Structure of This Article

This article proceeds as follows:

1. Introduction – What Does It Mean for an Asset to Increase?

2. Where Does Surplus Arise?

2.1 Self-Contained Stock Change — Can Surplus Arise Within a Single Entity?

2.1.1 Pure Stock Assets (Accumulated Assets)

2.1.2 Stock-like Flow Assets (Structurally Created Assets)

(1) Securitized Claims

(2) Fictionally Created Claims

2.2 Inter-Entity Stock Transfers — Can Surplus Arise Through Asset Movement?

(1) Unilateral Transfer — One-Way Movement Without Return

(2) Bilateral Stock Transfer — Two-Way Movement Through Exchange

2.3 Self-Contained Flow Cycles — Can Internal Deployment Generate Surplus?

2.4 Inter-Entity Flow Cycles — Can Surplus Arise Through Relational Flows?

(1) Lending Flow — Principal and Interest

(2) Investment Flow — Capital and Returns

3. Only One Path Leads to Surplus

3.1 Asset Movement Types That Generate Surplus

3.2 Core Components and Cycles of Surplus

4. Conclusion — Surplus Emerges Only in Self-Contained Flow Cycles

1. Introduction – What Does It Mean for an Asset to Increase?

In the previous post, we introduced a framework that classifies asset movements into eight types across four quadrants—defined by two axes: Single-Entity vs. Inter-Entity, and Stock vs. Flow.

In this post, we shift our focus from how assets move to a deeper question:

Can assets actually increase?

When assets are merely exchanged or circulated, the total value in the system doesn’t change. But what about cases where the outcome exceeds the input—where a surplus appears?

To explore this, we will examine each of the eight movement types and ask:

Which ones truly generate surplus—and which ones only move existing value around?

2. Where Does Surplus Arise?

When assets move, do they simply change hands—or do they generate surplus?

To explore this question, we’ll examine the eight structural types of asset movement, one by one, and ask whether each has the potential to produce surplus—defined here as an outcome that exceeds the value of what was originally deployed.

2.1 Self-Contained Stock Change — Can Surplus Arise Within a Single Entity?

Self-Contained Stock Change refers to changes in stock assets that occur entirely within one balance sheet.

In this section, we focus on Single-Entity Co-Generation—the emergence of new assets within a single BS—and examine whether such changes can give rise to surplus.

There are two primary types of asset emergence in this category—pure stock assets and stock-like flow assets.

The latter can be further divided into two subcategories: securitized claims and fictionally created claims.

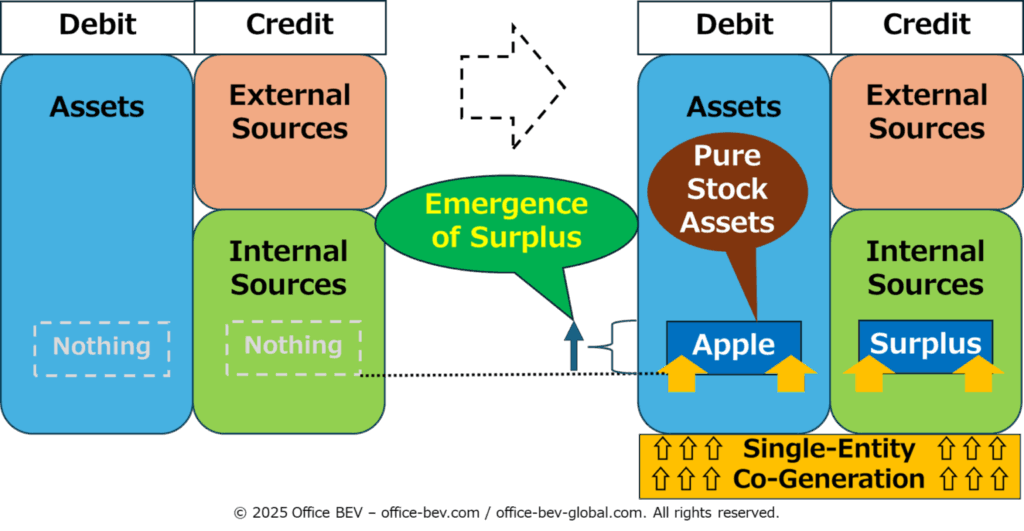

2.1.1 Pure Stock Assets (Accumulated Assets)

These are assets obtained directly from nature—without any labor, exchange, or contractual arrangement.

They are passively acquired and possess tangible, definite value at the moment they appear on the balance sheet.

Example: Picking apples from a tree that grew spontaneously in one’s yard.

As shown in the diagram, the balance sheet initially contains nothing. But once the apple is picked, both the asset (Apple) and a corresponding surplus (Internal Sources) are created through Single-Entity Co-Generation.

Since nothing was given up to obtain it, the apple represents a net gain—a clear case of surplus.

2.1.2 Stock-like Flow Assets (Structurally Created Assets)

These assets are created via Single-Entity Co-Generation, but their value depends on future relational use.

They are structurally prepared to enter into external flow but currently remain within the balance sheet.

This type is further divided into two subcategories: (1) Securitized Claims, and (2) Fictionally Created Claims.

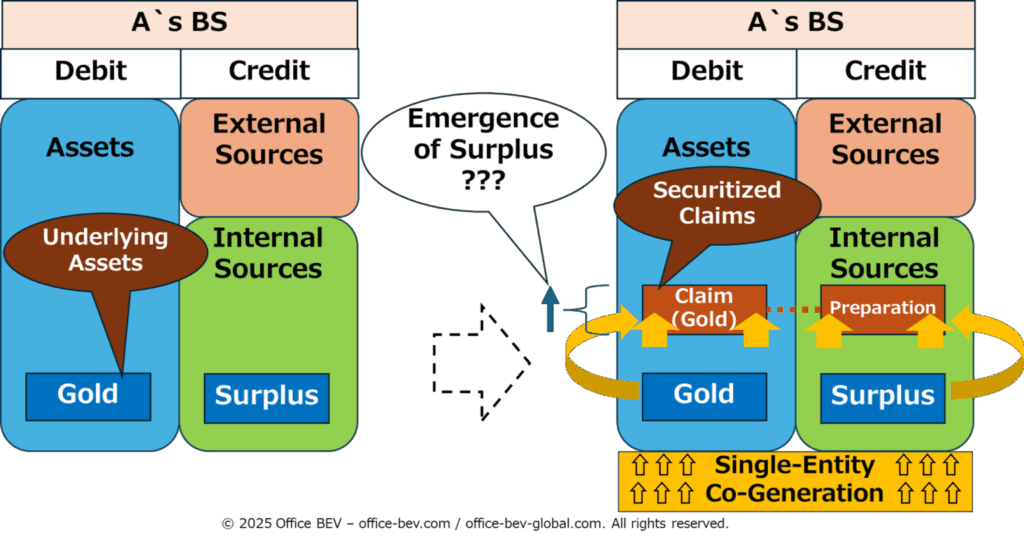

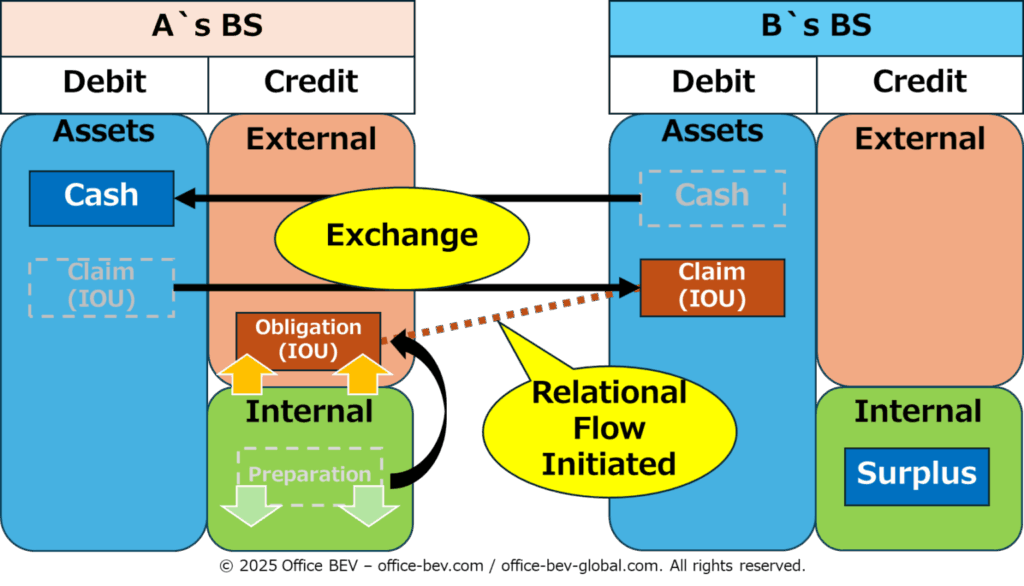

(1) Securitized Claims

These are claims created against an underlying asset (the principal) in anticipation of future transfer.

The asset already exists (e.g., gold), and the claim formalizes the promise to deliver it at a later time.

Example: Creating a claim to deliver gold that one already owns

Let’s say A holds gold.

Instead of delivering it now, A creates a claim — a formal promise to deliver it later.

This claim becomes a new asset on A’s balance sheet: it can be transferred, exchanged, or sold.

Let’s walk through the steps of this securitization process using A’s balance sheet as our frame.

Step-1: Single-Entity Co-Generation on A’s BS

Single-Entity Co-Generation can create new value in the form of a future claim/obligation flow, generated from an underlying asset (such as gold).

Debit: Claim to receive gold

Credit/Internal Sources: Preparation (indicating readiness for external flow — a placeholder for a future obligation)

This structure does not yet represent an external obligation—it simply prepares the balance sheet for potential external engagement.

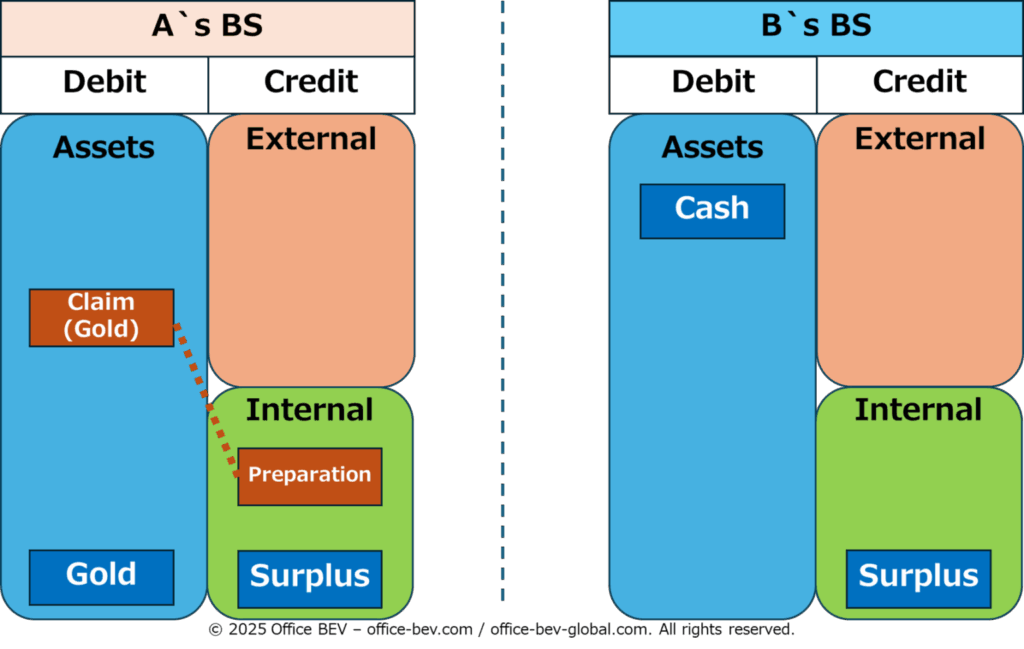

Step-2: Preparing for the exchange

B prepares to purchase the Claim(gold) from A.

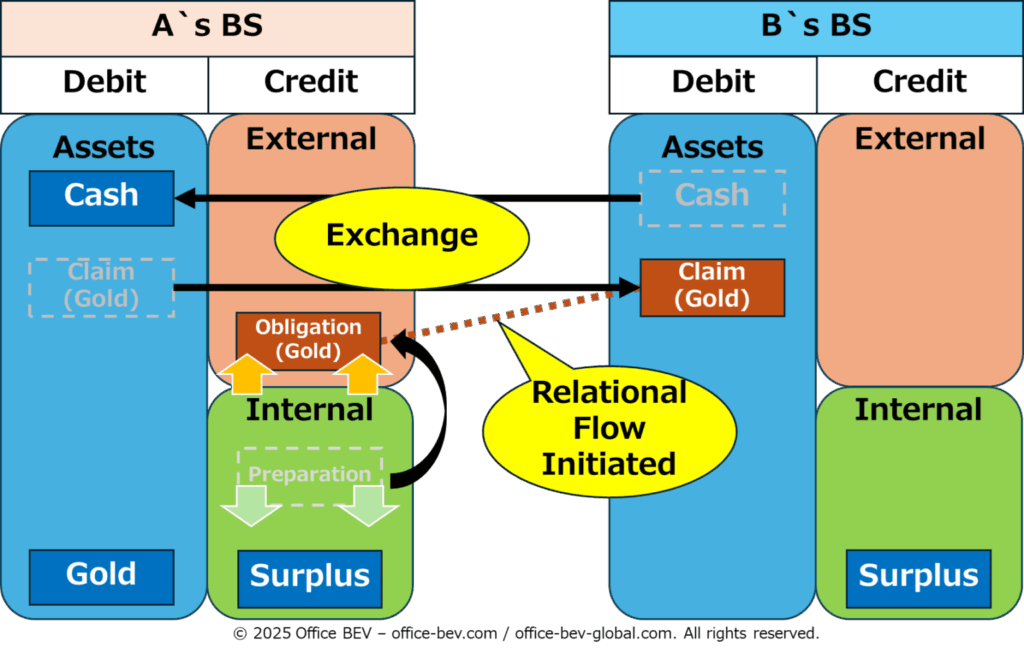

Step-3: Exchange execution

A’s claim (gold) is exchanged for B’s cash.

A’s preparation shifts from internal to external, transforming into an obligation to deliver the gold.

This marks the initiation of a relational flow between A and B.

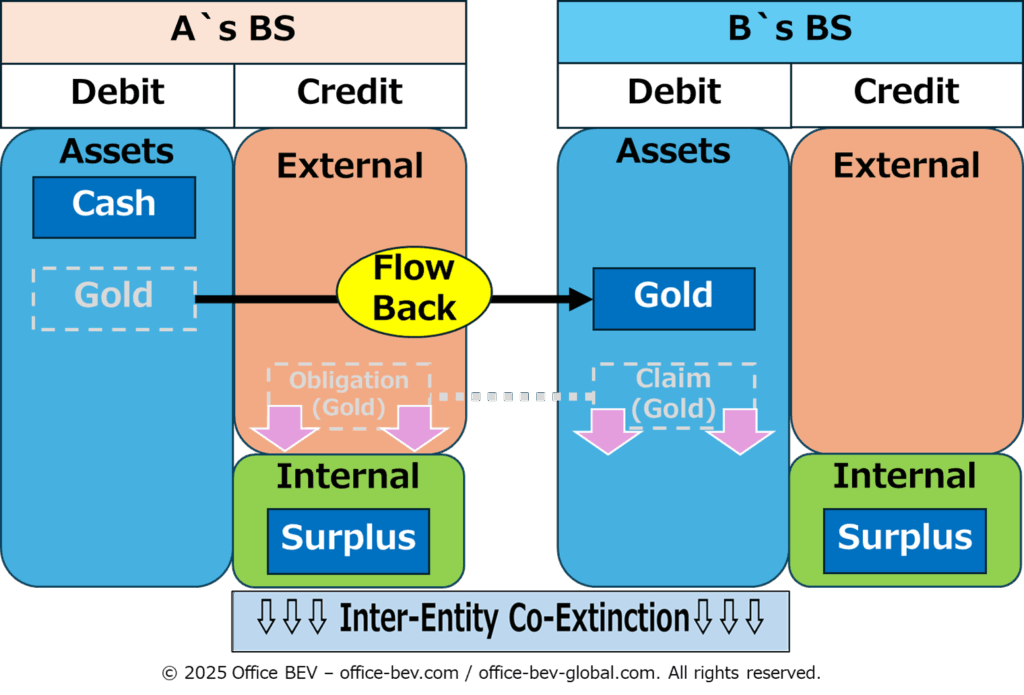

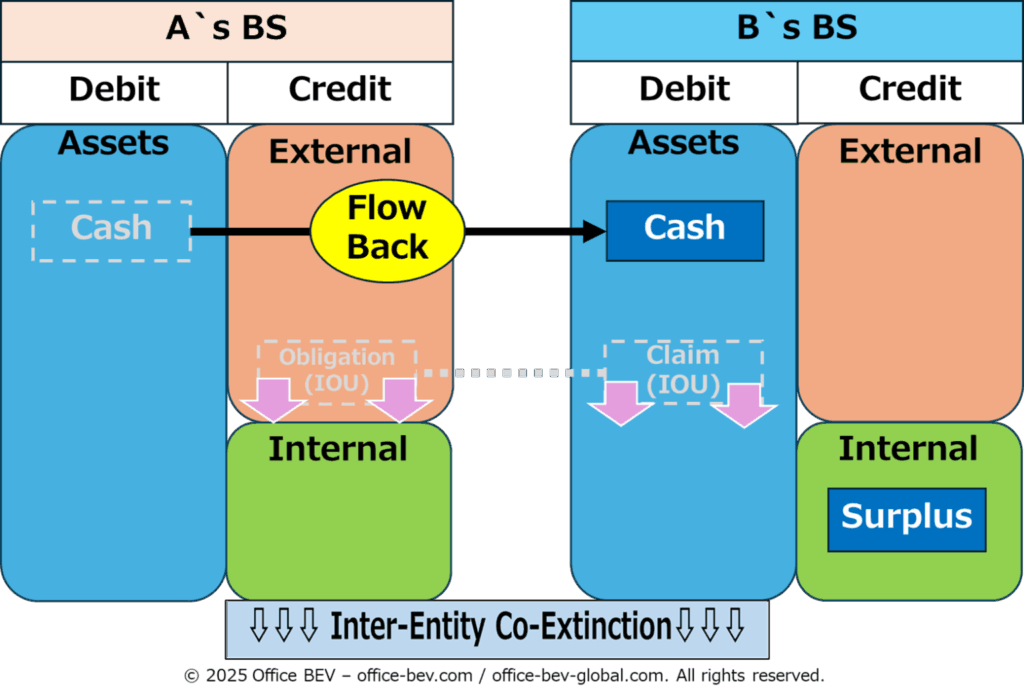

Step-4: Claim Exercise and Obligation Settlement

B exercises the claim, prompting A to deliver the underlying gold.

The asset (gold) flows back from A to B, and both the claim and obligation are extinguished through Inter-Entity Co-Extinction.

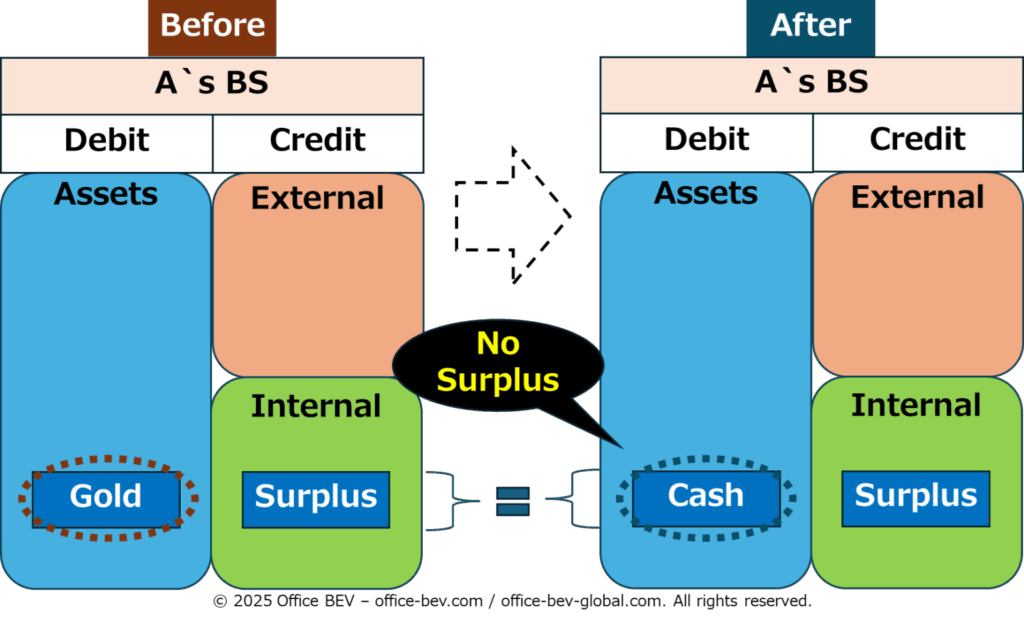

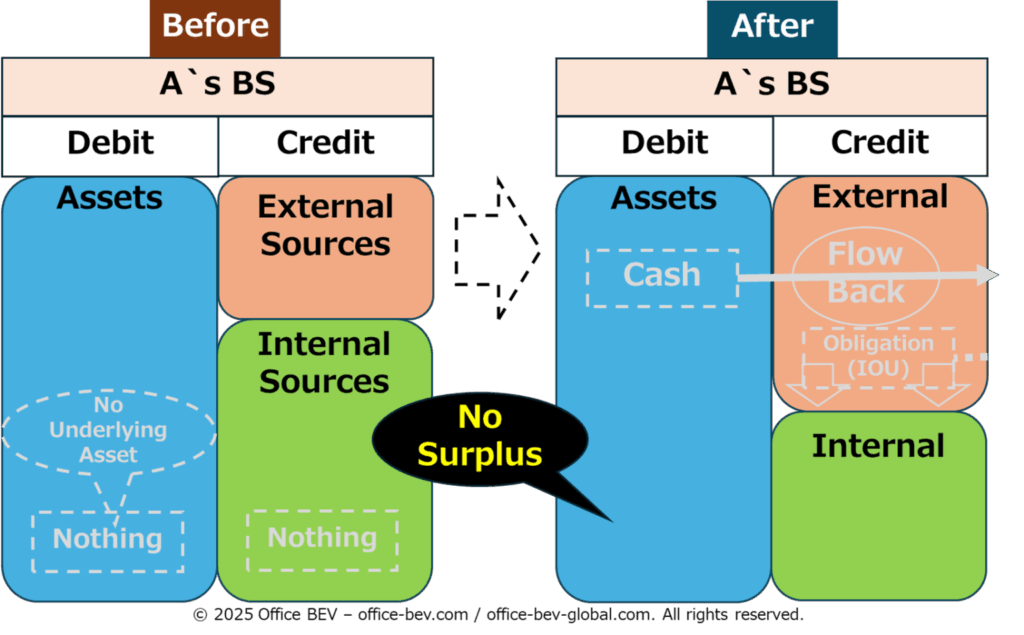

◆ Before/After Comparison — No Surplus Generated

A generated a securitized claim through Single-Entity Co-Generation, using gold as the underlying asset.

But in the end, the gold was simply exchanged for an equal amount of cash.

The total value on A’s balance sheet remains unchanged—no surplus is generated.

(Whether any surplus arises for the two parties involved in the exchange—A and B collectively—will be examined later in the section on inter-entity stock transfers, using a consolidated BS view for comparison.)

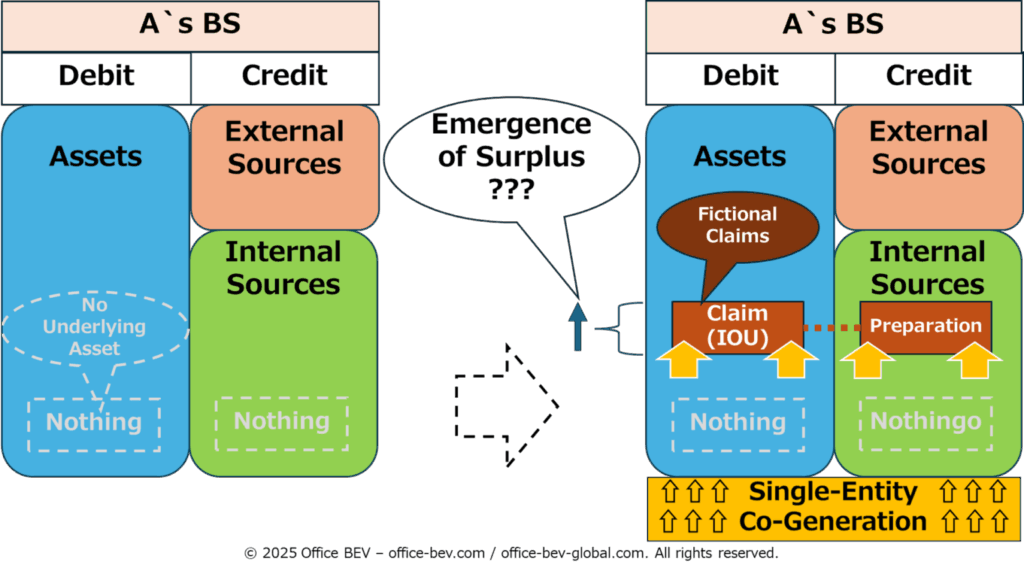

(2) Fictionally Created Claims

These are claims created without any underlying asset—based not on an existing resource but on expectation or credibility.

Although structurally similar to securitized claims, their value is entirely fictional at the time of creation.

Example: Creating a self-issued IOU — a promise to repay in the future, with no asset in hand

Let’s say A issues a claim promising to deliver money in the future—despite not holding any cash now.

The claim is recorded as an asset on A’s balance sheet, even though it has no tangible backing.

Let’s walk through the steps of this fictional claim creation, using A’s balance sheet as our frame.

Step-1: Single-Entity Co-Generation on A’s BS

Single-Entity Co-Generation allows A to create a receivable and its corresponding credit entry, even without an underlying asset.

Debit: Claim to receive cash (IOU)

Credit/Internal Sources: Preparation (indicating readiness to enter external flow — based solely on trust)

This structure reflects internal readiness but no actual obligation yet. The value here is fictional: it exists only through belief in future repayment.

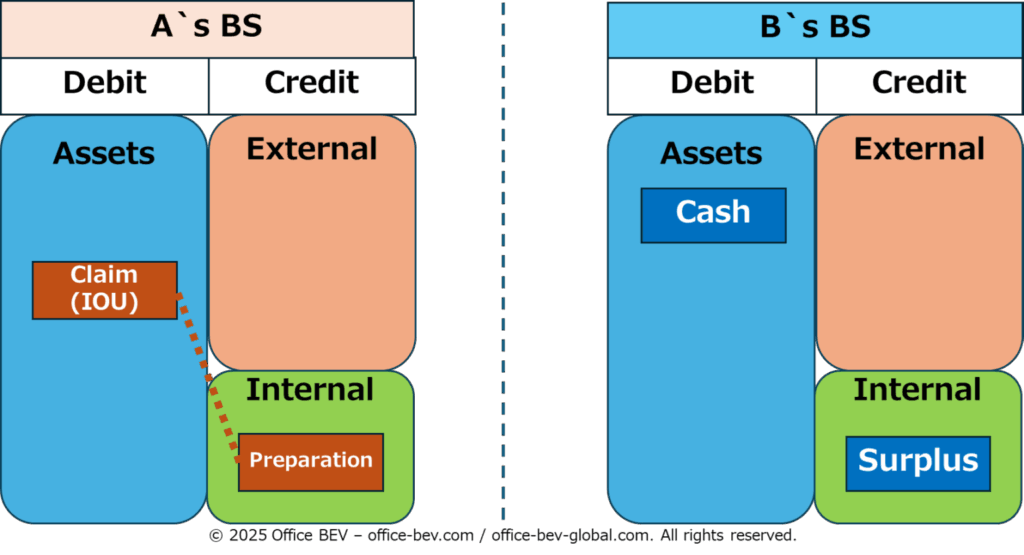

Step-2: Preparing for the exchange

A seeks to raise cash from B by offering the IOU.

B evaluates A’s credibility and considers whether to accept the claim.

Step-3: Exchange execution

A receives cash from B in exchange for the unbacked claim.

The internal “Preparation” entry shifts to an external obligation—A now owes B.

The flow relationship begins.

Step-4: Claim Exercise and Obligation Settlement

B exercises the claim. A returns the borrowed cash.

The claim and obligation are extinguished through Inter-Entity Co-Extinction.

◆ Before/After Comparison — No Surplus Generated

Although the claim initially appeared as new value on A’s BS, it was ultimately repaid.

The balance sheet returns to its original state—no surplus remains.

(Whether any surplus arises through this lending flow—including interest—will be examined later in the section on lending flow.)

2.2 Inter-Entity Stock Transfers — Can Surplus Arise Through Asset Movement?

Inter-Entity Stock Transfers refer to changes in stock assets that occur across separate entities, involving the transfer of assets from one balance sheet to another. In this section, we examine whether such transfers generate surplus.

There are two basic types of inter-entity stock transfers: (1) Unilateral Transfers, and (2) Bilateral Transfers.

(1) Unilateral Transfer — One-Way Movement Without Return

This refers to a one-way movement of an asset from one entity to another, with no reciprocal exchange. The asset leaves the originator’s balance sheet and appears on the recipient’s—without any claim or obligation involved.

Unilateral transfers can occur either involuntarily or voluntarily, but structurally, both represent the same phenomenon: a stock asset moves between entities without triggering any relational flow.

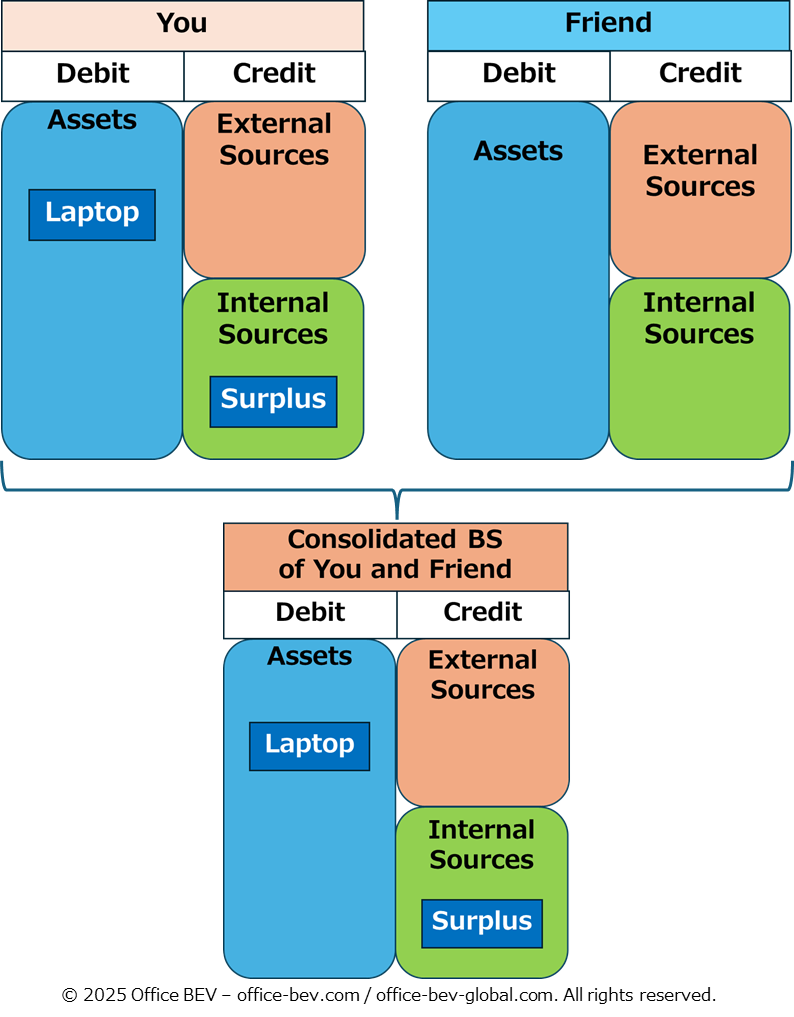

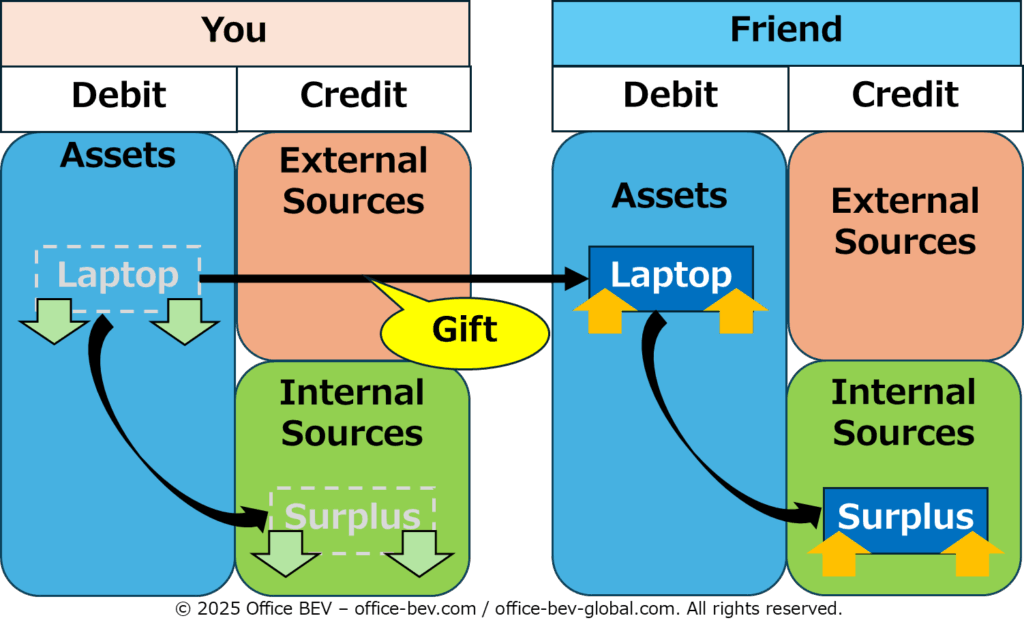

Example: You give your friend a laptop.

Step-1: Before the transfer

You hold a laptop on your balance sheet.

Step-2: Transfer execution

The laptop is handed over to your friend.

Step-3: After the transfer

You no longer hold the laptop. Your friend now holds it.

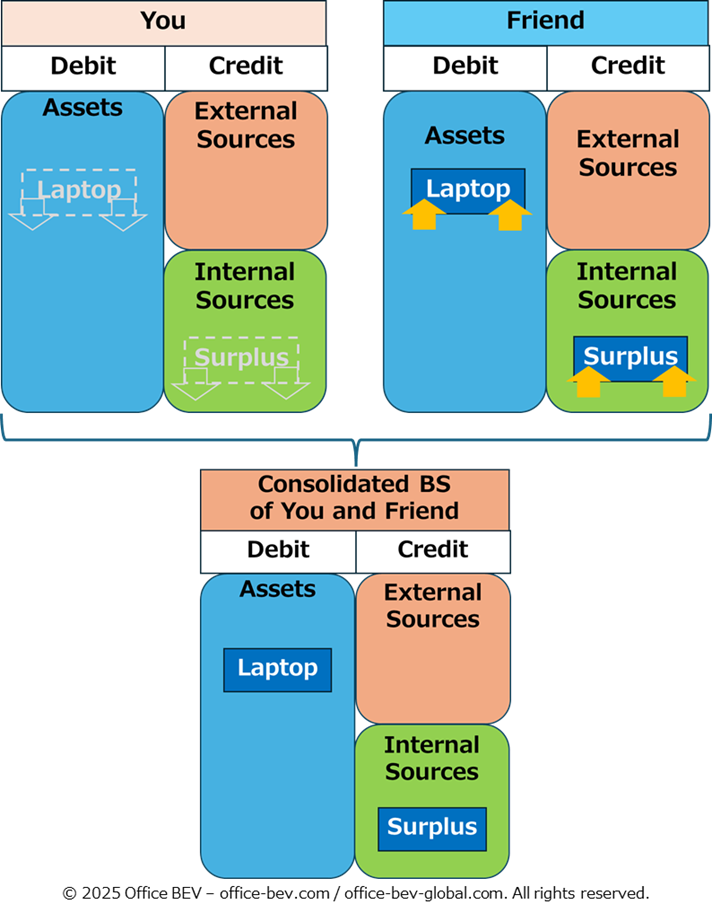

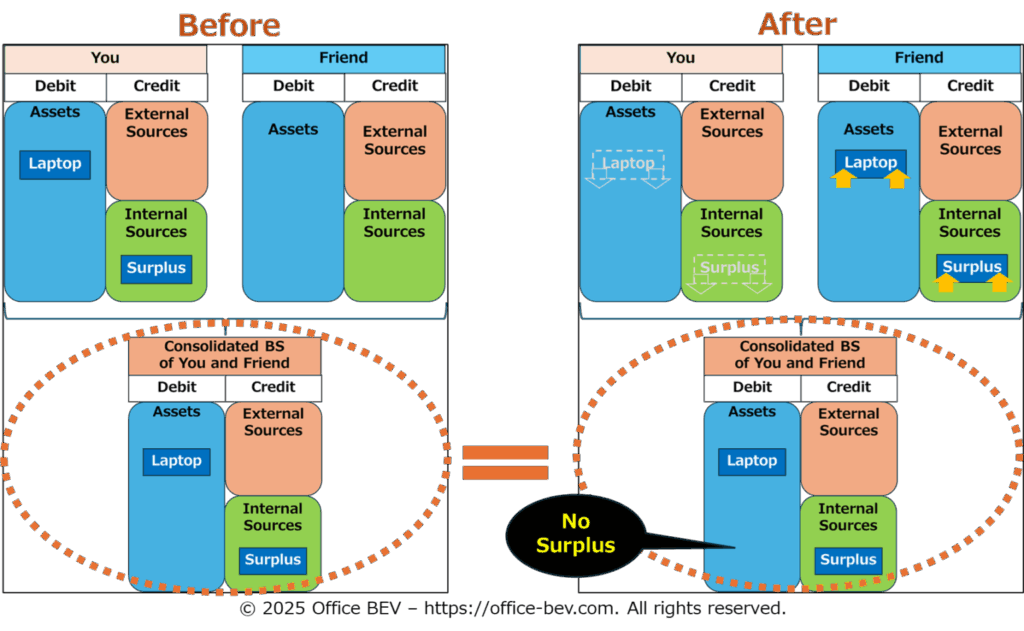

◆ Before/After Comparison — No Surplus Generated

Although the recipient’s balance sheet shows an increase in assets, this reflects only the arrival of an existing asset. From a consolidated view that includes both parties, the total asset value remains unchanged—no surplus has been created.

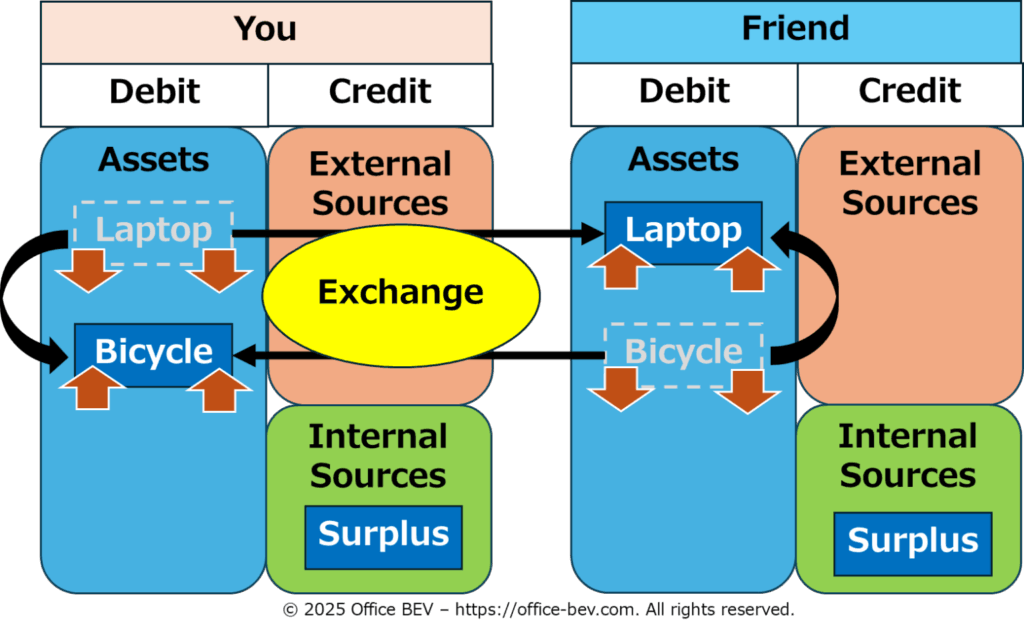

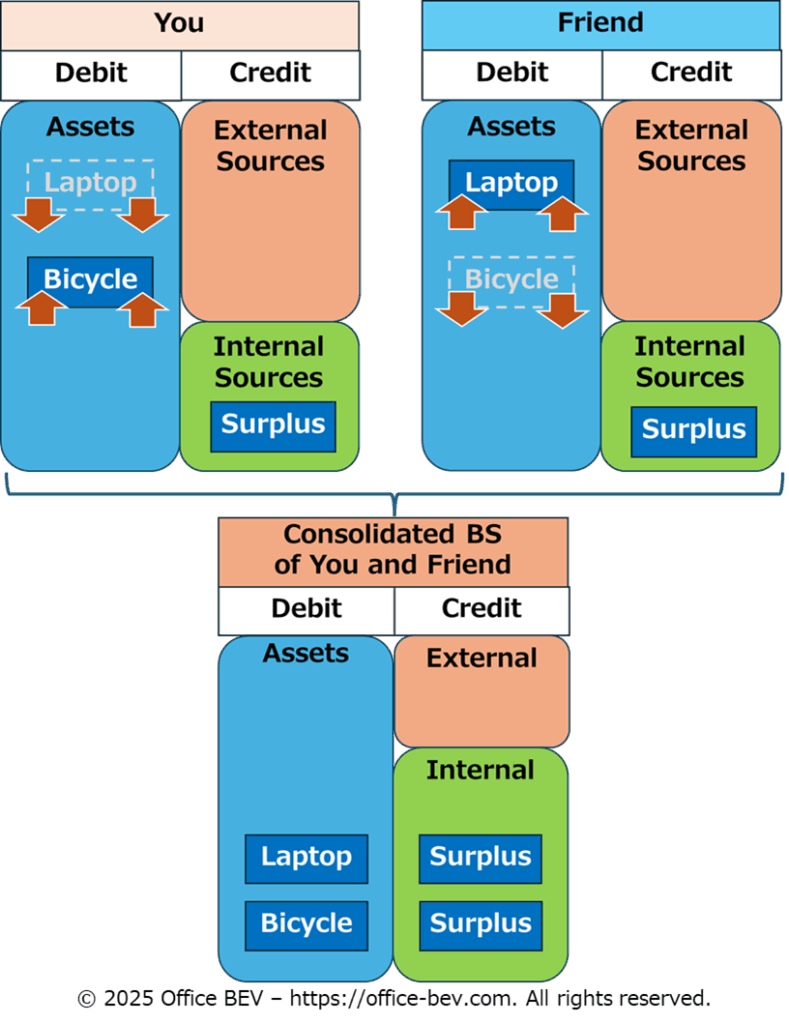

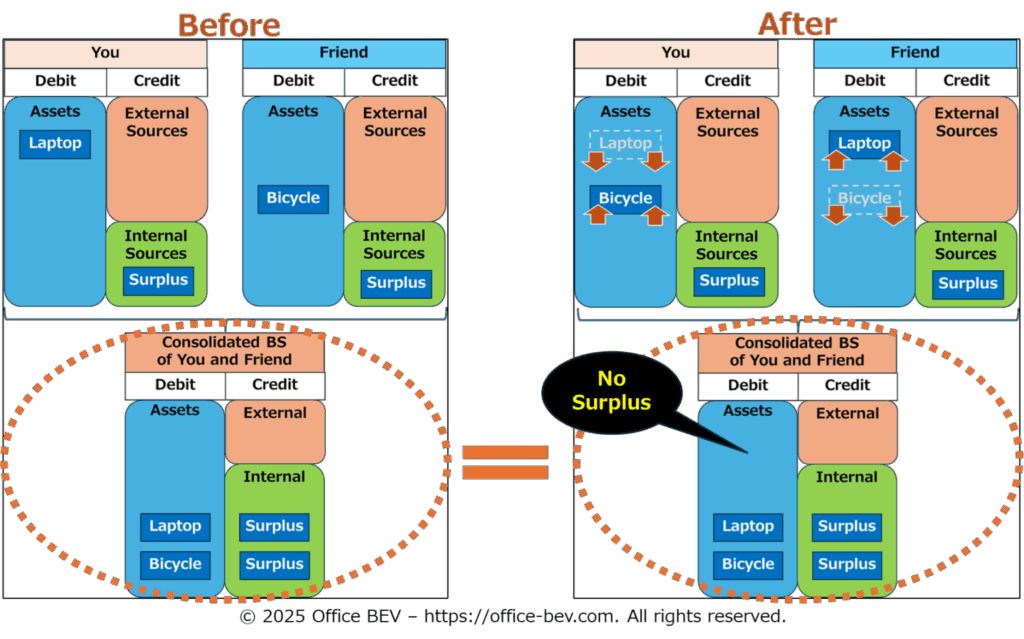

(2) Bilateral Stock Transfer — Two-Way Movement Through Exchange

This refers to a two-way movement of stock assets between entities, where each entity gives and receives an asset of value.

Unlike unilateral transfers, which involve movement in only one direction, bilateral transfers feature reciprocal exchange — but still without generating any claim or obligation.

Example: You exchange your laptop for your friend’s bicycle.

Step-1: Before the exchange

Each party holds their respective asset on their balance sheet.

You hold a laptop; your friend holds a bicycle.

Step-2: Exchange execution

The assets are simultaneously exchanged.

Your laptop is transferred to your friend, and their bicycle is transferred to you.

Step-3: After the exchange

You now hold the bicycle; your friend now holds the laptop.

Each balance sheet has changed in composition, but not in total value.

◆ Before/After Comparison — No Surplus Generated

Although both entities now hold different assets, the exchange involves a one-to-one substitution of existing value.

From a consolidated perspective that includes both entities, the total asset value remains unchanged—no surplus has been created.

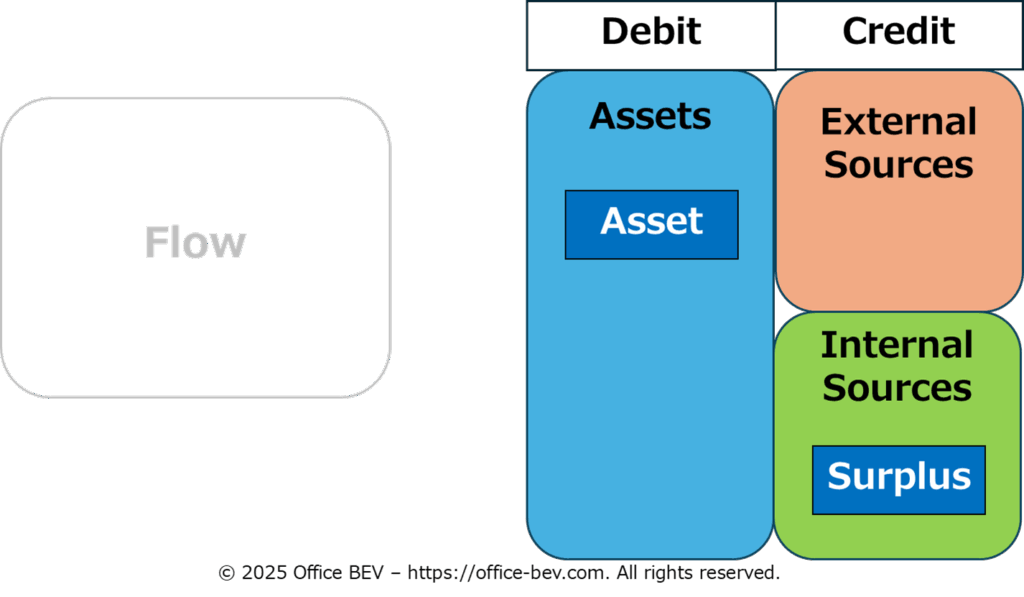

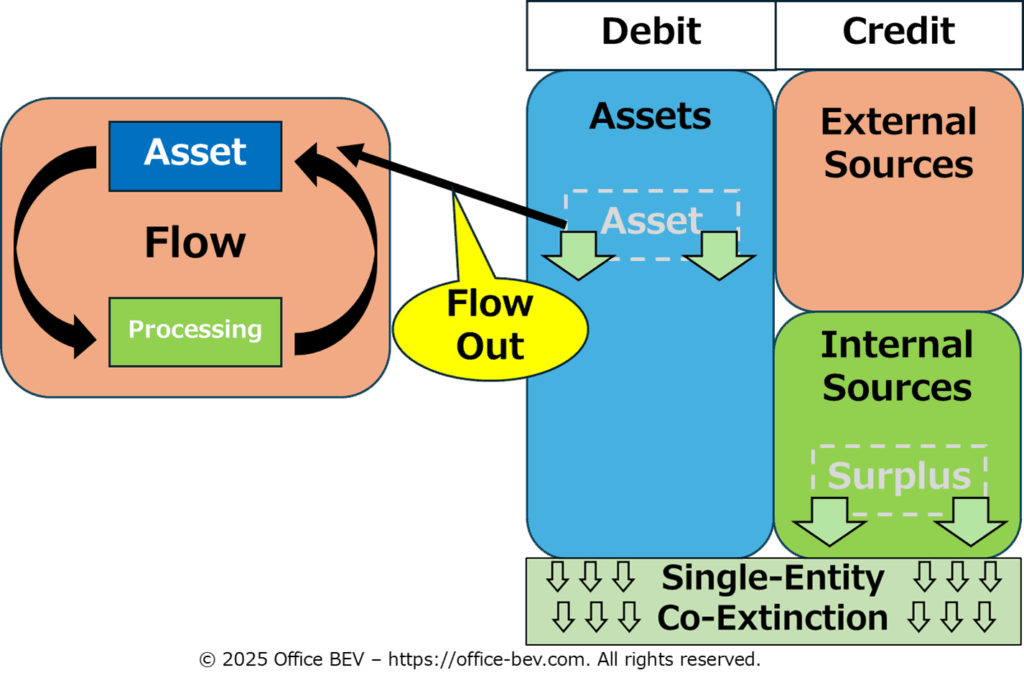

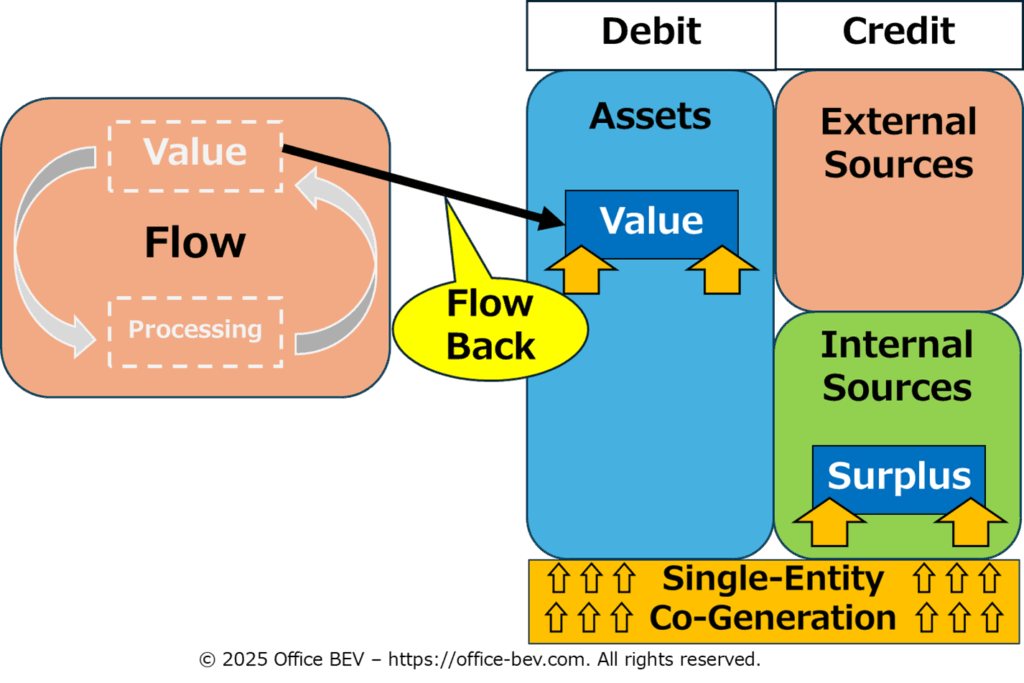

2.3 Self-Contained Flow Cycles — Can Internal Deployment Generate Surplus?

A self-contained flow cycle refers to the internal deployment of an asset by the same entity, followed by the retrieval of a different form of value after a certain period of time. It is a flow-based process that begins and ends within a single balance sheet.

There are two main types of self-contained flow cycles: Consumption Flows and Operational Flows. In both cases, an asset is deployed internally, transformed over time, and then recovered in a different form.

Step-1: Before Deployment

An asset is held before being deployed into the flow process.

Step-2: Deployment (Flow Out)

The asset is internally deployed—flowed out—into a specific process, such as consumption flows or operational flows.

Step-3: Recovery (Flow Back)

After a certain period of time, the asset is recovered—flows back—in the form of a transformed or augmented value.

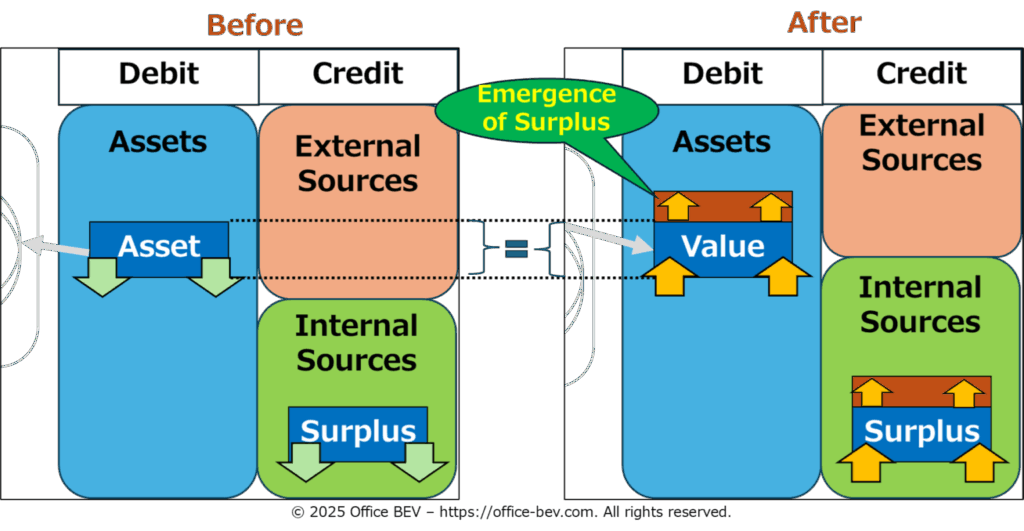

◆ Before/After Comparison — Surplus Arises If Recovery Exceeds Deployment

In a self-contained flow cycle, if the recovered value exceeds the original input, surplus is generated.

◆ Surplus Types in Self-Contained Flow Cycles

In Self-Contained Flow Cycles, Surplus can arise in various forms depending on what is recovered after the internal deployment.

(1) Physical Surplus

Generated through Consumption Flows that enhance bodily strength, endurance, or recovery.

→ Example: Gaining physical energy after rest or nutrition intake.

→ Non-monetary surplus

(2) Mental Surplus

Generated through Consumption Flows that improve cognitive capacity, creativity, or emotional clarity.

→ Example: Gaining mental focus after meditation or study.

→ Non-monetary surplus

(3) Monetary Surplus

Generated through Operational Flows that yield direct monetary returns such as cash or deposits.

→ Example: Providing a freelance service (such as design, writing, or tutoring) and

receiving payment afterward.

→ Monetary surplus

(4) Asset-Based Surplus

Generated through Operational Flows that result in Pure Stock Assets (PSAs)—goods, tools, or intellectual property—that can be used or monetized in the future.

→ Example: Creating a product, or developing a new technology.

→ Non-monetary surplus (potentially monetizable)

2.4 Inter-Entity Flow Cycles — Can Surplus Arise Through Relational Flows?

An Inter-Entity Flow Cycle refers to a process in which an asset held by one entity is deployed toward another entity, thereby establishing a relational structure of claim and obligation (Inter-Entity Co-Generation). After a certain period of time, the original asset is recovered and the relational structure is extinguished (Inter-Entity Co-Extinction).

There are two primary types of Inter-Entity Flow Cycles:

- Lending Flows

- Investment Flows

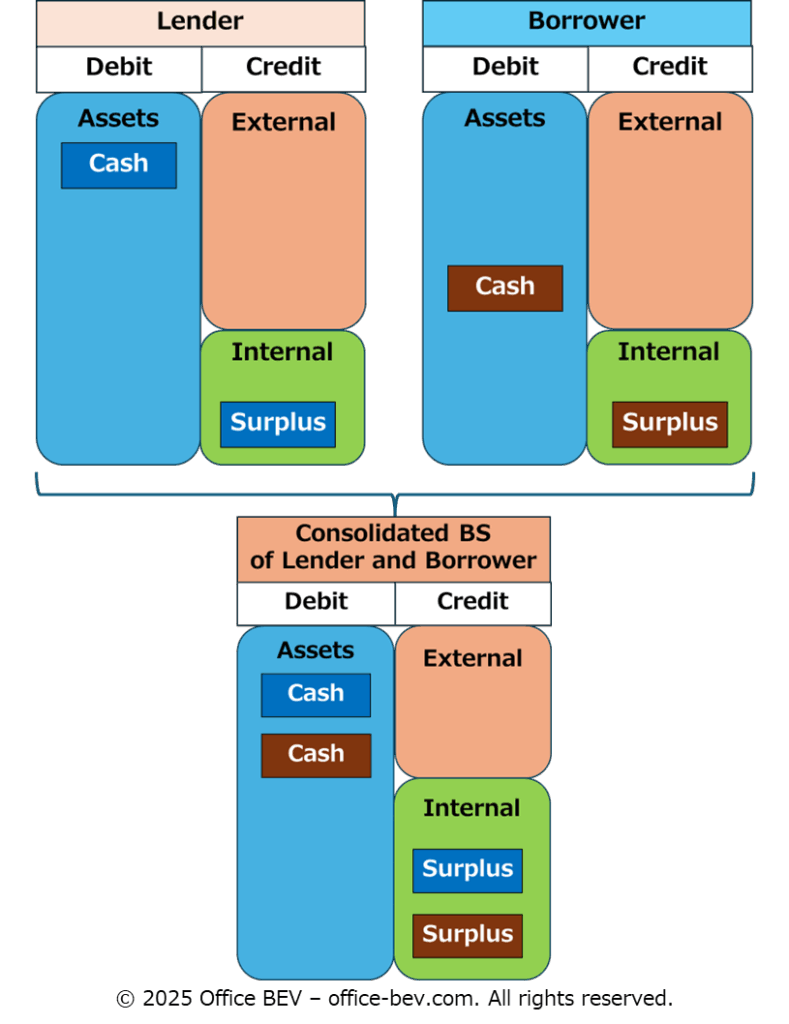

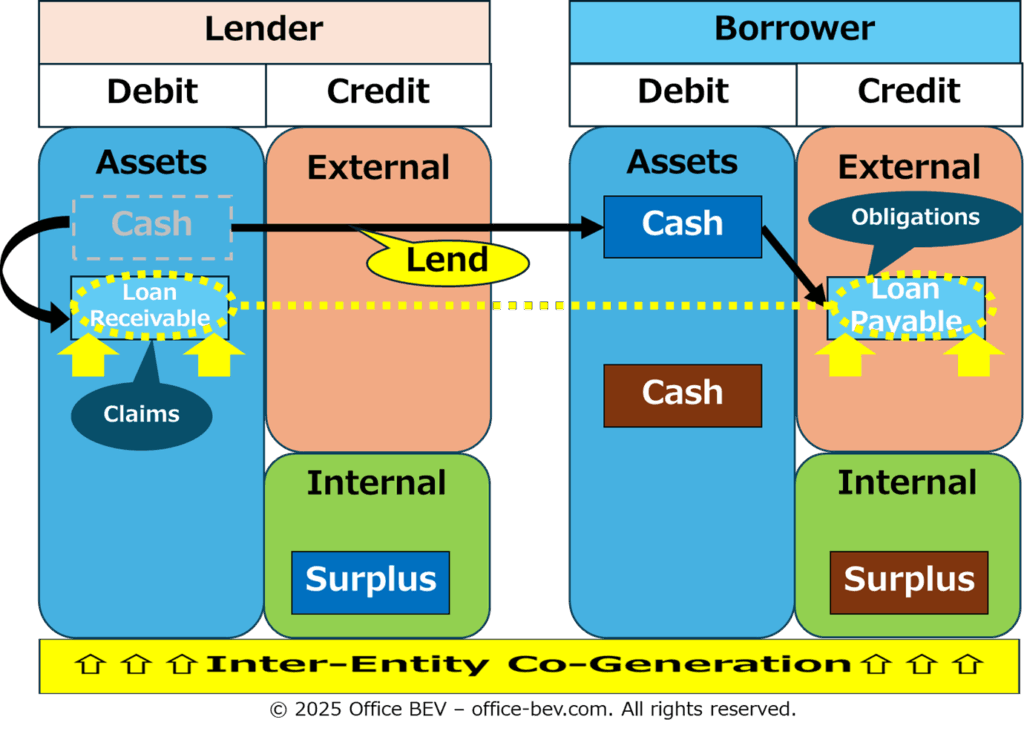

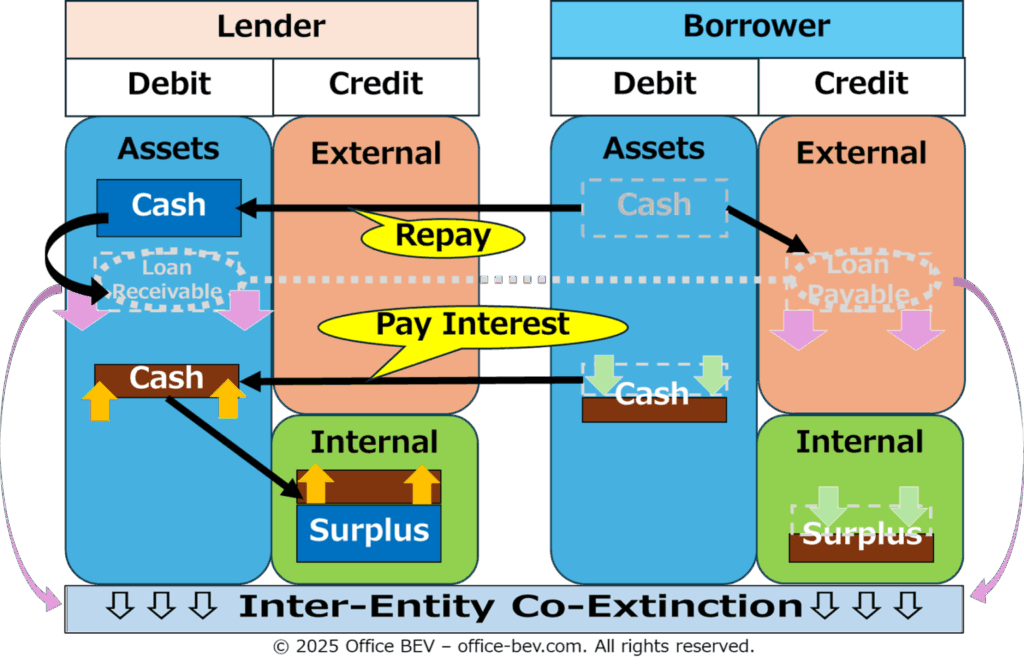

(1) Lending Flow — Principal and Interest

Example: The lender provides cash to the borrower and, after a fixed period, recovers the principal along with interest.

Step-1: Before Lending

The lender holds cash on their balance sheet.

Step-2: Lending Execution

Cash is transferred to the borrower; a claim and a corresponding obligation are simultaneously generated through Inter-Entity Co-Generation, marking the beginning of a reciprocal relationship between the two entities.

Step-3: Repayment Execution (Principal and Interest)

The borrower returns the principal and pays interest; the reciprocal claim–obligation relationship is extinguished through Inter-Entity Co-Extinction.

Step-4: After Repayment

The lender holds more cash; the borrower holds less.

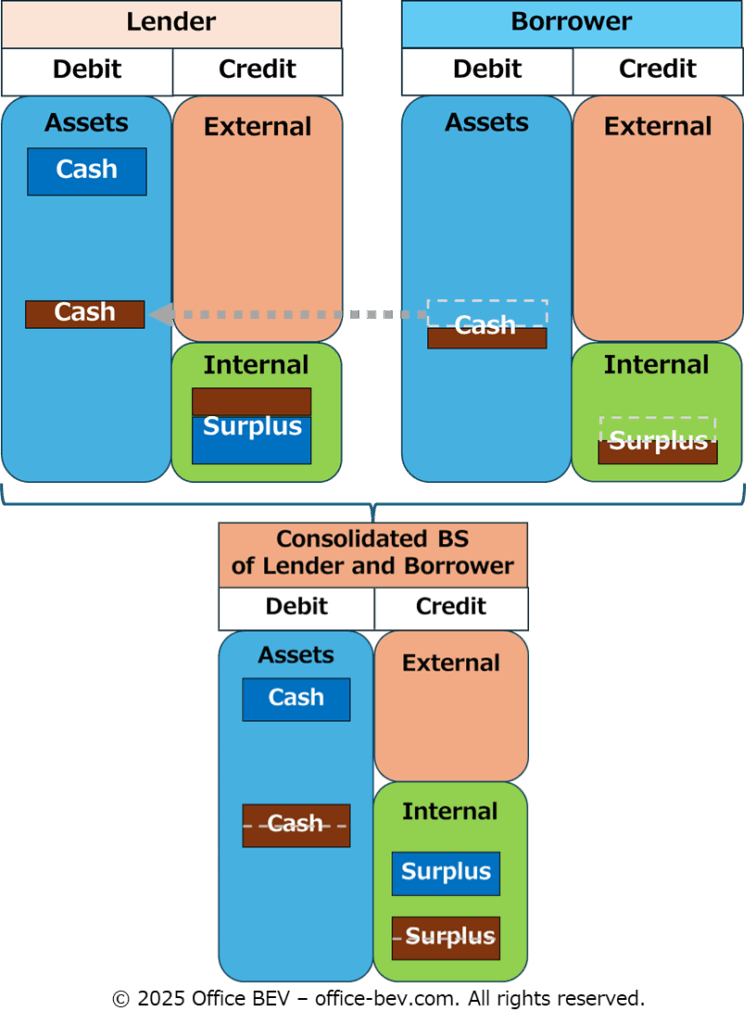

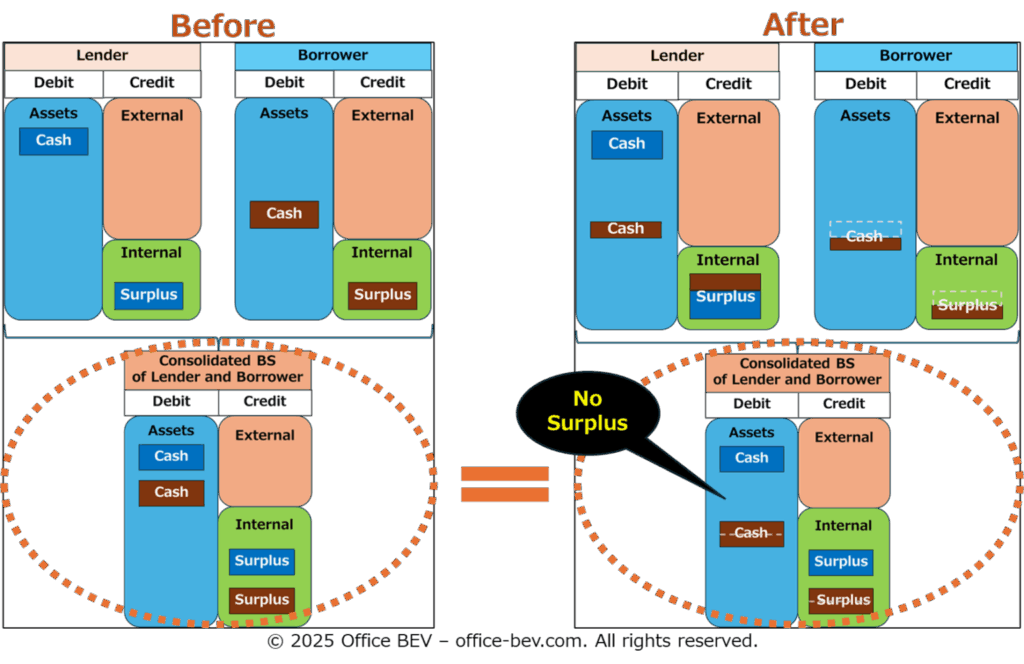

◆ Before/After Comparison — No Surplus Generated

In a lending flow, the principal moves from the lender to the borrower at the start, and back to the lender upon repayment.

The interest is merely a portion of the borrower’s existing assets transferred to the lender.

From a consolidated balance sheet perspective that includes both entities, the total amount of assets remains unchanged—no surplus is generated.

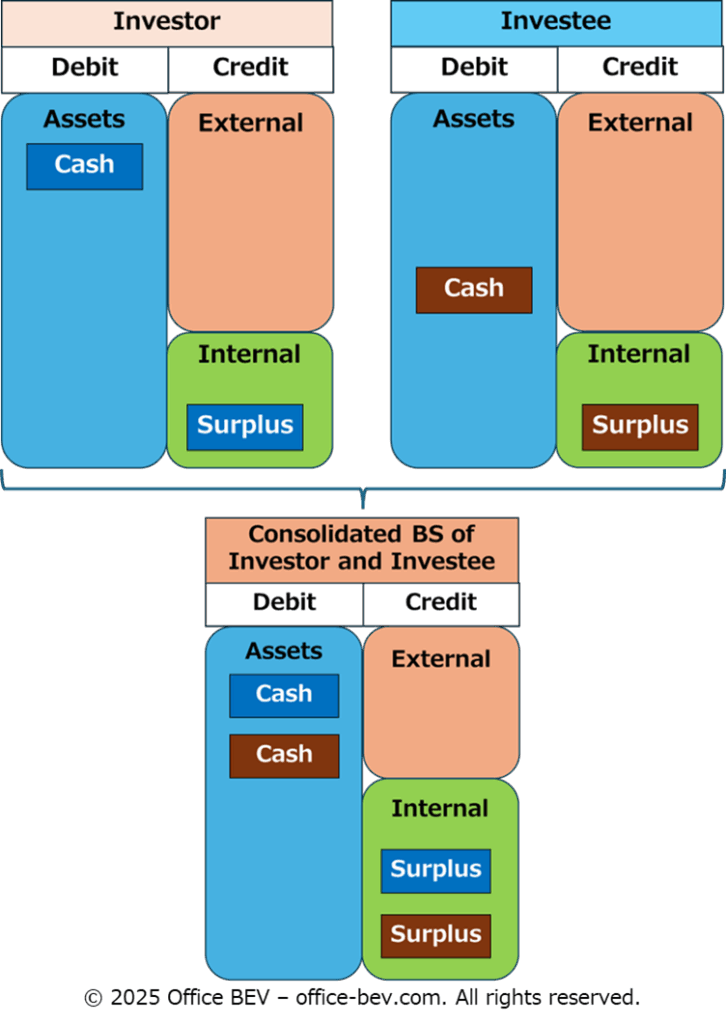

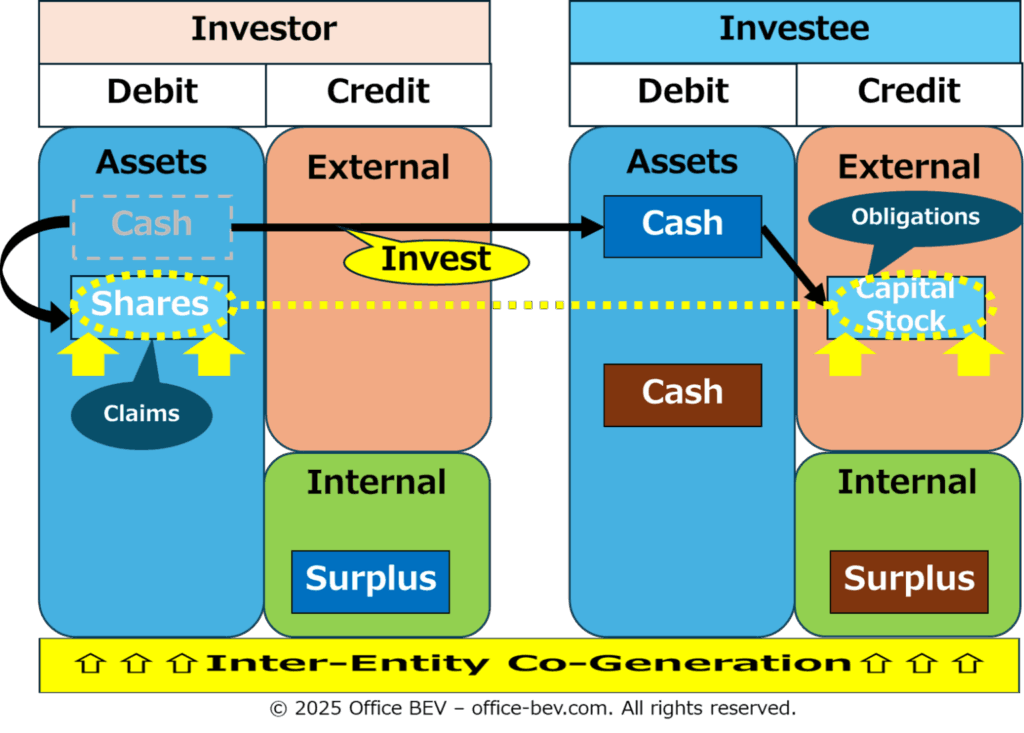

(2) Investment Flow — Capital and Returns

Example: An investor invests cash into an investee’s business and, after a certain period, receive a return (dividends).

Step-1: Before Investment

The investor holds cash as an asset.

Step-2: Investment Execution

Cash is transferred to the investee’s balance sheet; simultaneously, shares and a corresponding capital entry are generated through Inter-Entity Co-Generation, marking the beginning of a reciprocal relationship between the two entities.

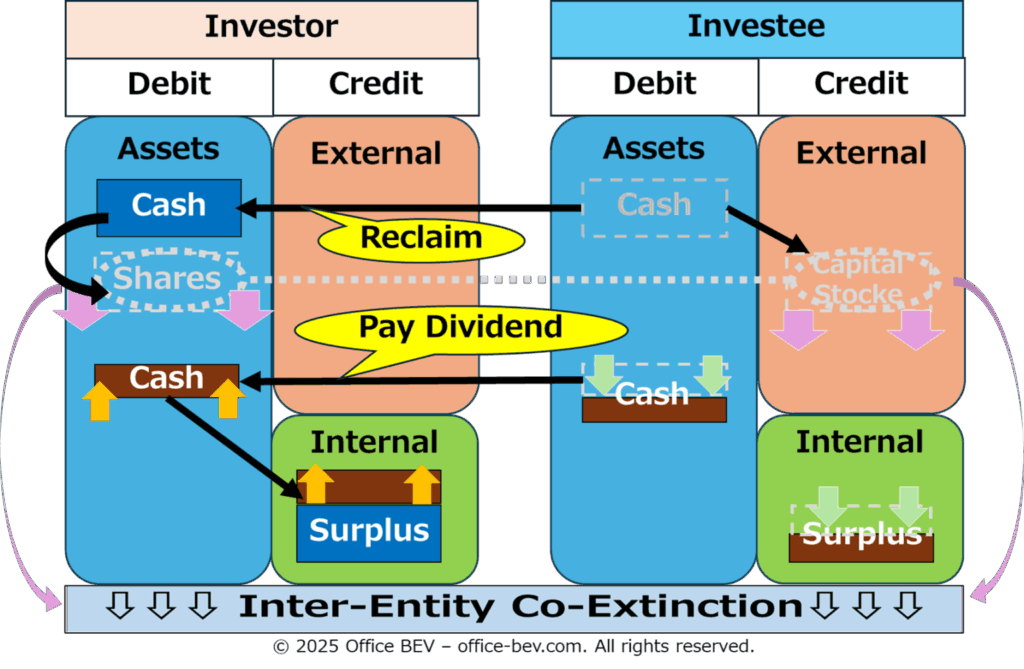

Step-3: Recovery Execution (Return of Capital and Distribution of Returns)

The investee returns the invested capital and distributes the agreed-upon returns; the reciprocal claim–obligation relationship is extinguished through Inter-Entity Co-Extinction.

Step-4: After Recovery

The investor now holds more cash; the investee’s assets have decreased.

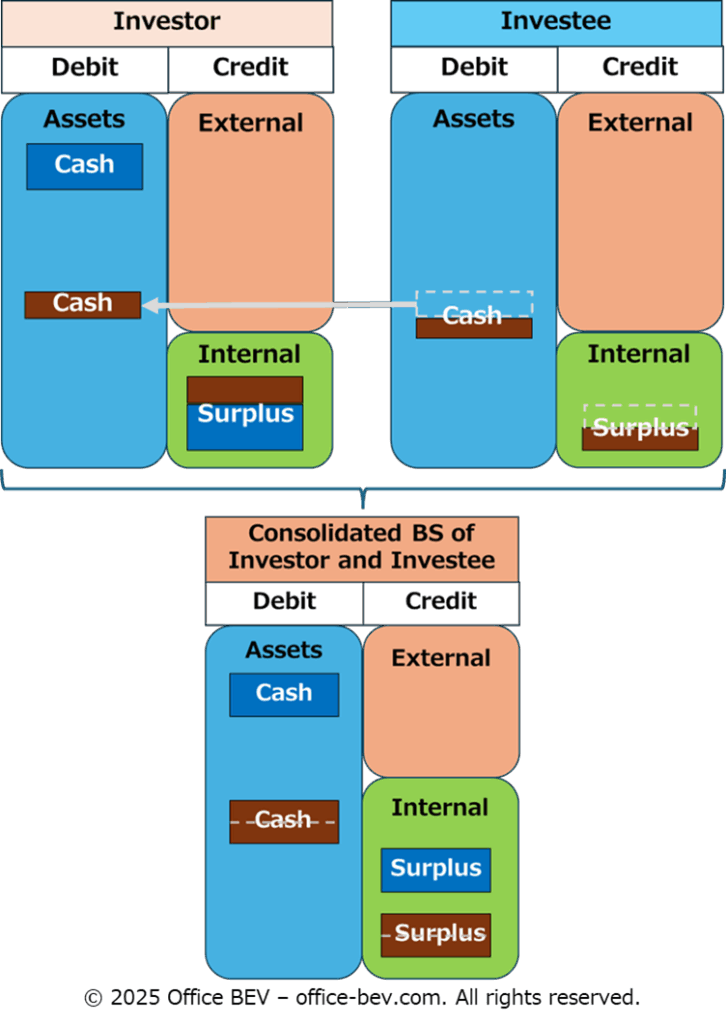

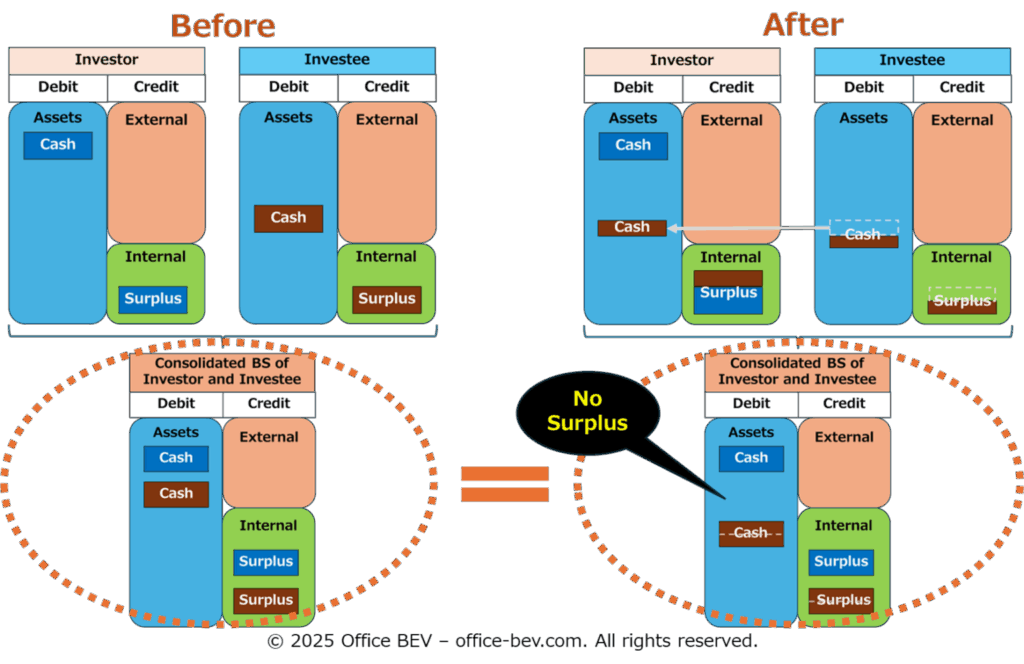

◆ Before/After Comparison — No Surplus Generated

In an investment flow, the capital is transferred from the investor to the investee.

The return (like dividends) is simply a portion of the investee’s existing assets transferred to the investor.

From the perspective of a consolidated balance sheet that includes both entities, the total asset value remains unchanged—no surplus is generated.

Observation: Do Interest and Dividends Represent Surplus?

At first glance, interest (in lending flows) and dividends (in investment flows) may appear as surplus gains to the lender or investor.

However, their sources may lie in the existing assets of the borrower or investee, or in surplus generated through asset changes or movements involving third parties—outside the inter-entity flow cycle being examined.

Ultimately, the inter-entity flow cycle does not, by itself, generate surplus.

This understanding leads us toward a deeper exploration of the fundamental elements of surplus.

3.Only One Path Leads to Surplus

In the previous chapter, we examined all eight types of asset movement to determine whether they generate surplus. Based on those findings, this chapter aims to consolidate the results, classify the types of surplus that emerge, and identify the asset movement structures where surplus generation occurs.

3.1 Asset Movement Types That Generate Surplus

Let’s begin by summarizing which movement types actually generate surplus:

(1) Self-Contained Stock Change

When pure stock assets (e.g., apples growing spontaneously) are acquired without any prior asset input—such as labor or exchange—A surplus is generated.

- Type of Surplus: Pure Stock Asset / Non-monetary

- Input Asset: None

(2) Inter-Entity Stock Transfer

These movements involve only the relocation of existing assets. No surplus is generated.

(3) Self-Contained Flow Cycles

These are internal cycles in which an asset is deployed and later recovered in a transformed value. When the recovered value exceeds the deployed input, surplus is generated. This includes two subtypes:

1) Consumption Flow

Surplus arises when the recovery enhances physical or mental capacity beyond the original input. From a BS perspective, both can be abstracted as labor power.

▪ Type of Surplus: Labor Power (Physical or Mental) / Non-monetary

▪ Input Asset: Pure Stock Asset (e.g., food, content)

2) Operational Flow

Surplus arises when the output exceeds the total value of the deployed inputs.

▪ Type of Surplus:

1) Pure Stock Asset (e.g., products, knowledge) / Non-monetary

2) Money

▪ Input Assets: Pure Stock Asset (e.g., materials), Labor Power, Money

(4) Inter-Entity Flow Cycle

Both the principal in lending/investment flows and the returns (interest/dividends) are transfers of existing assets.

Thus, no surplus is generated within the flow itself.

Conclusion:

Among the eight movement types, only Self-Contained Stock Change and Self-Contained Flow Cycles generate surplus.

However, the former can be regarded as a special case of the latter—a cycle with zero input, where the asset is recovered at the moment it emerges.

In this sense, all surplus ultimately originates from Self-Contained Flow Cycles.

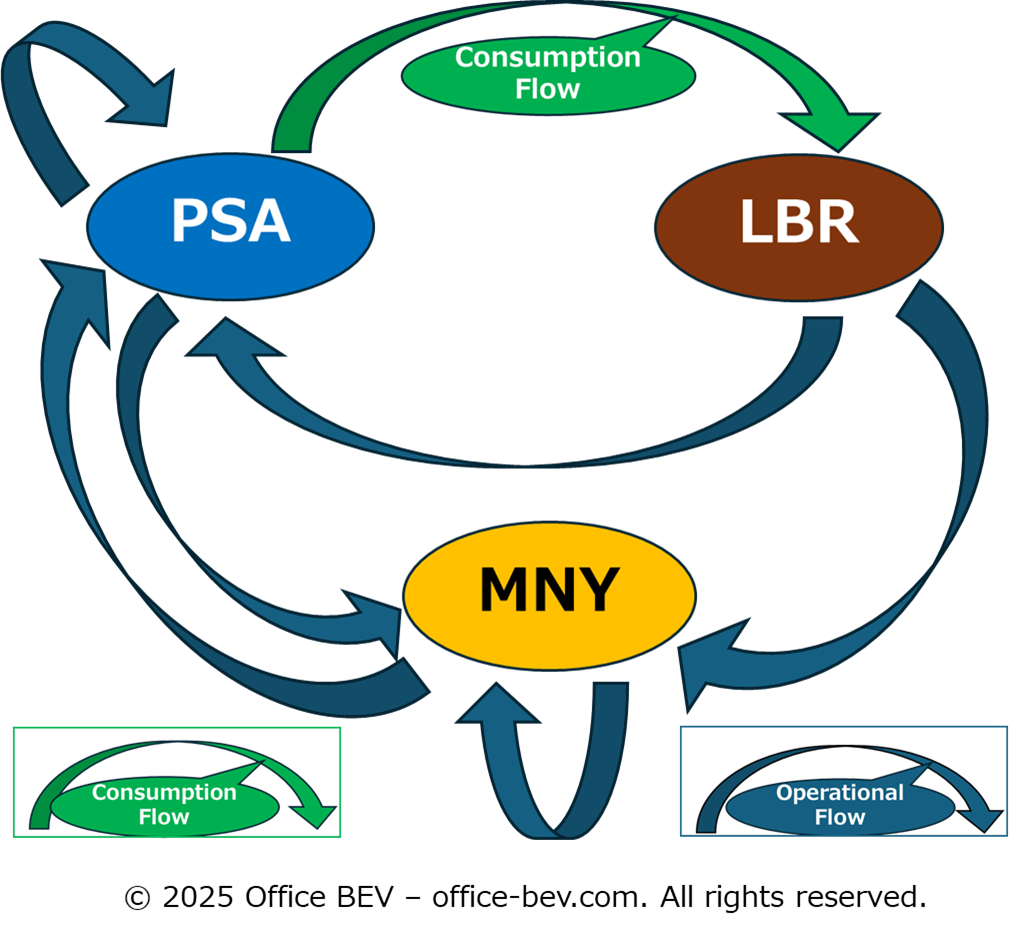

3.2 Core Components and Cycles of Surplus

As established earlier, Surplus arises from Self-Contained Flow Cycles. When we examine the input assets involved and the resulting surplus, we find that all cases converge into three core components:

Pure Stock Asset (PSA), Labor Power (LBR), and Money (MNY).

| Type of Surplus | Flow Type | Input Assets |

|---|---|---|

| (1) Labor Power (non-monetary) | Consumption Flow | PSA |

| (2) PSA (non-monetary) | Operational Flow | LBR / PSA / MNY |

| (3) Money | Operational Flow | LBR / PSA / MNY |

The diagram below illustrates how these three components move through two interdependent flows—consumption and operational—in the generation of surplus.

By examining how these three components interact, the following structure emerges:

Consumption Flows convert Pure Stock Assets (PSA) into Labor Power (LBR), but cannot generate PSA themselves. They thus rely on PSA supplied by Operational Flows. Conversely, Operational Flows use and regenerate both PSA and Money (MNY), but require LBR to function—a component that only Consumption Flows can produce.

In short, LBR flows one-way from Consumption to Operational Flows as an external input, while PSA and MNY circulate internally within Operational Flows. Surplus arises not within either flow alone, but through their interdependence.

4. Conclusion — Surplus Emerges Only in Self-Contained Flow Cycles

This article addressed the central question: Where does surplus come from?

By examining all eight types of asset movement introduced earlier, we find that only Self-Contained Flow Cycles—namely, Consumption Flows and Operational Flows—have the structural potential to generate surplus.

Within these cycles, Three Core Components—Pure Stock Assets (PSA), Labor Power (LBR), and Money (MNY)—circulate through two interdependent flows. In Consumption Flows, PSA is used to generate LBR. In Operational Flows, LBR and other assets are deployed to generate PSA and MNY. These two flows sustain each other: Consumption Flows depend on PSA regenerated through Operational Flows, while Operational Flows are activated by LBR generated through Consumption Flows. Surplus arises when the value recovered within this regenerative cycle exceeds the original input.

This is the structural answer to surplus: it emerges only when value flows internally and regeneratively within Self-Contained Flow Cycles—through the dual system of Consumption Flows and Operational Flows.

4 thoughts on “Structural Analysis(3): The Emergence of Surplus — Part 1: The Generation of Surplus”

Comments are closed.