Structure of This Article

This article proceeds as follows:

1. Introduction: Where Do Assets Come From?

2. The Birth of Assets: Single-Entity Co-Generation

3. The Creation of Stock Assets

(1) Pure Stock Assets (Accumulated Assets)

(2) Stock-like Flow Assets (Structurally Created Assets)

(2-1) Securitized Claims

(2-2) Fictionally Created Claims

4. The Creation of Flow Assets

(1) Flow from Pure Stock Assets (Inter-Entity Co-Generation)

(2) Exchange of Stock-like Flow Assets (No Inter-Entity Co-Generation)

(3) Flow from Stock-like Flow Assets (Layered Flow Structures)

5. Conclusion: Genesis as the Structural Foundation of Assets

1. Introduction: Where Do Assets Come From?

Where do assets come from?

This fundamental question lies at the very origin of balance sheet (BS) analysis. In order for an asset to “move” on a BS, it must first exist. But how does it come into being?

This article begins by exploring the genesis of assets — how they are created from nothing. Using the full framework of the Three-Layer BS Model — Layer 1: Domain of the Balance Sheet (whose BS is being analyzed), Layer 2: Structure = Stock/Flow, and Layer 3: Relations = Relativity — we examine the basic mechanics of asset creation.

We focus especially on two structural processes:

- Single-Entity Co-Generation: The creation of assets within a single BS (structure)

- Inter-Entity Co-Generation: The creation of assets through relational interaction (relations)

Through these two perspectives, we see how all three analytical layers — domain, structure, and relations — are involved in the genesis of assets.

Chapter 2 defines the basic form of single-entity asset creation. Chapters 3 and 4 then explore how the assets created through this process either remain internal as stock assets or, through inter-entity co-generation, gain value by entering external relationships as flow assets.

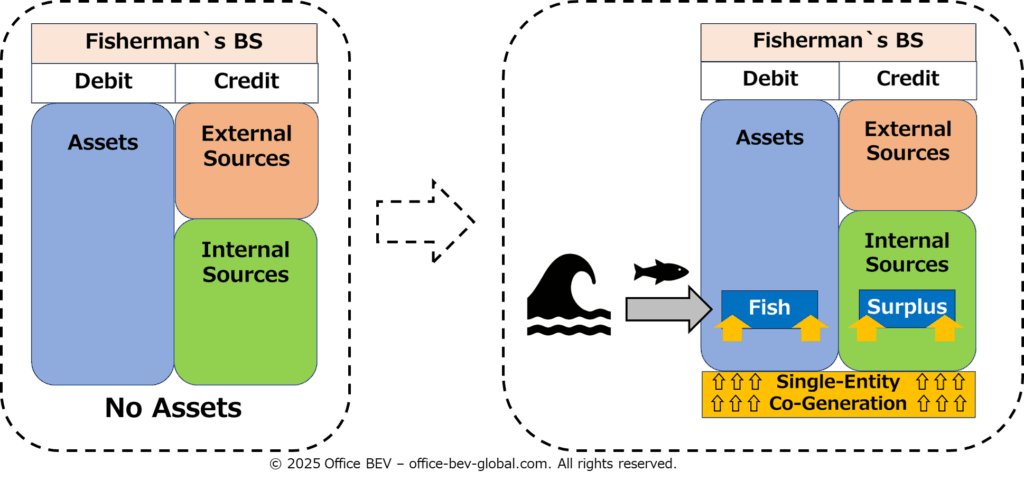

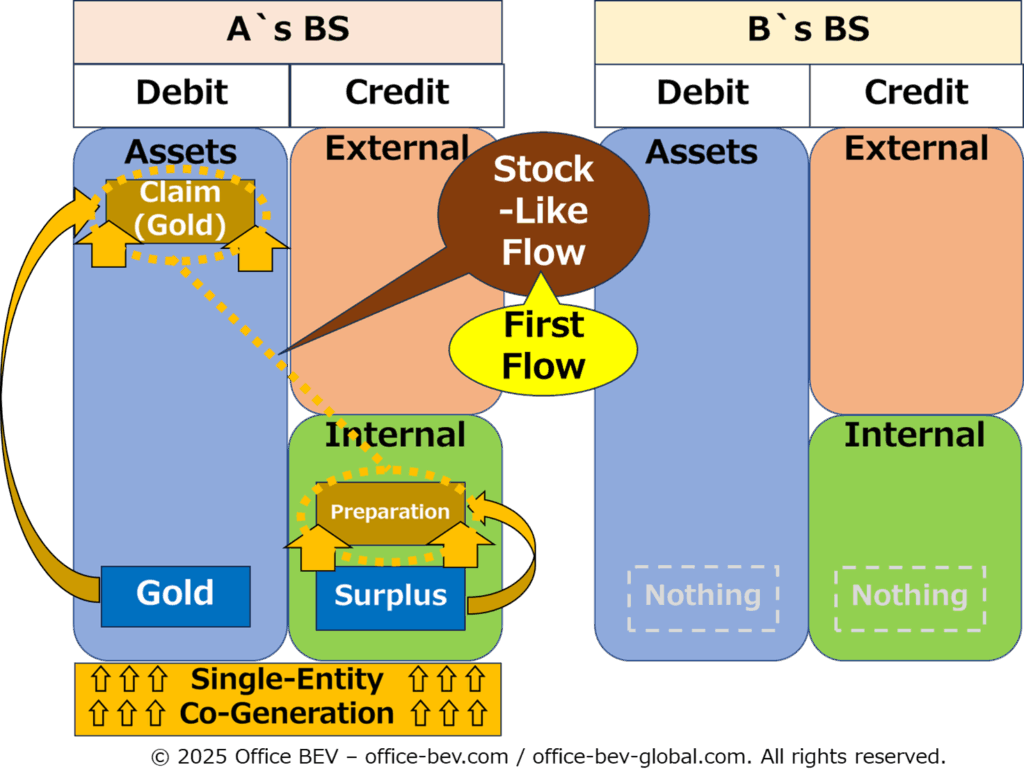

2. The Birth of Assets: Single-Entity Co-Generation

A balance sheet is structured with assets on the left (debit) and sources of those assets — either equity or liabilities — on the right (credit). For the balance to hold, both sides must arise simultaneously and in equal amounts.

We call this foundational structure single-entity co-generation.

This process refers to the moment when an asset is generated entirely within a single entity’s BS, with both debit and credit sides increasing from zero.

For example:

When a fisherman catches a fish, the asset (fish) appears on the debit side of their BS, and the surplus generated through their labor appears on the credit side. This creation happens before any transaction or exchange with others.

In this sense, asset generation is not about increase or decrease — it is about the birth of value. It is the structural origin of all asset movements.

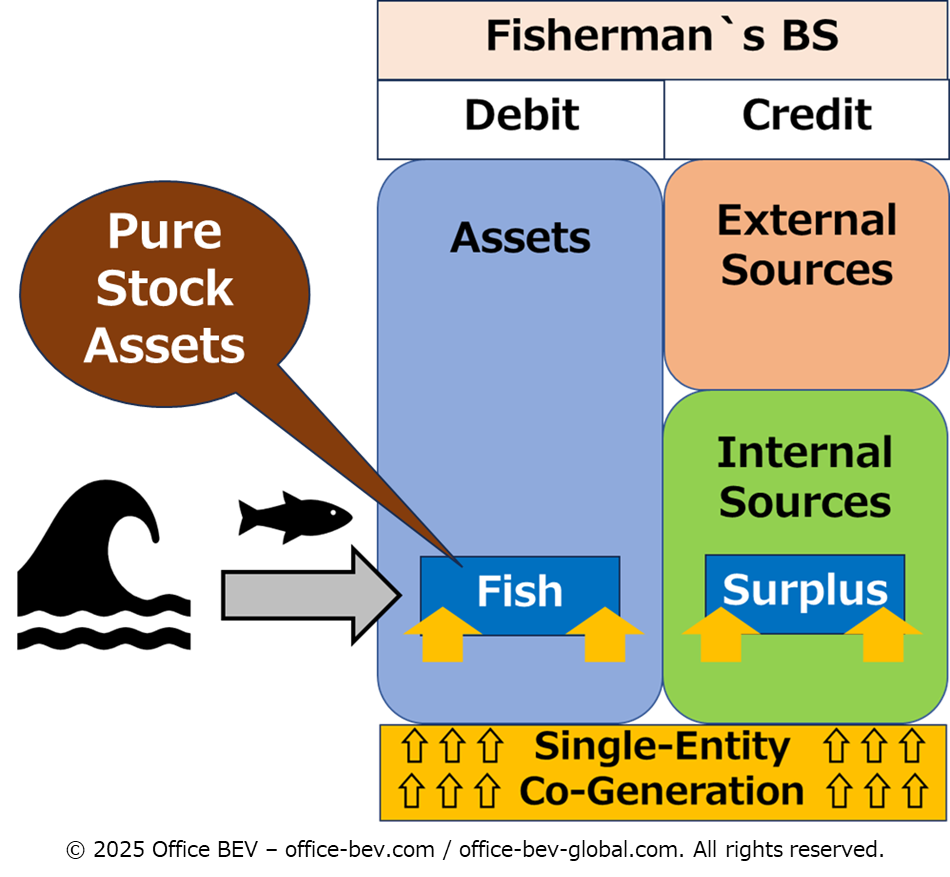

3. The Creation of Stock Assets

Assets generated through single-entity co-generation that remain within the entity and do not involve any relational claims are what we call stock assets.

These stock assets fall into two distinct categories:

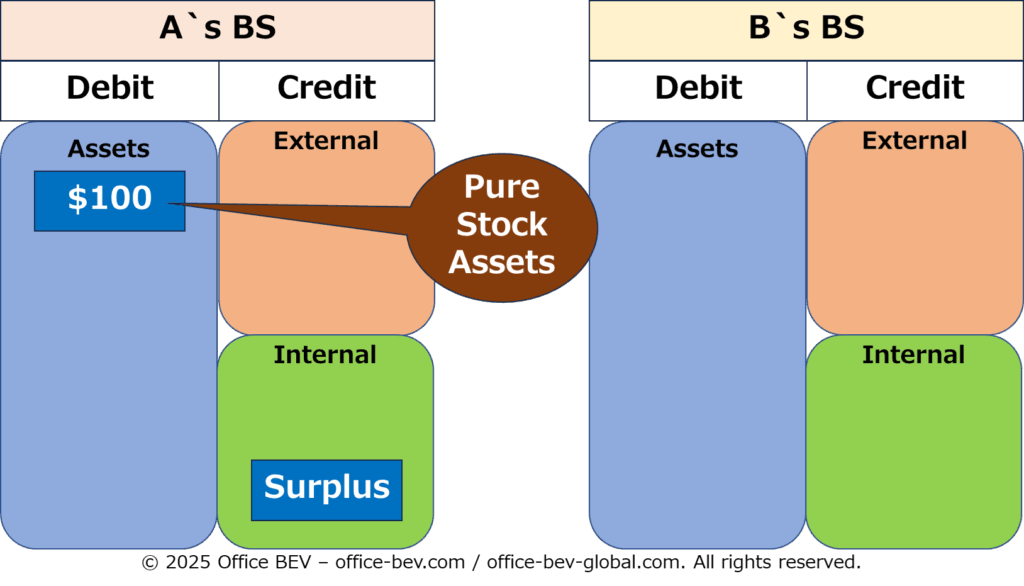

(1) Pure Stock Assets (Accumulated Assets)

These are assets obtained directly from nature or labor, with value that is already realized and confirmed at the moment of acquisition. They do not require external recognition or validation.

- Examples:

- A fisherman catching fish

- A farmer harvesting crops

- A pioneer claiming undeveloped land

Such assets are acquired through recovery and are recorded as pure stock on the BS.

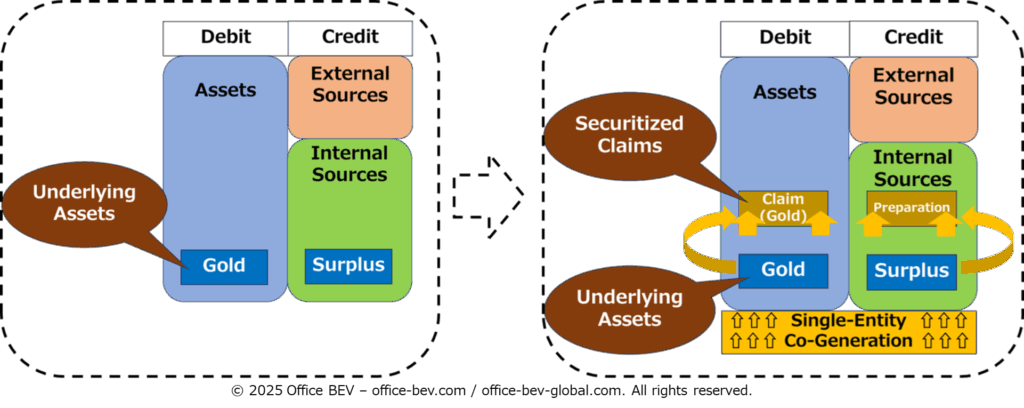

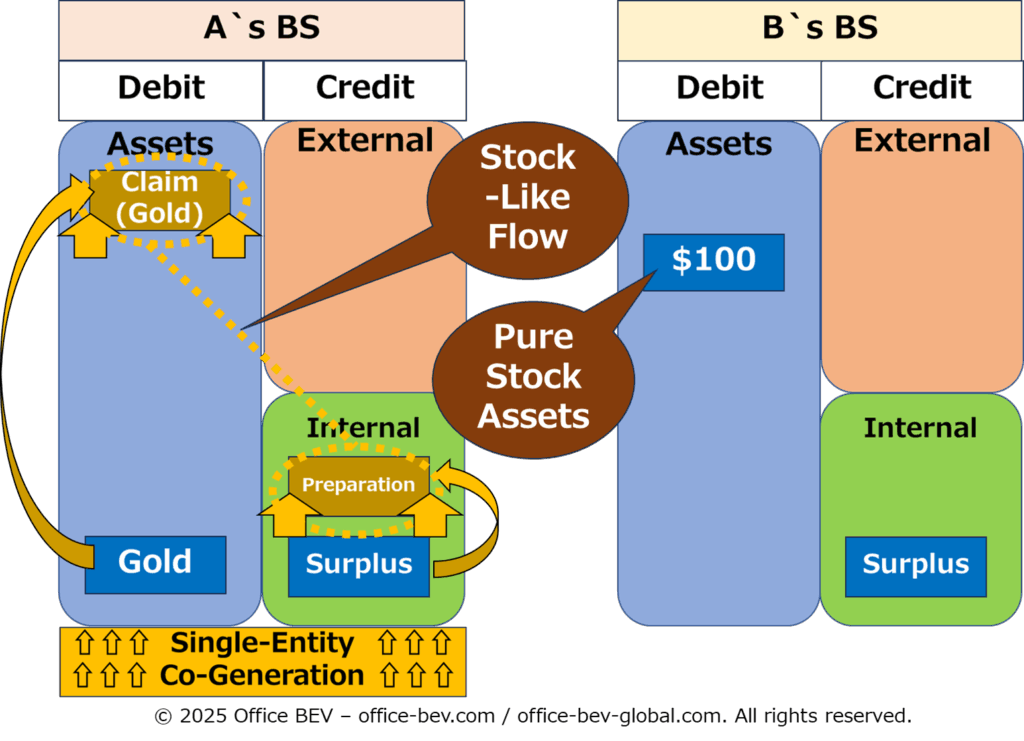

(2) Stock-like Flow Assets (Structurally Created Assets)

These assets are created via single-entity co-generation, but their value depends on future relational use. They are structurally prepared to enter into external flow, but currently remain within the BS.

This type is further divided into two subcategories:

(2-1) Securitized Claims

These are claims created against an underlying asset (the principal) in anticipation of future transfer.

- Examples:

- Creating a claim to deliver gold that one already owns

- Slicing an asset into smaller claims and issuing them as certificates

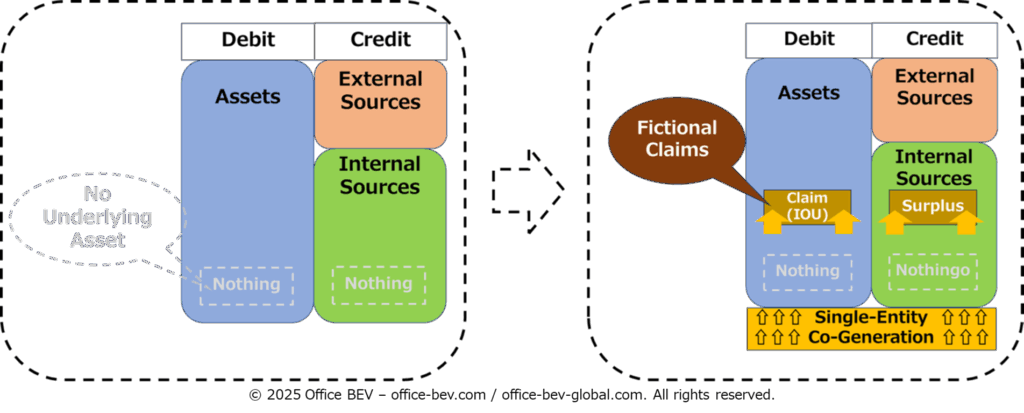

(2-2) Fictionally Created Claims

These are claims created from nothing, backed only by expectation or credibility. There is no underlying asset at the time of issuance.

- Examples:

- Fiat or credit money

- Self-issued IOU (promise to pay in the future, with no existing asset)

Stock assets, then, include both realized value (pure stock) and potential value (stock-like flow). Both are born through single-entity co-generation but differ fundamentally in their valuation and future role.

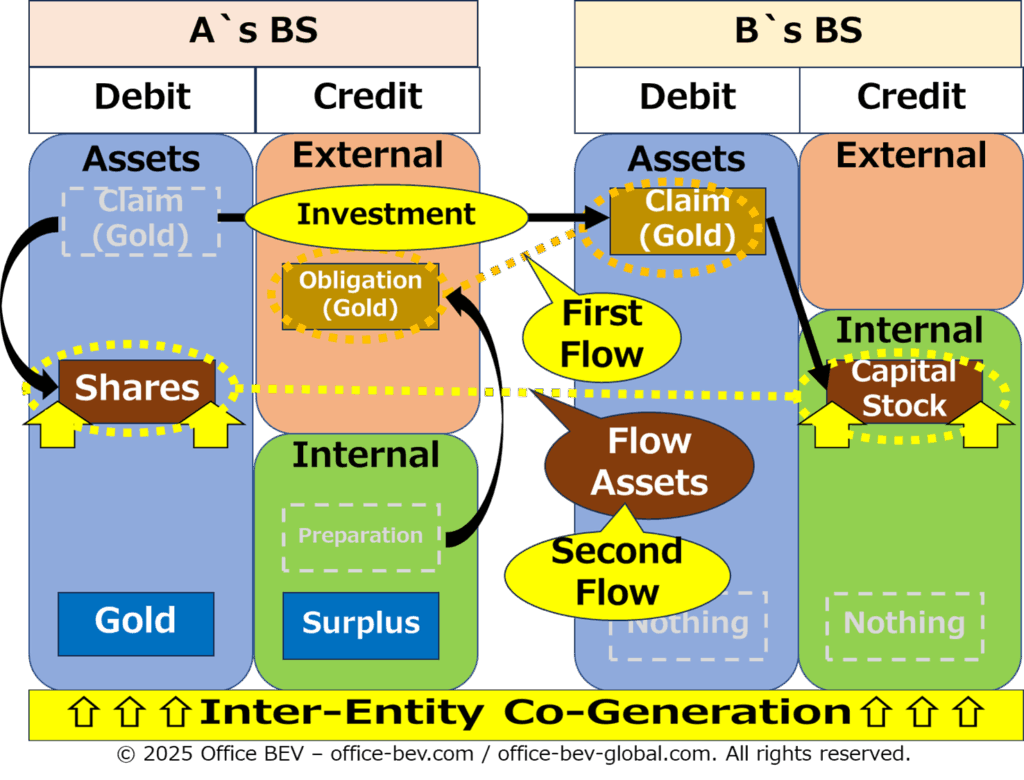

4. The Creation of Flow Assets

When assets come to hold value through relations with others, they become flow assets — defined by a structural pair of claims and obligations.

The process of creating such flow assets varies depending on the type of asset involved and the way it is deployed in relational transactions. We can identify three distinct patterns:

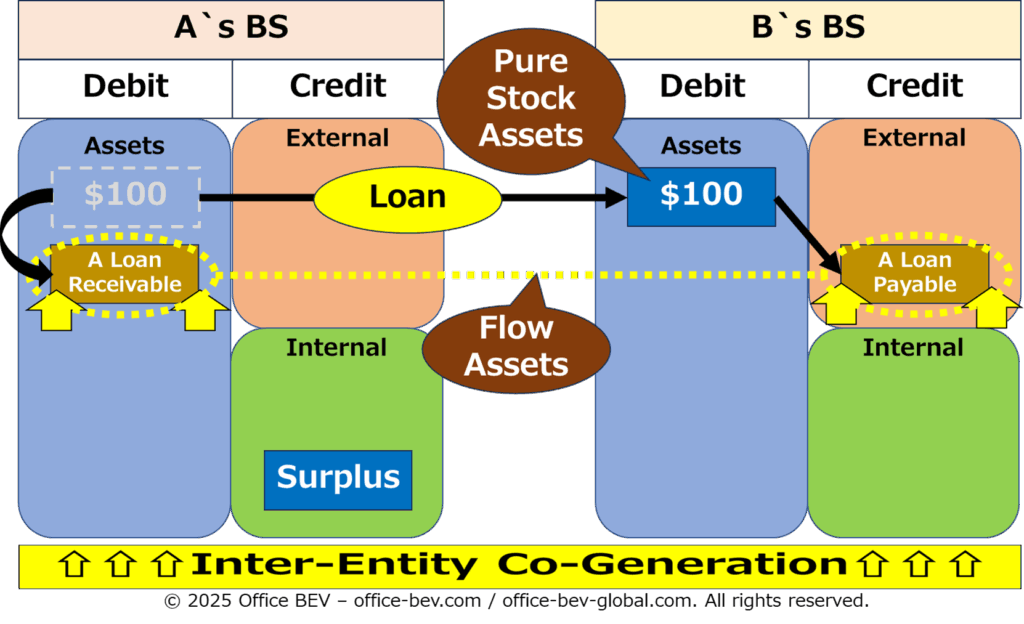

(1) Flow from Pure Stock Assets (Inter-Entity Co-Generation)

When a pure stock asset (e.g., cash) is lent rather than simply given away, it enters a flow relationship. In this process, a new pair of claims — a claim (receivable) and an obligation (payable) — is generated between entities.

This process is what we define as inter-entity co-generation.

- Example:

- A lends B $100 → A records a loan receivable; B records a loan payable

<Before>

<After>

Here, the original asset already existed (accumulated stock). The flow is born not by single-entity co-generation, but by deploying the existing asset into a relational structure. No additional single-entity co-generation is required.

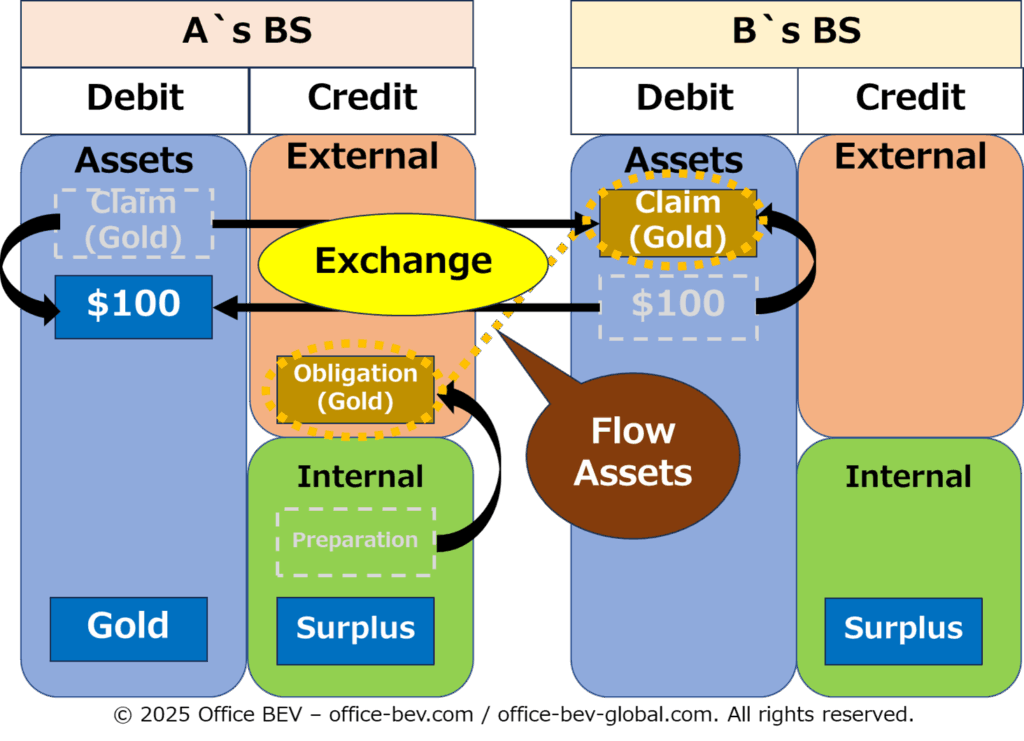

(2) Exchange of Stock-like Flow Assets (No Inter-Entity Co-Generation)

Stock-like flow assets (e.g., certificates) created through single-entity co-generation may later be transferred to others. This transfer does not itself create new claims or obligations — it merely activates the flow structure that was already prepared.

- Example:

- Transfer of bonds, checks, or existing receivables to another party

<Before>

<After>

The asset is already structurally complete. No new co-generation occurs during transfer — thus, no inter-entity co-generation.

(3) Flow from Stock-like Flow Assets (Layered Flow Structures)

When a prepared claim (such as a securitized or fictional claim) is used in a relational transaction, it generates a second layer of flow — this time with the previously issued claim itself becoming the object of a new claim/obligation pair.

This is what we call a Layered Flow Structure: a new relational flow built upon a previous one.

In this case:

- First flow: The original creation of a claim within a single BS (e.g., a certificate representing a gold claim).

- Second flow: The use of that claim in an external transaction (e.g., lending or investing it), which produces a new relational structure.

Example:

A contributes a certificate (claim on gold) to B as an investment

→ A receives shares

→ B records capital stock

<Before>

<After>

These layered flows form the foundation of recursive financial mechanisms — such as credit expansion, collateral chains, and leverage cycles — where one flow gives rise to another, and claims are layered upon claims.

5. Conclusion: Genesis as the Structural Foundation of Assets

To summarize the genesis of assets in BS terms:

- All assets are first created within a single BS through single-entity co-generation

- Stock assets include:

- Pure stock (already valuable through recovery)

- Stock-like flow assets (potentially valuable through future relations)

- Stock-like flow assets are subdivided into:

- Securitized claims (with underlying assets)

- Fictionally created claims (without underlying assets)

- Flow assets either emerge through inter-entity co-generation — when new claims and obligations are created — or are activated through the transfer of pre-existing claims, such as stock-like flow assets prepared in advance through single-entity co-generation.

Understanding this layered genesis provides the conceptual foundation for the next article, “Asset Structure,” where we explore how assets behave and are categorized within balance sheet movements — laying the groundwork for the following analysis of Interlinked Asset Flows and Transformation, as explored in the third article of this series.

3 thoughts on “Structural Analysis (1): The Genesis of Assets — Where Stock and Flow Begin”

Comments are closed.