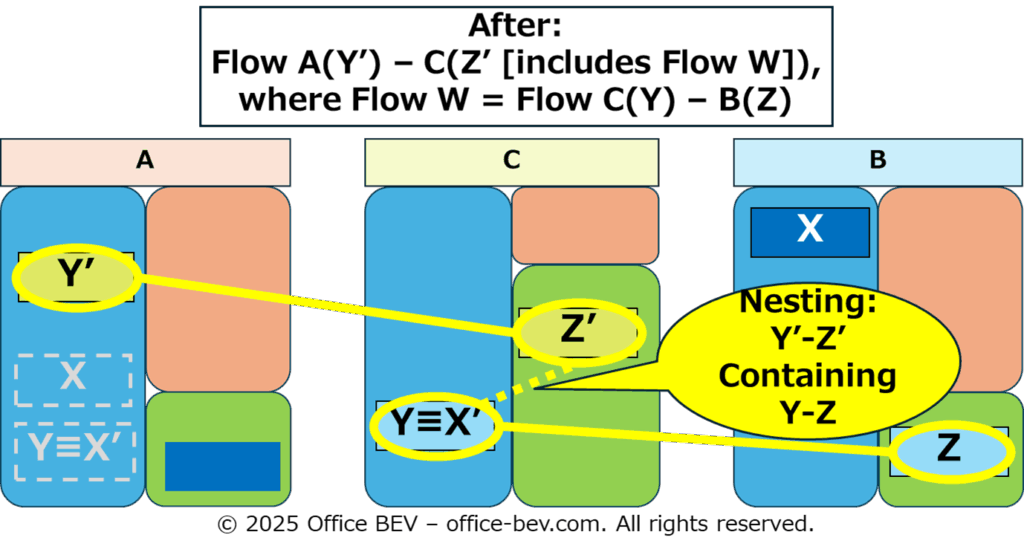

After: Flow A(Y’) – C(Z’ [includes Flow W]), where Flow W = Flow C(Y) – B(Z)

(Illustration to be inserted)

・In the Inter-Entity Flow Cycle between A and B, A holds the claim Y (shares of Company B) as a result of the principal deployment X, forming the Primary Inter-Entity Flow A(Y) – B(Z) (Before).

・By applying Structural Layering of Claim Y with Principal Asset X’ (Flow ≡ Stock Layering), A redeploys Y as an in-kind capital contribution to Company C.

・This Structural Layering triggers a Domain Jump, which initiates a Secondary Inter-Entity Flow A(Y’) – C(Z’), thereby creating a Nested Structure (Nesting) that encapsulates the Primary Flow A(Y) – B(Z) within the Secondary Flow, characterized by Vertical Layering and an Internal Hierarchy within the entity.

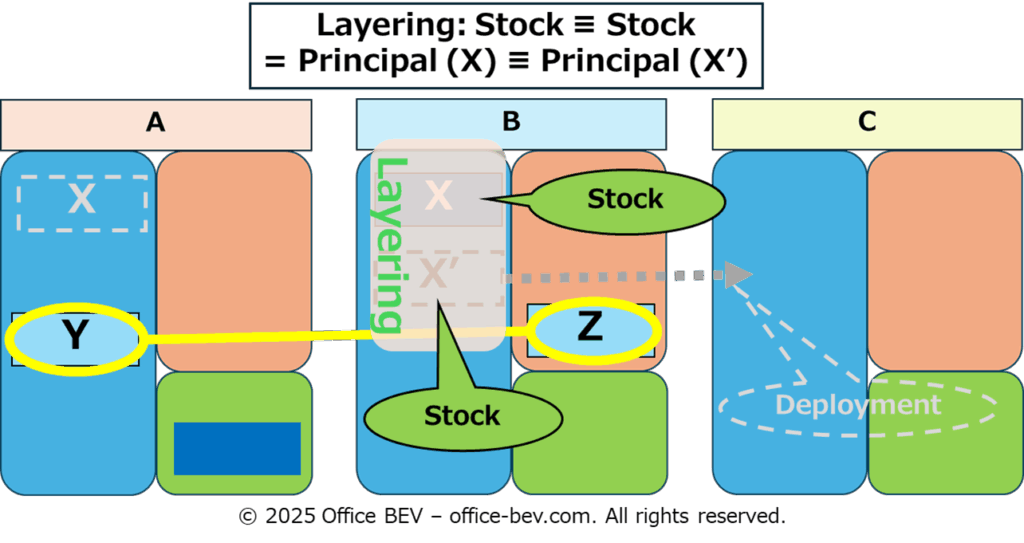

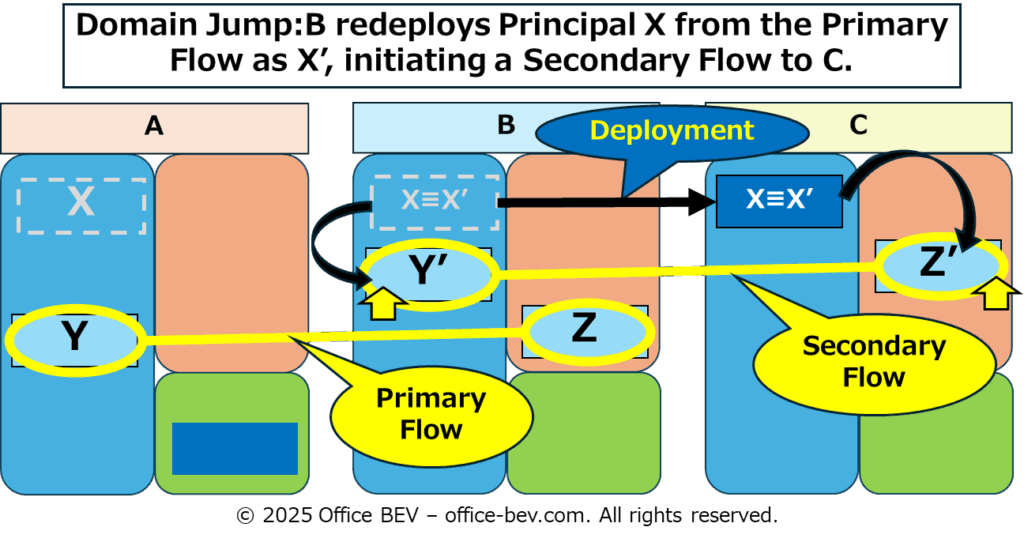

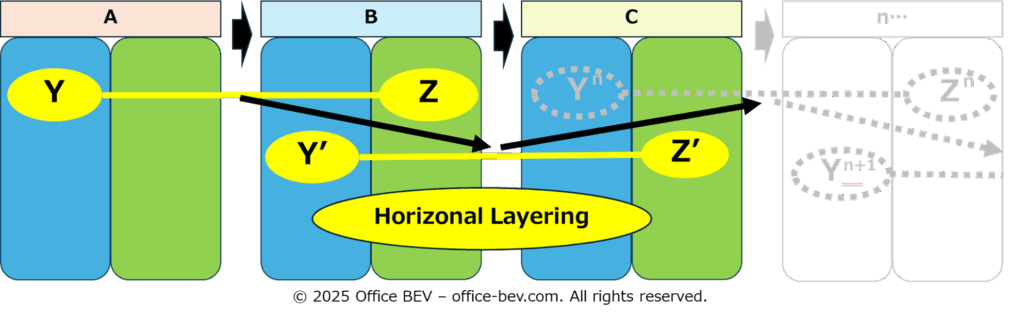

(3) Interlinkage

Structural Layering: Stock ≡ Stock’ Layering

Flow Structure: Cascade Flows (Horizontal Layering)

Entity Involvement: Inter-Entity Chain Expansion (Proliferating Links)

The third typology, Interlinkage, refers to a structure in which a Principal Asset deployed in one Inter-Entity Flow is redeployed as the Principal Asset of another Inter-Entity Flow, thereby giving rise to an inter-flow link that can further proliferate horizontally, forming a chain-like structure of Cascade Flows.

Example: B redeploys the Lending Principal X, borrowed from A, as Principal X’ for a new Lending Flow to C.

・Entities: A, B, C

・Primary Flow (A–B) Elements:

X = Lending principal,

Y = A’s claim (loan receivable from B),

Z = B’s obligation (repayment to A).

・Secondary Flow (B–C) Elements:

X’ = Lending principal = X,

Y’ = B’s claim (loan receivable from C),

Z’ = C’s obligation (repayment to B).

Before: Flow A(Y) – B(Z)

Layering: Stock ≡ Stock’ = Principal (X) ≡ Principal (X’)

Domain Jump:B redeploys Principal X from the Primary Flow as X’, initiating a Secondary Flow to C.

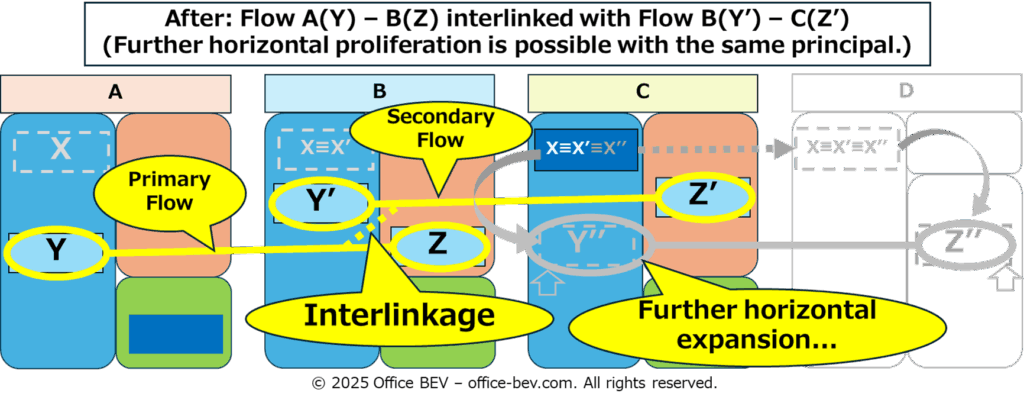

After: Flow A(Y) – B(Z) interlinked with Flow B(Y’) – C(Z’)

(Further horizontal proliferation is possible with the same principal.)

(Illustration to be inserted)

- In the Inter-Entity Flow Cycle between A and B, B holds the Lending Principal X received from A (Before).

- By applying Structural Layering of Principal X with Principal X’ (Stock ≡ Stock’ Layering), B initiates a Domain Jump by redeploying X as X’ into a Secondary Lending Flow to C.

- As a result, the Primary Flow A–B is interlinked with the Secondary Flow B–C, forming a chain structure that can horizontally expand into a sequence of Cascade Flows.

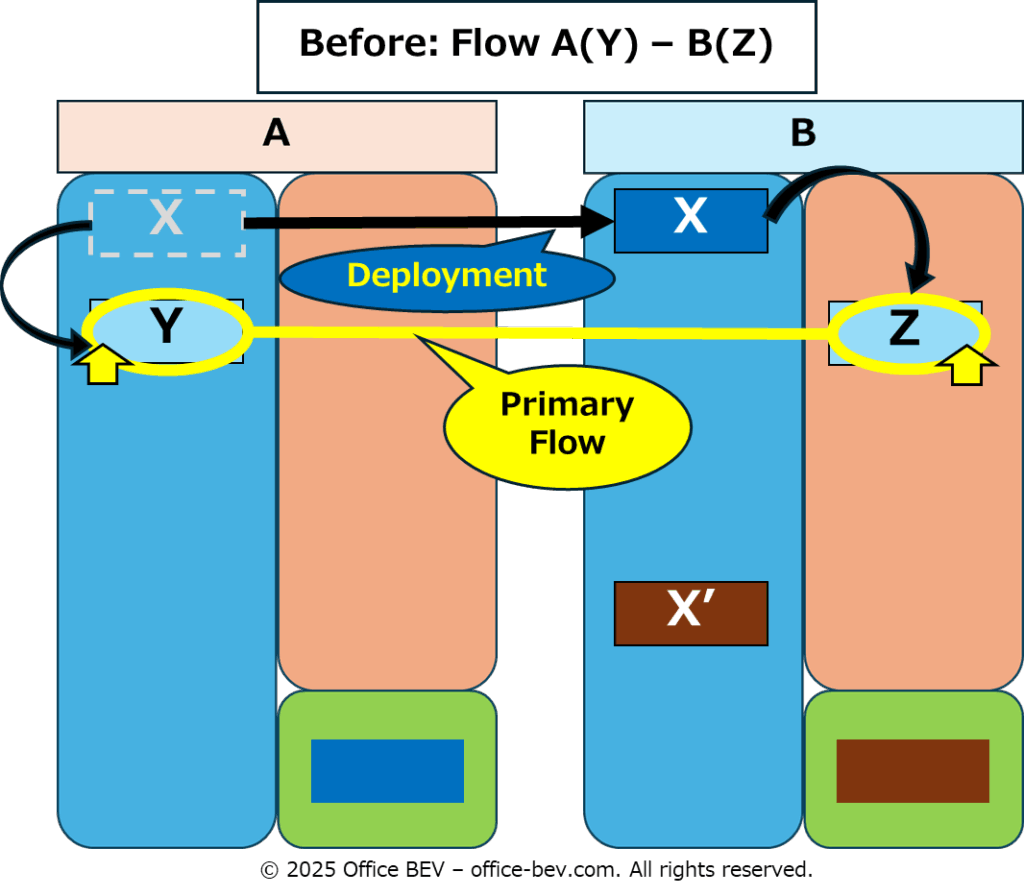

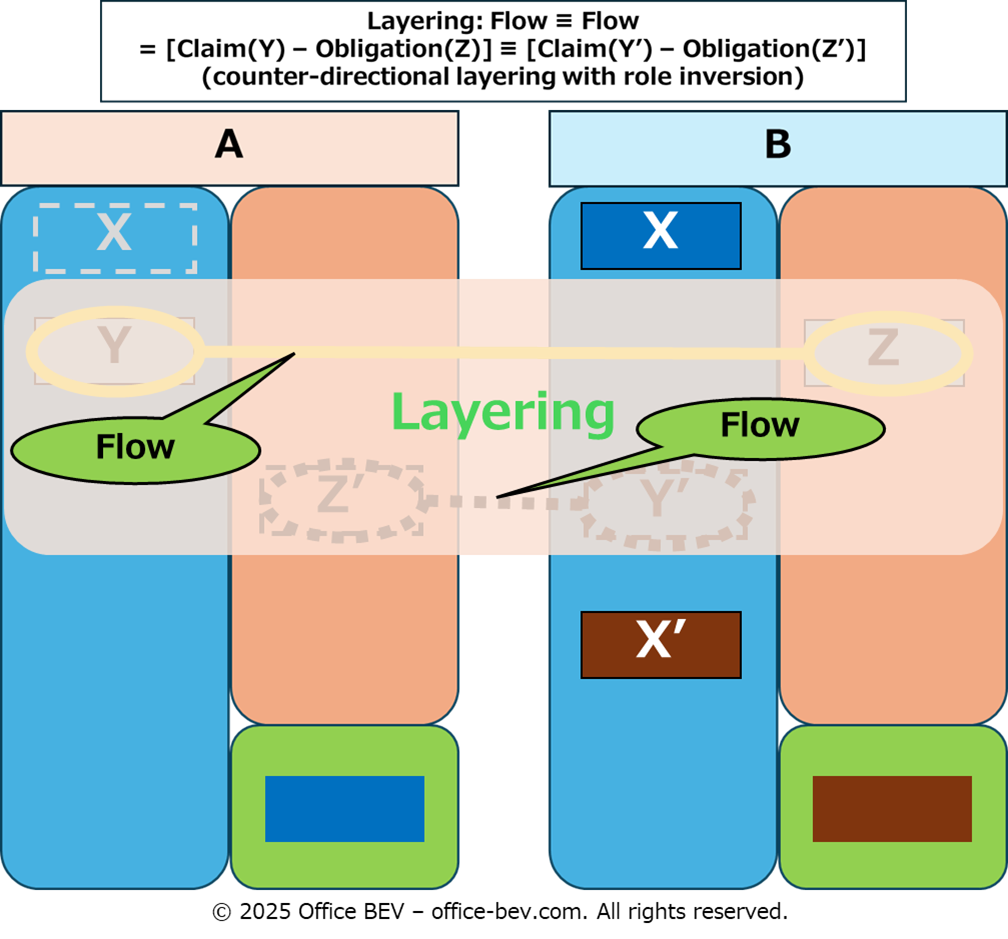

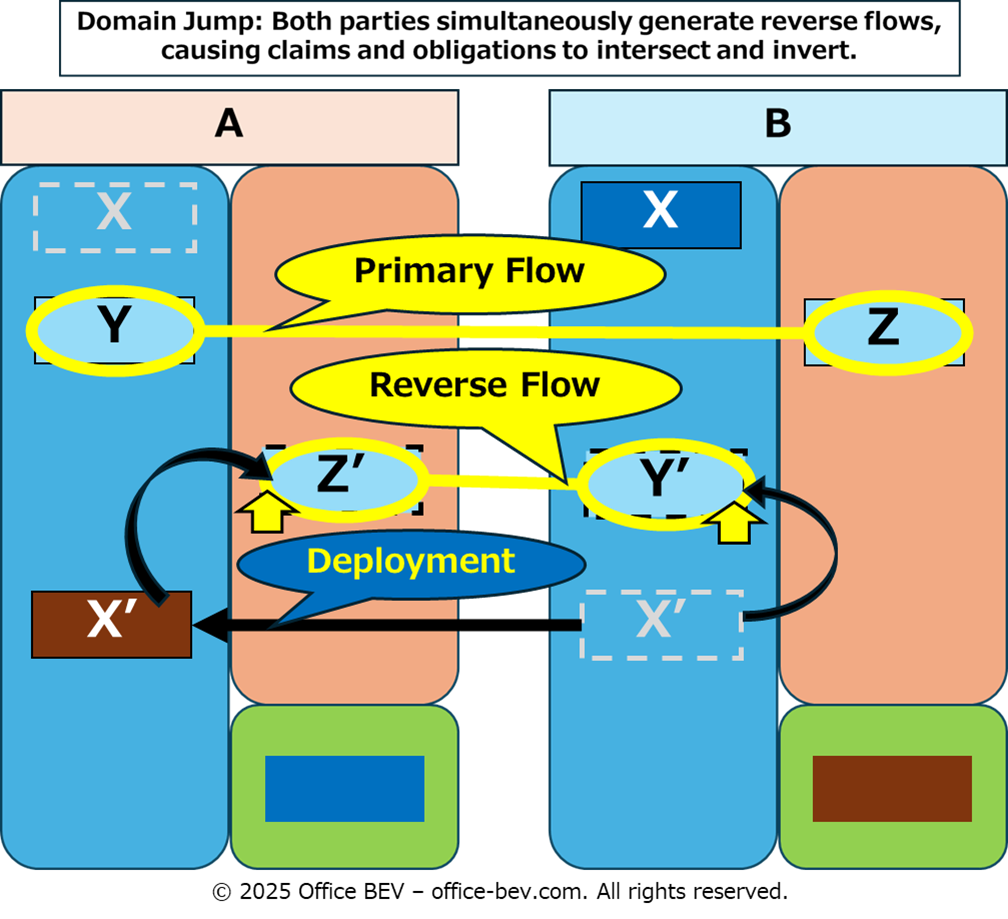

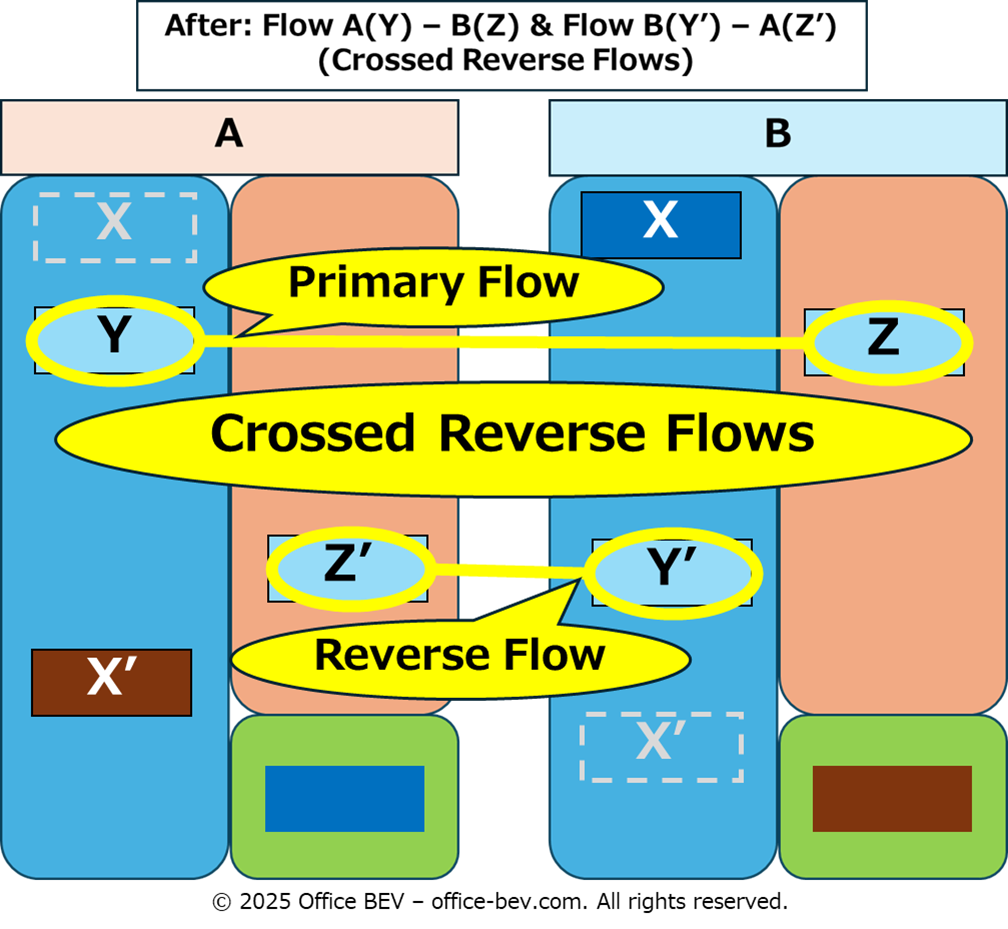

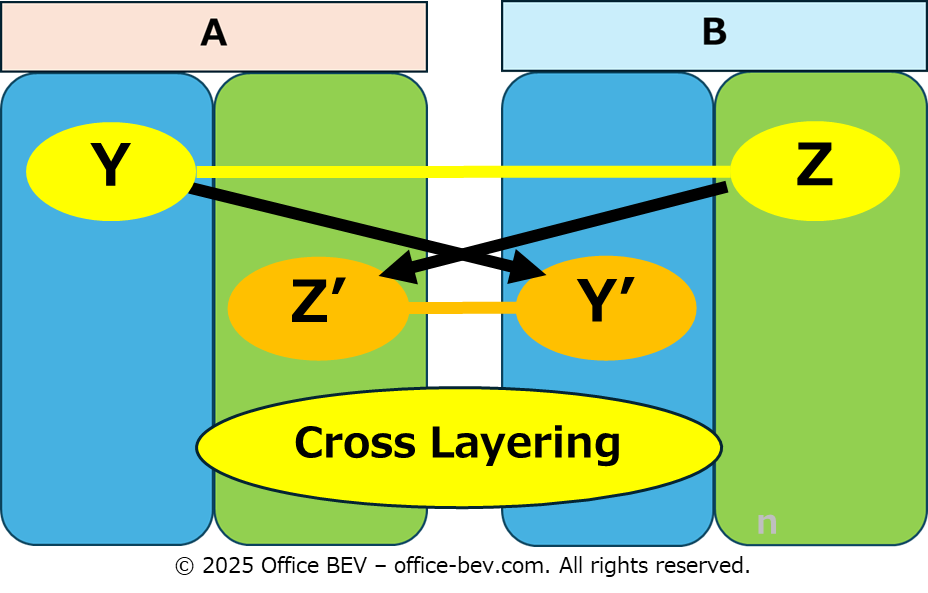

(4) Cross-Generation

Structural Layering: Flow ≡ Flow’ Layering

Flow Structure: Reverse Flows (Cross Layering)

Entity Involvement: Reversal of Entity Relations (role inversion)

The fourth typology, Cross-Generation, refers to a structure in which a new Inter-Entity Flow with reversed claims and obligations is simultaneously generated against an existing Inter-Entity Flow, resulting in a pair of parallel flows that cross and invert the entity relations.

Example: A mutual lending agreement between Company A and Company B.

- Entities: A, B

- Primary Flow (A–B) Elements:

X = Lending Principal (A → B),

Y = A’s claim (repayment from B),

Z = B’s obligation (repayment to A). - Secondary Flow (B–A) Elements:

X’ = Lending Principal (B → A),

Y’ = B’s claim (repayment from A),

Z’ = A’s obligation (repayment to B).

Before: Flow A(Y) – B(Z)

Layering: Flow ≡ Flow’ = [Claim(Y) – Obligation(Z)] ≡ [Claim(Y’) – Obligation(Z’)] (counter-directional layering with role inversion)

Domain Jump: Both parties simultaneously generate reverse flows, causing claims and obligations to intersect and invert.

After: Flow A(Y) – B(Z) & Flow B(Y’) – A(Z’) (Crossed Reverse Flows)

(Illustration to be inserted)

- In the Inter-Entity Flow Cycle between A and B, A and B mutually recognize each other as both claim holder and obligor (via Flow ≡ Flow’ Structural Layering).

- As a result, the original Inter-Entity Flow A(Y) – B(Z) and a reversed Flow B(Y’) – A(Z’) are simultaneously generated, forming a structure of intersecting reverse flows (Cross-Generation).

Summary – Four Typologies of Domain Jumps in Inter-Entity Flow Transformation

| Type | ① Structural Layering | ② Flow Structure | ③ Entity Involvement |

|---|---|---|---|

| (1) Externalization | Flow ≡ Stock Layering (Claim-Exchange) | Shifted Flow (Single-Layer) | Entity Shift (change of holder) |

| (2) Nesting | Flow ≡ Stock Layering (Claim-Deployment) | Nested Flows (Vertical Layering) | Intra-Entity Layering (internal hierarchy) |

| (3) Interlinkage | Stock ≡ Stock’ Layering | Cascade Flows (Horizontal Layering) | Inter-Entity Chain Expansion (Proliferating Links) |

| (4) Cross-Generation | Flow ≡ Flow’ Layering | Reverse Flows (Cross Layering) | Reversal of Entity Relations (role inversion) |

5. Conclusion — Assets as Structures That Interlink, Layer, and Transform

Assets undergo Movement—the cycle of Generation, Transfer, and Extinction.

These movements, when interlinked through Structural Layering and Domain Jumps, result in Structural Transformation.

In this article, we have explored how assets connect, evolve, and circulate within complex relational structures. We approached this question through the lens of the Grand Circulation Structure of Assets—Generation, Transfer, and Extinction—while focusing on the structural transformation processes embedded in the Transfer phase.

Within the Transfer phase, we confirmed the Evolutionary Model of Asset Transfer, which traces the development from Single-Entity to Inter-Entity, from Stock to Flow, and finally from Flow to Layered Flows, where transformation takes place.

In this phase of Asset Transformation, we observed two primary forms: Stock Transformation and Flow Transformation.

The latter arises when Structural Layering of Flow Elements triggers Domain Jumps, which in turn drive the creation of Layered Flow Structures that enable deeper and more diversified forms of transformation.

These layered flows reveal increasing structural complexity, progressing through:

Entity Shift (Externalization), Internal Hierarchy (Nesting), Proliferating Links (Interlinkage), and Role Inversion (Cross-Generation).

(Insert the overall illustration here)

From this perspective, assets should not be viewed merely as objects or conventional claims, but as relational structures—emerging within flows, evolving through layered structures and interconnections, and continually transforming their meaning and position within the broader system of circulation.

This perspective forms the foundation for the next article, Structure Analysis (5): The Nature of Surplus, where we will examine whether these interlinked and layered asset structures genuinely generate surplus as a whole, or merely represent structural redistribution or reconfiguration. This analysis will also prepare the ground for our forthcoming discussion on the Nature of Money and its role in recognizing surplus.